Abstract

Содержание

- Introduction

- 1. Review of research and development

- 2. Theoretical and methodological bases of accounting of intangible assets

- 3. Organization of intangible assets accounting

- Conclusion

- References

Introduction

Relevance of the research topic. Recently, considerable attention has been paid to the use of intangible assets in the economic activity of the enterprise as a potential source of economic benefits. Intellectual property is a relatively new object of accounting, which is due to non-material nature, features of legal protection and its reflection in the composition of assets. A significant part of intellectual property objects only begins to be participants in the economic turnover, which requires constant revision and improvement of the accounting methods in order to take into account the diversity and heterogeneity of the objects. At all levels of management, it is noted about the need for innovative development of the economy of the republic and the use of products of intellectual labor as a tool for increasing production efficiency. At the moment, there are problems of defining intellectual property rights, in particular, the problem of their accounting at the enterprise, so this topic is relevant.

The purpose of the study is to identify problems, deficiencies and contradictions in accounting and audit of intangible assets and develop recommendations for improving the accounting of intangible assets.

1. Review of research and development

Intangible assets are one of the main prerequisites for the growth of competitiveness of domestic enterprises in the context of the orientation of the world economy on the strategy of innovative development. The novelty of this object of accounting predetermines the emergence of a number of issues requiring clarification. The development of the theory and practice of accounting for intangible assets is devoted to the work of many researchers, among which there are foreign founding scientists: Sveby, Kaplan, Norton, Edvinson; scientists who studied the methodology of using intangible assets: P. Drucker, H. Itami, I. Nonaka, H. Tekeuchi, T. Stewart, T. Davenport, G. Jogha, V. Matveeva, I. Tkachenko, F. Efimova, O . Kendyukhov, E. Bobrova, N. Knukhova, I. Pavlyuk, G. Nashker, F. Butinz, A. Lavrov, L. Kotenka, S. Polenov, E. Annenkova, E. Mizikovsky.

At the same time, profound and comprehensive theoretical studies in this field with a complex analysis of both domestic and international accounting practices are rare, and sometimes even completely absent. In most of the works, a critical analysis of the existing theoretical and methodological foundations and practical multidimensionality of accounting for this type of assets is given inadequately, insufficient attention is paid to improving the methodology and practice of accounting for intangible assets. It is advisable to note that in the scientific literature there is no uniform approach to the interpretation of the category of intangible assets.

So, Lishilenko A.V. distinguishes between the concepts of intangible resources and intangible assets. Where, intangible assets are access to the author's property rights, which are protected by rights, "which in themselves are intangible assets". Intangible resources are an integral part of the enterprise's potential, which can provide economic benefits for a relatively long period [1].

By the definition of AI Koblyanskaya, the term "intangible assets" encompasses any disembodied objects (their circle remains inexhaustible), which can be capitalized by the enterprise, organization, institution [2].

Butinets F.F. emphasizes that the peculiarity of intangible assets is the absence of physical substance [3].

I.A. Blank defines intangible assets as non-current assets that do not have material form and ensure the implementation of all major types of economic activities [5].

M.S. Pushkar, G.P. Zhuravl and V.G. Miller argue that intangible assets are the cost of documented rights to use land, water, other natural resources, as well as patents, copyrights and trademarks, computer software, and so on [6].

2. Theoretical and methodological bases of accounting of intangible assets

The main provisions for the organization of accounting for intangible assets are laid down in P(S)BU 8 and IAS 38 [8, 9].

In accordance with clause 4 P(S)BU 8, an intangible asset is a non-monetary asset that has no material form can be identified [8].

Under IAS 38, an intangible asset is an identifiable non-monetary asset that does not have a physical form [9].

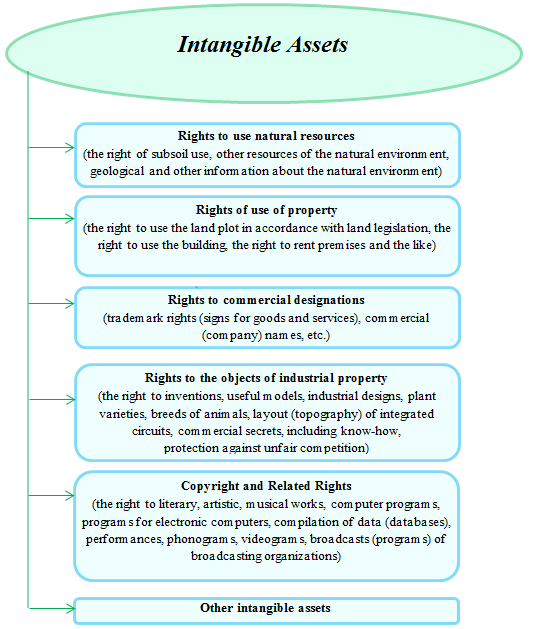

According to P(S)BU 8 accounting of intangible assets is conducted relative to each object in 6 groups. These groups are shown in figure 1.

Figure 1 – Classification of intangible assets

3. Organization of intangible assets accounting

Documentary processing of transactions with intangible assets is carried out using the standard forms approved by Order № 732. There are four standard forms approved [10] [10].

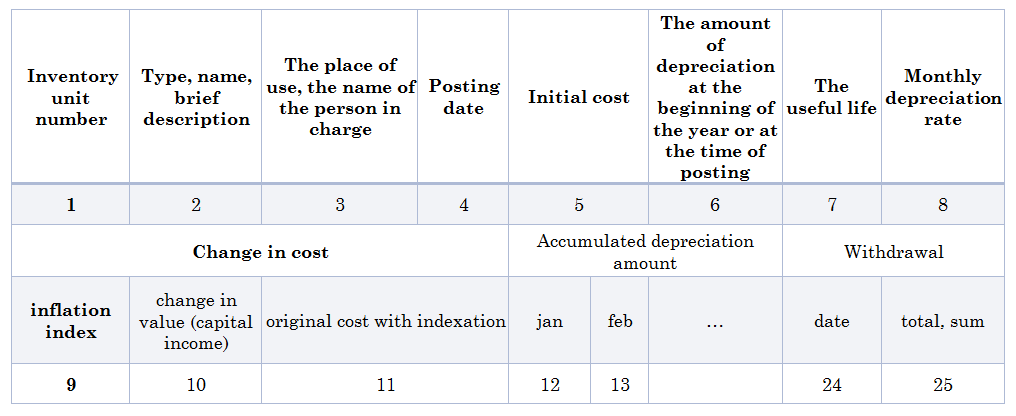

Also, for accounting for intangible assets, a statement of intangible assets, accrued depreciation (depreciation), which is shown in Figure 2, can be used.

Figure 2 – Statement of accounting for intangible assets, accrued depreciation (depreciation)

Synthetic accounting of intangible assets is maintained on account 12 "Intangible assets".

The document turnover on accounting for the received intangible assets is presented in Figure 3.

Figure 3 – Document circulation on accounting of the received intangible assets

Conclusion

Based on the generalization of the approaches of domestic and foreign scientific schools to the definition of the essence of intangible assets, it is proved that intangible assets as an economic and accounting category are characterized by such basic interdependent and interrelated components as: the lack of a material-material (physical) structure; utility in the realization of the goals for the production of products (provision of services, performance of work) and in the management of the firm (enterprise) itself; the possibility of making a profit not only at a certain point in time, but also in future periods of economic activity. Interpretation of intangible assets as an economic category is broader than an accounting object, since intangible assets today include a number of objects that can not be identified as an asset in accordance with the requirements of financial accounting (because of the impossibility of separation from the enterprise or individual, the difficulty in assessing and t. n).

References

- Лишиленко, А. В. Бухгалтерский учет [Текст]: учебник / А. В. Лишиленко. – К. : ЦНЛ, 2005. – 632 c

- Кобылянский В. Право пользования землей в Украине // Все о бухгалтерском учете. - 2006. - № 45 (712). - С.17-22.

- Бутынец Ф.Ф. Аудит: Учебник. - Житомир: Рута, 2006. - 672 с

- Балабанов И.Т. Основы финансового менеджмента. Как управлять капиталом? - М.: Финансы и статистика, 2010. - 363 с.

- Бланк И.А. Финансовый менеджмент: Учебный курс. - К.: Ника-Центр, 2008. - 528 с.

- Пушкарь, Н. С. Финансовый учет [Текст] : учебник / М.С. Пушкарь. – Тернополь : Карт – бланш, 2002. – 628 c.

- Бухгалтерский учёт: Учебник/ Под ред.П.С. Безруких. - 2-е изд., перераб. и доп. - М.: Бухгалтерский учет, 2009. - 576 с.

- Положение (стандарт) бухгалтерского учета 8 «Нематериальные активы», утв. Приказом Министерства финансов Украины от 18.10.99 г. № 242 [Электронный ресурс]. - Режим доступа: http://search.ligazakon.ua/l_doc2.nsf/link1/REG4043.html

- Международный стандарт бухгалтерского учета 38 «Нематериальные активы». [Электронный ресурс]. - Режим доступа: buhgalter911.com/Res/MSBO/MSBO38_01012015.pdf

- Приказ Минфина Украины от 22.11.2004 № 732 «Об утверждении типовых форм первичного учета объектов права интеллектуальной собственности в составе нематериальных активов» [Электронный ресурс]. – Режим доступа: http://search.ligazakon.ua/l_doc2.nsf/link1/RE10179.html

- Инструкция об использовании Плана счетов бухгалтерского учета активов, капитала, обязательств и хозяйственных операций предприятий и организаций, утвержденное приказом Министерства финансов Украины от 30.11.1999 г. №291 (с изменениями и дополнениями). Режим доступа: http://search.ligazakon.ua/l_doc2.nsf/link1/REG4186.html

- Международный стандарт бухгалтерского учета 38 «Нематериальные активы». [Электронный ресурс]. - Режим доступа: buhgalter911.com/Res/MSBO/MSBO38_01012015.pdf