| FG |

Done: Bludova Zoya

Introduction :

In condition of competitions and instability of environment it is necessary to respond operativly to detours from normal activity of the enterprise. Money flow management is that instrument, with the help of which it is possible to reach the desired result in the activity of the enterprise - a receptions of the profit.

Thereby, in the process of the operation of any enterprise money moving is present (the payments and arrivals) that is to say money flows; the different approaches to determination of the categories "money flows" exist; in Ukraine in condition of the inflations and crisis of the defaults on a payment money flow management is the most actual problem in finance management.

These circumstances condition the choice of the subject of the study:

In master`s work it is necessary to solve the following problems to performe these purposes :

- consider the theoretical approaches to the notion and essence of money flow;

- analyse the main methods of money flow management;

- define leading indexes, used when governing money flow;

- consider the events of impossibility to decide given problems analytically;

- produce the estimation of the investment risk of money flow;

- on base of the analysis of the factors to develop the recommendations on improvement of the mechanism of money flow management of enterprises.

Practical value of the degree study is concluded in development of concrete actions on improvement of money flow management on enterprise.

Money flow discounting

The method of the discounting money flow of the investment project is the key in modern financial analysis.

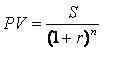

The Process of the finding of the current value is called discounting.

In order the sum grown through n periods of capitalization, is S monetary units, it is necessary to place in bank  monetary units at the beginning of the period. Such initial capital is called current applied, value of the amount S and is marked by symbol PV (of the term "present value"). For current value there is a formula monetary units at the beginning of the period. Such initial capital is called current applied, value of the amount S and is marked by symbol PV (of the term "present value"). For current value there is a formula  (1.2) (1.2)

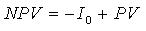

Calculation of net current value of the project, which is found on formular: (1.3) (1.3)

Net current value of the project shows, on how many given project requires less initial investment than bank deposit the amount of which is equal to the expected project profit. If net current value of the project is positive it is more profitable to invest money into the project. But if net current value of the project is negative it is more profitable to invest money into the bank.

The Rate of the discounting of the project money flow, under which net current value is zero, is called the internal rate of return project. In English literature internal rate of return has a special indication IRR (the term "internal rate of return").

From given determinations, as well as from formulars (1.2) and (1.3) directly results that internal rate of return project is the solution decision of the following equation:  (1.4) (1.4)

We shall note that in efficient financial market the investment projects with alike financial risk must have an equal internal rate of return. We shall also note that the higher financial risk of the project that greater internal profit is required from the project by the potential investors.

Analysis of the sensitivity of a project money flow :

The analysis of sensitivity of a project money flow investment - is the analysis of the process as money flows of the project change when one or several influencing factor upon them change.

At decision of the economic problems situations often occur when qualification of the direct performers does not allow to develop enough identical economic and mathematical models or solve the problem by modern mathematical methods. In such event the decision can be found by methods of simulation modeling.

Since models disregarding risk an less interesting, we shall take as an investment project, under which any money investment will be considered; generating money flows in the future.

Economic and mathematical model of money flow given project is defined:  (1.5) (1.5)

where:

Q - an annual production output ;

р - expected price ;

u - a variable costs in payment on one product;

F - a constant costs for one year;

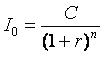

I0 - an initial investments;

n - a length of the project in years;

t - a tax rate;

r - a rate of the discounting money flow project.

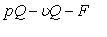

Profit of the project before payment of the tax for one year is  (1.6) (1.6)

Accounting tax profit will be pQ - vQ - F - I 0 / n (1.7)

When parameter of the models are constant p = const, Q = const, F = const, I 0 = const - the solution is rather simple. We shall present these parameters as casual parameters with given law of the distribution. We shall conduct the statistical studies of similar investment project in similar economic condition, shall consider that they are subject to one of the laws: even, normal or significant. For this it will be necessary to generate the casual numbers evenly portioned in interval [0,1].

The Long-run objective of given the problems of simulation modeling is finding the probability density of the random quantities Cj (1.5).

The Decision is produced thereby.

Four arrays of evenly distributed numbers in interval [0,1] are generated each array has so aproximately N=100. Are generated arrays  then. So mean then. So mean  and dispersion and dispersion  depend on the law of the distribution numbers used. depend on the law of the distribution numbers used.

Even law:

Significant (exponential) law:

Normal law:

Substituting j-e numbers in algorithm of the formula (1.7) and calculate Aj for each number j. Depending on condition positive accounting tax profit or no (1.5) hereinafter use the correponding algorithm.The outputs is used an array of casual numbers Dj with sought law of the distribution.

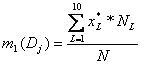

We Build the histogram with number category Dj with number category L=  =10. beforehand find Djmin and Dkmax. The Difference Dkmax - Djmin do on L=10, this there is width of our category. We find the mediums all categories =10. beforehand find Djmin and Dkmax. The Difference Dkmax - Djmin do on L=10, this there is width of our category. We find the mediums all categories  . .

Have:

where:

- a population mean of the random quantity Dj ; - a population mean of the random quantity Dj ;

-an average importance L-go category ;

- an amount digital in L-y category; - an amount digital in L-y category;

N=100 - a gross amount digital.

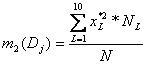

Similarly we calculate:  : :

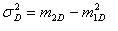

The Dispersion casual digital is defined as:

Taken at definite moment the total company capital is stable, then in some time it changes. The capital on flow happens daily. The Competition between enterprise requires the constant adjustment to changing condition; the technological improvements, allowing significant capital investments, inflation, the percent rates changes, tax legislation, - all these render the big influence upon the capital flow of the enterprise.

So it is necessary to control effectively the capital flow within the framework of enterprise.

In conclusion :

In conclusion we can say that in this work we have a simple model, but in real life it is necessary to use more complex models.

When writing the given abstract the master`s work was not completed yet, the final termination is January 2007. The full-text of the work and all materials on subject can be received from the author or leader after the specified date.

on main page

|

JGKJYF |