Sourse of information:

http://www.steelonthenet.com/pdf/ukraine_coal_21-Sep-08.pdf

While being of a crucial importance for energy generation, Ukrainian coal mining sector experiences hard times being depredating for two decades. In 2008 Ukrainian coal mining sector faced three major challenges: deficit of steam coal at power stations conditioned by increase in consumption, disruption of coking coal supplies from Russia and hourly wage introduction initiated with an aim to reduce high death rates.

During the Soviet Union times Ukraine considered to be the main source of coal for the whole USSR, as it supplied 23% of the total coal extraction of the Union. Ukraine has different kinds of coal: hard coal, bituminous coal, anthracite, etc, the country occupies the 8th place in the world on amount of coal resources - 117.3bln tones. This potential predetermined dependence of Ukrainian industry and power sector on coal supply. Although the coal-mining industry of Ukraine occupies a leading position in supplying the country with power and the amount of coal resources is sufficient, coal mining continually has decreased. Coal mining decreased over the decade 1990-2000 by half from 164.8mln tones in 1990 down to 76.2mln tones in 1999). The decay of the coal mining industry was partially conditioned by its development in the last years of the USSR existence. Thus, the investment policy of the Soviet Union supported the idea of reducing investments in the coal-mining operations in the Donbass region. The main reason for such actions was a possibility to develop coalfields in the eastern regions of Russia, containing cheaper coal.

The decline in coal production during the 1990s was caused in large part by the collapse of domestic demand and the recession of heavy industry as Ukraine's economy contracted. Since Ukraine became independent in 1991, the country's coal sector has fallen into disarray: the industry suffered from labor strikes, hazardous working conditions, inefficiency and low productivity, corruption, consumer non-payments, unpaid wages and huge debts, and outmoded equipment.

One of the major reasons behind that was technological and technical state of mines. Currently almost 40% of all Ukrainian mines have been functioning for more than 50 years, and 15% for more than 70 years.

Attempts to reform the Ukrainian coal sector began in 1994 when the ministry of coal industry was created. However all reform attempts have failed up to the present moment to tackle unprofitability of the existing coal mines. About a hundred loss-making pits have been closed so far but with so many pits sunk deep in debt, the privatisation programme is still stuck. Although mines are expensive to operate, the Ukrainian government has been reluctant to reduce the number of mines due to the social costs of closing so many pits in an area with few other jobs.

Coal extraction recovered after its biggest decline on the edge of the century and this year is expected to reach 80mln tones, (see table 1).

| 2006 | 2007 | Jan-Aug 2008 | Jan-Aug 2008, y/y | |

| Steam coal | 50,1 | 47,0 | 33,6 | 7,3% |

| including extracted by state owned enterprises | 35,0 | 32,4 | 23,4 | 3,2% |

| Coking coal | 30,1 | 28,4 | 18,8 | 0,2% |

| including extracted by state owned enterprises | 11,4 | 9,8 | 7,1 | 8,0% |

| TOTAL | 80,3 | 75,4 | 52,4 | 4,4% |

Source: Ministry of coal industry.

Steam coal is fully consumed by heating and power sector. Thus in 2007 more than 40mln tones was consumed by CHP's and the rest including 3.5mln tones imported from Russia went to boiler houses and population.

One of the resent issues of the 2H08 relates to the coal reserves at boiler houses and CHPs. While after the dramatic decline in July 2008 when coal reserves at CHPs reduced by 17.3% or by 0.51mln tones down to 2.44mln tones on the 1st of August reserves were still larger by 0.36mln tones than what was at depots a year ago (2.09mln tones) the declining tendency continued in August and September. During the first half of September reserves dropped from 2.4mln tones down to 2.1mln tones instead of 3.1mln tones planned in energy balance of the country. This situation is mainly conditioned by usage of 1.2mln tones of coal to compensate for unexpected closure of the second block of Khmelnickij atomic power station. As the reserves appeared to be insufficient to compensate the closure in full, 5 other energy blocks fueled by natural gas have been put in service, which is increasing the price of electricity.

Moreover due to high demand for coking coal from the side of metallurgy dual-purpose coal is fully dispatched to coking plants as this usage is more profitable.At the same time Ministry of fuel and energy plans to increase reserves of steam coal up to 4mln tones before the beginning of the heating season (October 15), which imply importing of foreign (presumably Russian) coal in amount of 2.4mln tones. In the nearest future Ministry of coal industry expects increase in coal extraction by 5-6mln tones accompanied by closure of the pits producing less than 500 tones of coal per day.

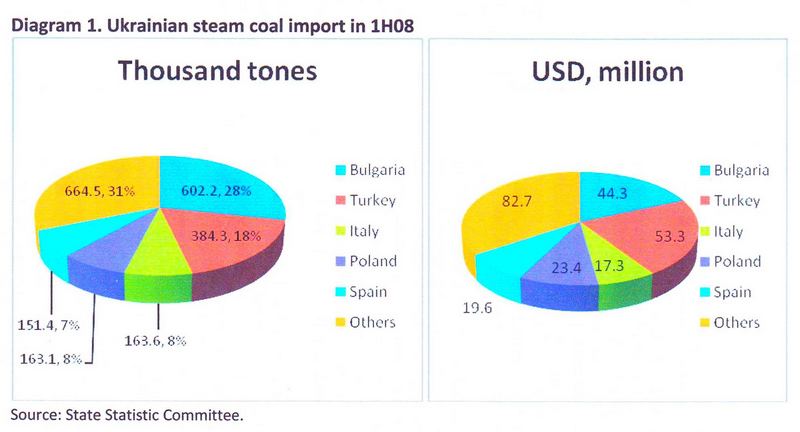

While importing steam coal from Russia, Ukraine exports it to many countries (see Diagram 1)

Ukrainian export of coke is also growing fast. Thus during seven months of 2008 coke export grew by 40.1% y/y and reached 0.57mln tones or USD166.56mln. In 2007 the growth was 36.6%y/y while export reached 0.58mln tones or USD 102mln. While exporting steam coal Ukraine lacks coking coal. Ukrainian metallurgy needs around 30mln tones of coking coal per year, while Ukrainian mines are able to supply less than 20mln tones. Thus in the first seven months of 2008 metallurgical enterprises bought 18.53mln tones of coal concentrate and run-of-mine coal only 11.93mln tones of which were of Ukrainian origin. Major role in coking coal supply is played by Russia, imports from which reached 4.93mln tones up to 1 August 2008, while USA and Canada sold 0.97mln tones and Kazakhstan sold 0,67mln tones.

Presence of North American countries in the list of major coal suppliers needs special attention As these remote countries turned to be important suppliers due to efforts of just one coke chemical plant JSC Alchevskkoks (member Industrial Union of Donbass - IUD) which failed to ensure stable coal supply from the Ukrainian companies and did not find alternatives in Russia.

While iron and steel oligarchs that in parallel own coke and steel companies have a possibility to save on coke by purchasing it in Russia, long distance logistics seems to be incompatible with lucrative cooperation. However in summer 2007 Russian Railroads OJSC reduced the number of carriages used for coal delivery from Kusbas (Russia) to Ukraine, which cut its import by 10%. Russian financial and industrial groups benefited from this situation, as the Ukrainian companies obtained proposals to buy more coke rather than coal from Russia. IUD corporation was the one who suffered the most from the conflict with Russian Railroads in the result of which it had to change the markets where it purchased inputs for coke production.

Alchevskkoks started importing coking coal from the USA in 2007. In 2008 Alchevskkoks intends to import about 1.5 million tons of coking coal. Increase in coal import from abroad by sea has its own impediments due to the lack of deep-water ports able to accept the vessels with up to 100 thousand tones deadweight. Thus coal for Alchevskkoks is supplied by large- capacity vessels to Romanian Constantsa port and then reloaded to low-tonage ships with carrying capacity of 20-30 tons to be delivered to Mariupol port. This route of coal supply increases its cost dramatically and is economically feasible only in case coal prices remain high in the Ukrainian market (USD 380-400 per ton).

Reducing in the Ukrainian coal output is likely to deprive the domestic coke companies of their key competitive advantage - closeness to the raw material, and 1/3 of coke producers will be forced to leave the market. The most vulnerable will be small coke enterprises with the most obsolete capacities.

The death rate in Ukraine's mines started rising sharply when the government, after gaining independence from the Soviet Union in 1991, slashed subsidies to the industry. The country's mines today are considered among the world's most dangerous as hundreds of coal miners are dying in industrial accidents in Ukraine every year. It is generally believed that the very bad discipline is to blame. The safety regulations are permanently being undermined because the pit owners aim at maintaining production levels at any cost while miners do not take proper care of themselves seeking increase in personal output.

Outdated equipment and widespread disregard for safety rules have been blamed for the accidents, which claimed 318 lives last year and at least 140 so far this year. At the end of 2007 explosion at the one of Ukraine's largest mines - Zasyadko, employing 10,000 people and producing up to 10,000 tones of coal per day attracted attention to the question of miners' payroll accounting which currently depends on output. Investigation of the accident showed that miners are not interested in compliance with safety regulations as it leads to increase in downtime and consequently lessen their earnings. When the new government came to power shortly after the tragedy it initiated a set of actions aimed at improvement of coal sector safety. In addition to usual fruitless repressions against pit managers appeared an idea to replace efficiency wage for miners with hourly wage, which is thought to improve motivation for observance of safety standards. The process of the new law adoption was slow until the new explosion on 8 June 2008 at the Karl Marx mine in the Donetsk region.

After that the Ministry of coal industry introduced hourly wage as an experiment at seven mines around the country. The experiment is to continue three months and will be followed by its results analysis with possible recommendations to spread the practice to other mines.

The reason for the process to be so slow is in demands for increase in coal extraction combined with inefficient investments in the sector which is incompatible with safety reforms at mines.