The problems of company’s alternative development, its bankruptcy and bankruptcy prediction have become very relevant in Lithuania during the last decades. According to the different authors, every bankruptcy is assessed as its local phenomenon as well as the macro economic appearance, which brings a lot of economic and social consequences for people who lose their jobs as well as for appropriate institutions. Theoretical results of research are often integrated into the process of company’s administration, however the rising number of bankruptcies shows that bankruptcy prediction is not assessed properly in the practical level of company’s management. The administration practice of failed companies in Lithuania shows that this process often determines negative results in the company and is very painful for its employees as well as for its creditors and owners. The changes of external conditions and the pressure that company experiences in the nowadays market economy often go the limits of the company’s management competence. Working companies face the global transformation, which is very specific, so it is not always possible to apply the traditional means of crisis management in their administration. Bankruptcy, as one of crisis development alternative in the company, is possible to avoid properly estimating bankruptcy probability and applying prevention means in company’s performance in time. When bankruptcy mechanism is late, to start new activities or to reorganize the company is often impossible because of the short company’s reserves. Bankruptcy prediction should be based on the continual observation and assessment of its financial state in order to notice the very first bankruptcy features, to define their reasons and to estimate their solution possibilities. The article deals with the theoretical dynamic alternatives of crisis development in a company. Bankruptcy features are analyzed applying discriminant analysis.

Keywords: crisis in a company, bankruptcy probability, bankruptcy prediction, discriminant analysis.

Introduction

Because of the difficult dynamic changes of the business environment company’s performance often becomes difficult to forecast. The most decisions are made without detailed analysis of information about future perspectives of its performance. In such indeterminate conditions crisis appears in the company determining the stagnation of its performance and even its bankruptcy. Statistical data analysis showed that over 40 percent of company’s performance is losing; however the system of bankruptcy prevention and company’s reinstatement is just being created in Lithuania. The number of insolvent companies is growing. These companies are usually liquidated and only a few are rehabilitated and reorganized. This lets us make the presumption that the features of crisis situation in the company are diagnosed too late, they are not assessed properly and it determines danger in the company’s performance.

A lot of head managers of the company think that profitable performance and creation of successful strategies make presumptions to avoid crisis and herewith bankruptcy in the company. However, crisis possibility persists even during the successful company’s performance so only a few companies’ head managers making strategic plans integrate the management level of preventive situational diagnostic into them.

The scientific problem of the research – the problematic of bankruptcy probability as dynamic alternative of company’s development is widely explored in Lithuanian as well as in the foreign scientific works, but it is not properly assessed the diagnostic of crisis situation, which is mostly dangerous in the company’s performance. In the theoretical and practical works the authors concentrate their attention at the identification of crisis features in the particular crisis levels and at the financial rate variations connected with these features. The reasons are assessed only after the bankruptcy has happened and forecast of crisis situation in the successful companies is absent.

The aim of the research – to define the main features of crisis development alternatives, to provide their diagnostics possibilities for bankruptcy probability estimation in a company.

Object – the diagnostics of crisis development alternatives in a company.

Research methods – analysis of the scientific literature, mathematical statistical methods, discriminant analysis, filing and summation.

The Main Features of the Crisis in a Company and the Need of its Diagnostics

Big attention has been paid at the crisis topic in the company during the last few years. Darling, Kash (1998) Chong, Escarraz (1998), Maynard (1993), Offer (1996), Trenenkov, Dvedenidova (2000), Altman, Edvard (1968) and other scientists made some research concerning crisis forecast and the search of preventive instruments, their typology and modeling the decision possibilities in the company. In Lithuania the analogous research was made by Bivainis, Garskaite (2000, 2002), Purlys (2001), Tvarijonaviciene (2002), Grigaravicius (2002) and others.

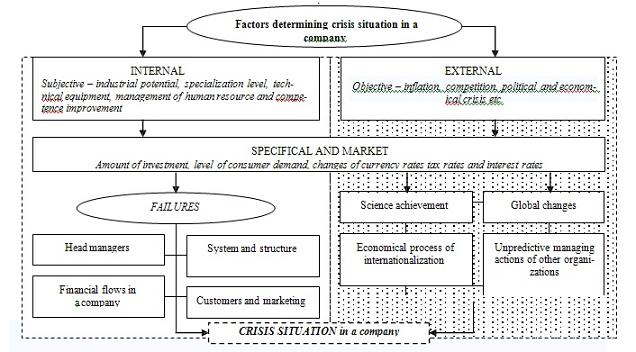

It is impossible to avoid crisis in the company working in the indeterminate business environment. The company faces with the situations when objective conditions of external and internal environment appear which affect the balance state of the company’s performance. Then a company, willing or unwilling, has to pass into the new performance state which results better efficiency and consequence and improves other parameters of its performance. However, to work in such objective conditions which require changes, it is impossible only for those companies which have so called critical internal potential. Not having such potential companies are determined to vegetate or even fail (Stoskus, Berzinskiene, 2005). This internal potential includes not only stability of the financial rates of the company but competence of the head managers, labour force and flexibility of the industrial system as well. Factors of knowledge, business intelligence and orientation are very important during crisis period in a company. Welltimed forecast of the first crisis features and its reasons let decrease the negative influence on the company’s performance and avoid bankruptcy. The diagnosis of crisis situation should be pointed to the identification of the factors which determined the crisis and their early rehabilitation. The influence of the factors on the company’s performance was analyzed by Clark (1995), K. Laitinen (1999), Chong, Escarraz (1998), James (2000), Liucvaitis (2004), Zakarevicius (2004), Sakalas, Savaneviciene, (2004) and others. It is noticed that the influence of the environment during the crisis in a company has a synergy effect: external conditions consolidate expression of internal factors. The scheme of the factors determining crisis situation in a company is shown in Figure1.

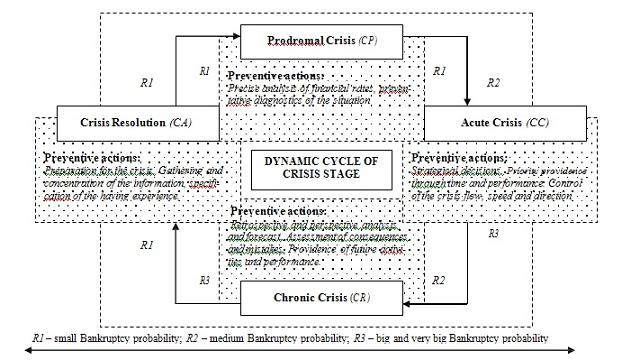

Assessing the diagnostics of crisis situation in a company, it is very important to estimate the dynamic alternatives of the situation, because the bankruptcy probability and possibility has different level in each of them. According to the works of the authors Offer (1996), Mitroff (1996), MacKenzie (1994) Fink (2002), there are four main stages of crisis development alternatives which create dynamic cycle: Prodromal Crisis, (CP); Acute Crisis (CA); Chronic Crisis (CC) and Crisis Resolution (CR).

The dynamic stage of prodromal crisis is related to the warning stage. In most cases it is the beginni ng of thechanges. In this stage bankruptcy probability is not very big, because after having done the preventative diagnostics of financial rates it is possible to define the first signals of crisis situation and to prepare scenario. If such situation is not defined and properly assessed, crisis can appear and disorganize company’s management what will cost company a big loss. The stage of prodromal crisis is often called precrisis level (Fink, 2002), but this title is more often used when the retrospective of the company’s performance is assessed and the reasons of crisis situation are defined. Bankruptcy probability is very high in the stage. And this shows that it is very important to predict crisis situation in time and to prepare very carefully to solve it. Sometimes crisis is predicted, recognized, but scenario is not made. In this case analysis paralysis appears in a company’s performance and bankruptcy probability becomes very high. It proves that it is very important to define crisis in its very first stage to avoid complications in company’s performance and to escape bankruptcy process. It is easier to manage crisis when it is predicted in advance. Unexpected crisis is difficult to manage, is more expensive to overcome and it often leads company to a failure.

The following stage of the crisis is acute crisis ( CA) (Fink, 2002). It is irreversible stage of the changes. The prefatory stage of the crisis has already finished and a company enters into the hasty acute stage of the crisis. In this stage it is impossible to recover all loss which amount depends on the company’s possibility to manage crisis. In the prodromal stage it is possible to forecast and recognize crisis, however in acute crisis stage it bursts suddenly. Proper reaction and strict planned actions let accumulate its consequences and avoid bankruptcy. Intervention of proper actions makes presumptions for right preparation which lets control crisis flow, speed, direction and length. In this stage crisis control is necessary as much as possible. In other way it is possible to accumulate crisis influence forecasting the time intervention and defining the action priorities of the different objects in a company.

Essential difficulty controlling acute crisis in a company, even having prepared well to it, is its speed and intensity, which appear in this period. The speed depends on crisis type, and its intensity is determined by the value of the possible result. If it is possible to define the crisis speed and intensity in the prodromal crisis stage, the presumptions can be made to prepare for the crisis management and control when it reaches acute dynamic stage. In the time aspect acute crisis is the shortest but its consequences are the largest.

The third stage of the crisis in a company is Chronic Crisis (CC). It is so called cleaning stage. If the detailed research or audit is not done, long-lasting negative phenomenon roots in a company. It is a period of recovery, analysis, uncertainty and rehabilitation. Effective management of crisis, competent performance of head managers, right decisions help company survive with the least possible loss. This period is important for preparation of oncoming critical situations, analyzing last failures, decision making etc. It also could become the time of financial changes, management shake in a company, consolidation of few companies or even bankruptcy. This period can be termless and only company’s decisions can moderate it.

The last fourth stage is Crisis Resolution (CR). In this stage the final crisis management aim is reached. When a company faces crisis, the best scenario based on real counts has to be made to overcome it. In this crisis resolution stage when the trajectory of changes is possible to forecast, the best scenario of rehabilitation performance can be chosen. In this period one crisis is ending and another is starting.

To sum it up, it could be claimed that the importance of crisis diagnostics is emphasized in every crisis stage. A lot of different diagnostics models can be used to define crisis stage, its level, development tendencies and bankruptcy probability.

Means of Bankruptcy Prediction

A lot of different means of bankruptcy prediction are found in the scientific literature. Bankruptcy prediction based on the financial rate changes in the company is the most usual way to predict company’s failure. All company’s financial rates which can predict company’s failure can be put into two groups: financial rates which show bad financial state of the company during the period and financial rates which show some problems in the company’s performance (Kovaliov, 1994).

Credits and debts which are not paid in time show that a company has financial difficulties. In this case it is necessary to look through some balances of the last few years and to estimate this position during the last fewyears. If this problem appeared only last year, it is necessary to define its reasons and find the best way how to solve it.

Negative state of financial rates from the second group can appear not only in the insolvent company b ut in the profitable one too.

Different methods are used to predict bankruptcy in the company. Mackevicius and Poskaite (2000) claim that two analyses methods are best to predict bankruptcy: system of different comparative rates and proportion of solvency and profitable rates.

Altman rate system is very useful practically. Solvency index is counted using multi discriminant analysis (MDA) and is based on the presumption that only two rates show possible bankruptcy in the company: covering ratio (Kp = short-term capital / short-term liabilities) and financial dependence ratio (Kfp = lent capital/ all asset).

The first ratio defines company’s liquidity, and the second – financial stability. The bigger covering ratio and the less financial dependence are, the less probability of bankruptcy is. And conversely, company can fail when its covering ratio is decreasing and financial dependence is growing. In this case scientists found discriminant point, which lets all these ratios to put into two groups: ratio combinations, having which company can fail and ratio combinations, having which company does not have probability to fail.

To predict bankruptcy probability the models of relative solvency rates are used R.Taffler and H.Tisshaw, Spingate, R.Lis and Ca-Score and Fulmer models.

To sum it up, assessing the possibilities of company’s performance and estimating real probability of bankruptcy, it is necessary to apply different means of bankruptcy prediction which supplement each other and let define wider spectrum of performance problems.

Bankruptcy Prediction Using Discriminant Analysis

For a number of years, there was considerable research by accountants and finance people trying to find a business ratio that would serve as the sole predictor of corporate bankruptcy. William Beaver conducted a very comprehensive study using a variety of financial ratios (1966). His conclusion was that the cash flow to debt ratio was the single best predictor (Chuvakhin & Gertmenian, 2003).

Beaver’s unvaried analysis led the way to a multivariate analysis by Edward Altman, who used multiple discriminant analysis in his effort to find a bankruptcy prediction model. He selected 33 publicly-traded manufacturing bankrupt companies between 1946 and 1965 and matched them to 33 firms on a random basis for a stratified sample (assets and industry). The results of the multiple discriminant analysis yielded an equation; he called the Z – score that correctly classified 94% of the bankrupt enterprises and 97% of the non-bankrupt enterprises one year prior to bankruptcy. These percentages dropped when trying to predict bankruptcy two or more years before it occurred.

The ratios used in the Altman model are:

where A – capital/ assets;

B – inappropriate balance/ assets;

C – profit before taxes/ assets;

D – stock value in the market/ liability;

E – sales/ assets.

When Z < 2.68, bankruptcy is possible working capital over total assets, retained earning over total assets, earnings before interest and taxes over total assets, market value of equity over book value of total liabilities, and sales over total assets (Altman, 1968).

The Z – score model has been extended to include private companies (Z’ model) and non-manufacturing firms (Z’ model) (Chuvakhin & Gertmenian, 2003). Although accounting ratios were shown to predict bankruptcy accurately for the manufacturing industry, such financial ratios usually lack theoretical justification. Since bankruptcy is cash oriented phenomenon, the use of variables based on cash flows is theoretically appealing. Specifically, the equation developed by G.H. Lawson was used to test a bankruptcy predictive model (Aziz et al, 1988, 1989). Lawson's relation includes operating cash flow, net investment, liquidity change, taxes paid, shareholder cash flow, and lender cash flows. Lawson’s cash flow based model is compared to Altman’s accounting based financial ratios analyses with updated discriminant coefficients. The results show that it is difficult to state which model performs better (Aziz, 1984).

Discriminant analysis is superior to linear discriminant analysis in predicting bankruptcy and bond ratings. Furthermore, cash flow measures have no information content beyond accrual earnings in predicting corporate failure. Information content is defined as the ability of data to predict corporate failure and corporate bond ratings. However, accrual earnings have information content over and above cash flow measurements. On the other hand, neither cash flow measures nor accrual earnings improve the classification accuracy of bond ratings substantially (El Shamy, Mostafa Ahmed, 1989).

Regarding the use of cash flows to predict corporate bankruptcy, the common view is that cash flow information does not contain any significant incremental information over the accrual accounting information to discriminate between bankrupt and non-bankrupt enterprises. (Watson, 1996). One author argues that cash flow from operations could be misleading because of management’s manipulation of the timing of cash flows, such as not paying bills on time or reducing inventory below desired levels. These maneuvers increase the measure of cash flows from operations reported in the income statement. Such an increase is probably not a good sign, and these distortions arise most often from companies experiencing financial distress (Viscione, 1985).

On the other hand, there is the opinion that cash flow from operations has not been properly measured, that some researchers did not validate their model that cash flows and accrual data were highly correlated in the earlier days, and that incomplete information does not allow for study replication. These reasons and additional evidence is used to regard the significance and predictive ability of cash flows for financially distressed companies (Sharma, 2001).

Other concerns regarding bankruptcy prediction models deal with potential problems associated with models inappropriately applied. This could be the case when statistical models derived for a certain time period, industries, and financial distress situations are applied to situations other than those originally developed for. It is found that these models are sensitive to time periods. This means that the accuracy of the model decline when they are applied to time periods different from those used to develop and build the model. Furthermore, while Ohlson's model was sensitive to industry classification, Zmijjewski's model was not. However, neither model is sensitive to financial distress situations other than those used to develop the models. Therefore, it is not only necessary to understand the uses of prediction models, but to comprehend their limitations as well. (Grice & Dugan, 2001)

Regardless of bankruptcy prediction model’s disadvantages or shortcomings, the idea of developing such models to attempt to predict financial distress and failure has been welcomed around the globe. For example, previous empirical studies using financial ratios as predictors of corporate bankruptcy have been conducted in Japan. However, due to the limited sample size, the results are not general. This Japanese study proposes a universal model that accurately predicts 86% of bankrupt companies, independent of industry type and its size (Shirata, 1998).

Method

Discriminant analysis method is a statistical technique used to develop functions, which discriminate between two (or more) naturally existing groups. Specifically, the question is whether or not two (or more) groups are significantly different from each other with respect to the mean of a given variable(s). If the means for a variable are significantly different in different groups, then this variable discriminates between the groups. This is the simplest way.

The most common application of discriminant analy- sis is to include many measures in order to determine the ones that discriminate between groups. This leads to building a model of how best to predict to which group a given object belongs to. By some methods the analysis can be performed step by step, where all variables are reviewed and evaluated at each step to determine which contribute the most to discriminating between groups. It can also be done backwards, where all variables are included in the model and at each step, the variable that contributes the least to the predictive model is eliminated.

Discrimination possibilities of variable are set when empirical average of i variable in j group and general empirical average of variable i are market with symbols:

then:

where:

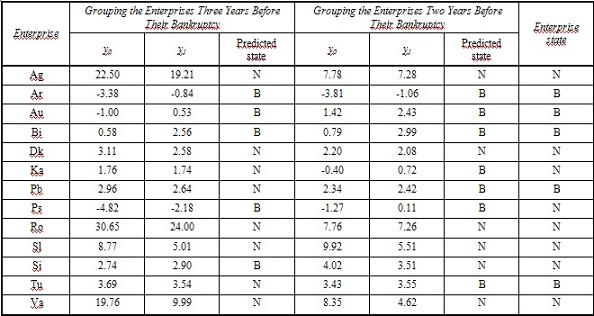

For the derivation of the classification functions by discriminant analysis method we used financial data of 13 enterprise 2 years before insolvency of 5 of them. Another 8 enterprise were successful.

The classification functions appeared to be the following for the successful enterprises:

and for the failed enterprises:

where y0 , y1 – classification function values of successful and failed enterprises;

xgp – net profitability;

xtm – ratio of short-term solvency;

xis – ratio of indebtedness;

xgl – ratio of quick liquidity.

The program package Statistica was used for discriminant analysis. Making these functions, program checked the correctness of classification of them as well. The results showed that two enterprises were classified incorrectly. They were grouped with failed, though they were successful during the next two years.

Classification functions are used in this way: the indicators of searching enterprise are written down into both functions. Enterprise is classified to the group, which function has a greater value.

The Results of Enterprise Classification, Grouping the Enterprises Three and Two Years before Their Bankruptcy

The Main Results

Effectiveness of developed classification functions was checked grouping the same enterprises in three years’ time period before bankruptcy and in two years’ time as well. Results are given in the table 2. Grouping the enterprises in three years’ time period before bankruptcy, when the bankruptcy features were weaker, only 4 enterprises were predicted incorrectly and the classification reliability was 70 percent. Grouping the enterprises in two years’ time period before bankruptcy, the classification reliability was already 84 per cent. In this case two enterprises were predicted incorrectly.

The same enterprises were examined using neural network method by the same authors (Purvinis and others, 2005). Applying this method prediction reliability was 92 per cent.

Conclusions

1. Nowadays indeterminable business conditions make it difficult to forecast business environment and often create presumption for crisis in a company. It is difficult to avoid it, but after having no- ticed the first features of crisis and reacted to them in time it is possible to continue successful company’s performance.

2. To avoid complications in company’s performance it is important to diagnose the first features of crisis in prodromal crisis stage. Unexpected crisis is difficult to control and its management is more complicated, more expensive and often does not have any succession in company’s performance.

3. Having done the research it can be claimed that

companies do not consider properly the preventa- tive system of bankruptcy what determines risk in further company’s performance. The results of the research showed that successful companies more often noticed the first features of bankruptcy than failed companies. It shows that crisis is a natural process in company’s performance and its further development depends on its internal potential: competence of head managers, quality of human resource and financial capability.

References

1. Altman, E. Financial Ratios, Discrimination Analysis and the Pre- diction of Corporate Bankruptcy // Journal of Finance, 1968, 23, September.

2. Aziz, A. Bankruptcy prediction - an investigation of cash flow based methods / A. Aziz, D.C. Emanuel, G.H. Lawson // Journal of Management Studies, 1988, 25(5), p. 419 -437.

3. Aziz, A. Bankruptcy Prediction // Journal of Finance, September, 1984.

4. Aziz, A. Cash Flow Reporting and Financial Distress Models: Testing of Hypothesis / A. Aziz, G.H. Lawson // Financial Ma n- agement, 1989, 18(1), p. 55-63.

5. Beavei, W. Financial Ratios as Predictors of Failure // Journal of Accouting Research, 1966, Vol.4, p. 71 -127.

6. Bivainis J. Antikrizinio imoniu valdymo priemones / J. Bivainis, K.Garskaite // Ekonomika. Vilnius, 2002, p. 19-36.

7. Bivainis J. Imoniu bankroto gresmes ivertinimas / J. B ivainis, K. Garskaite // Ekonomika. Vilnius, 2000, p. 51-56.

8. Chong, J. DR Escarraz Anticipating and Dealing With Financial Crisis / J. Chong, D. Escarraz // Management Decision, 1998, 36(9/10).

9. Chuvakhin, N. Predicting Bankruptcy in the World Companies / N. Chuvakhin, L. Wayne Gertmenian // Journal of Finance, April, 2003.

10. MacKenzie, S. B. The impact of organizational citizenship beh a- vior on evaluations of sales performance / S. B. MacKenzie, P. M. Podsakoff, R. Fetter // Journal of Marketing. 2004, N. 57, p. 70-80.