Abstract

Content

- Introduction

- 1. Theme urgency

- 2. Goal and tasks of the research

- 3. Analysis of land legislation on monetary valuation

- 4.Standard monetary valuation in GIS

- Conclusion

- References

Introduction

Land as the basis of economic, social, industrial and other activities has a cost, and an adequate assessment of land is one of the important conditions for the normal functioning and formation of the economy. A significant role in shaping the sustainable development of this sphere is played by the creation of land resource assessment methodologies that can take into account all the spe-cific factors of land issues.

1. Theme urgency

The relevance of the topic is the development of technology for the mon-etary valuation of land in settlements, as well as the search for appropriate principles of market relations approaches to the practical implementation of cadastral valuation of land in the DPR.

The topic of work fits into the scientific research of the Geoinformatics and Geodesy Department of DonNTU. For example, at the Department of Geoinformatics and Geodesy for more than 10 years, research has been con-ducted aimed at improving the methods and technologies of regulatory mone-tary valuation of land for taxation. To date, according to the results of these studies, 2 Ph. D. and more than 10 master’s theses have been defended (Krivo-bokov MG, Kuz-netsova DS, Revdannik DA, Chayka AG, Chesnokova MA, Supenko S .S. And others.).

2. Goal and tasks of the research

The purpose of the work is the creation of new and application of stand-ard geographic information system tools for automating the process of regula-tory monetary valuation (RMV) of land in small and medium-sized settle-ments.

Tasks:

The result of the master’s work should be a new technology, based on the ArcGIS 10.2 platform, which will significantly reduce labor costs and reduce appraisers errors.

The use of land in the DPR is paid. Payment for land is charged in the form of land tax or rent, determined depending on the regulatory monetary value of land, the accuracy of which depends largely on the quality of the ini-tial information.

3. Analysis of land legislation on monetary valuation

In accordance with the «Provisional Regulation on the Tax System of the DPR,» prior to the adoption of the relevant regulatory legal documents, the calculation of land charges, submission of reports and payment of land charges in the country is carried out in accordance with the requirements and rates (taking into account the established benefits and peculiarities) the tax system of Ukraine as of 01/01/2014 [3].

At the same time, the annual indexation of RMV of lands, provided for by art. 138 Law of the DPR «On the tax system», until 01/01/2019 is not im-plemented.

RMV indexation coefficient of land for which the normative monetary value of agricultural land, land of settlements and other non-agricultural land has been indexed, calculated in accordance with art. 138 of the DPR Law «On the tax system», as of 01/01/2017, amounted to 1,034, as of 01/01/2018, it was 1.005 [2,4].

However, when forming your own land tax system in the DPR, you must first pay attention to solving problems that exist for a long time in the land tax system:

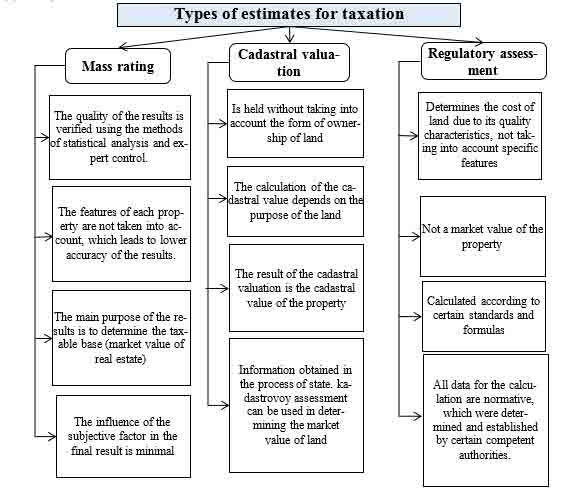

In developed countries of Western Europe and America, which have a developed market for land and real estate, a massive land valuation is applied for taxation, the mathematical model of which is based on market data. In the countries of Eastern Europe that emerged after the collapse of the USSR, vari-ous ways of mass appraisal were chosen for land assessment: cadastral (Rus-sian Federation, Belarus, etc.) and regulatory monetary valuations (Ukraine). The objective of these assessments is to determine the value of land of immov-able property for the creation and operation of a unified taxation system for all real estate objects, in particular, land (fig.1) [7].

Figure 1 – Types of estimates for taxation

To substantiate the choice of the theoretical base of the monetary valuation of land in the Donetsk region, the results of which will be used for taxation, an analy-sis was made of the existing types of land valuations and their peculiarities were revealed.

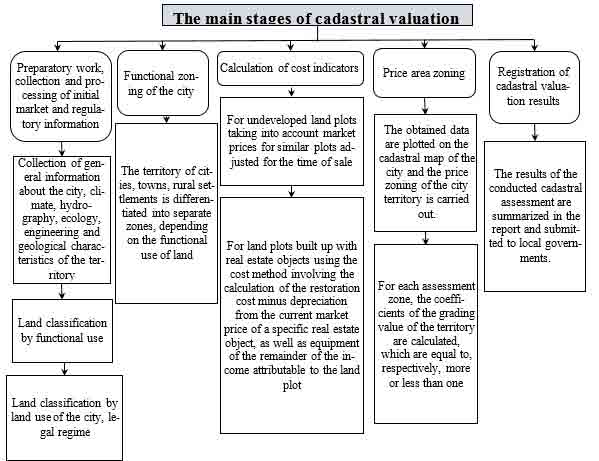

We begin with a discussion of mass valuation methods in the framework of a comparative approach (fig. 2). Ideally, this method should look like this. Suppose land plots are estimated that are close in location and are identical in basic charac-teristics. For such an assessment, within the framework of the comparative ap-proach, it is necessary to have some statistics on sales of similar objects due to the fact that the land plots that are identical in their basic parameters differed in area and location. So, the average value (or median) of these prices can be viewed as a mass estimate, and the process of obtaining this estimate is the method (more pre-cisely, one of the methods) of mass estimation. Thus, in the methods of mass esti-mation, the individual features of the object, the uniqueness of each of them are ignored, and the conclusions obtained (for example, the specific cost) equally apply to each of the objects from this group.

Figure 2 – The main stages of mass assessment

Currently, to determine the cadastral value of land and other real estate objects, mass valuation methods are used based on a sample of data on sales of land plots and other real estate in the entire territory being assessed.

The lack of a state cadastre system is associated with unjustified expenses of citi-zens, as a result of the work of the system. According to the latest changes in tax legislation, real estate tax is calculated on the basis of its cadastral value. Despite the fact that, according to the law, the cadastral value today should not exceed the market value, in practice, the valuation mechanism makes it possible to obtain an overestimated cost, which leads to a multiple tax increase [6].

This situation, in the first place, is simply unfair, since citizens and businessmen pay a tax that is too high several times, and are compelled to dispute their personal right to fair taxation for their money. Secondly, a business that owns real estate suffers greatly, and commercial real estate tax is often too high (fig. 3).

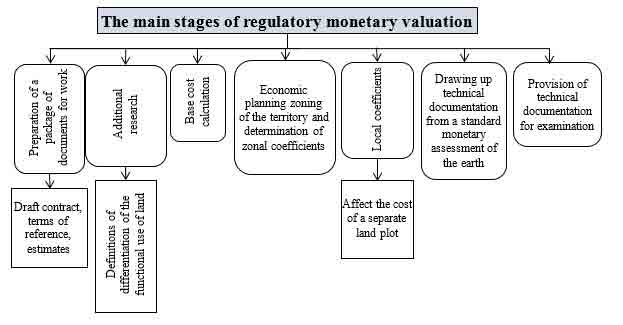

The basis of the RMV is the capitalization of rental income, obtained depending on the location of the settlement in the national, regional and local production and settlement systems, the arrangement of its territory and the quality of the land, taking into account the climatic and engineering-geological conditions, architectural and historical -cultural value, ecological condition, and functional land use (fig. 4).

Figure 3 – The main stages of cadastral valuation

Figure 4 – The main stages of regulatory monetary assessment

The introduction of mass appraisal (the experience of developed countries), based on the land market data on the territory of the DPR, is impossible due to the lack of such. In order to apply cadastral valuation (the experience of a number of countries in the post-Soviet space) on the territory of the DPR, it is necessary not only to make significant changes to a number of regulatory and legislative acts, but also to make corrections to the methodology itself.

Based on the foregoing, one should make a choice in favor of the methods of the normative monetary value of land, which is used in Ukraine. Moreover, the land legislation of Ukraine can be used in accordance with the Decree [5], which does not contradict the Declaration on the sovereignty of the Donetskaya People’s Republic and the Constitution of the DPR.

4. Standard monetary valuation in GIS

RMV of land settlements – a complex, lengthy process. Most of his time is spent on collecting initial information.

One of the ways to reduce the time of work is the automatization of the land RMV process based on geo-information technologies, for example, in ArcMAP 10.2.

The evaluation process should begin with collecting baseline data. All calcula-tions are linked to the minimum estimated unit of RMV of the land of the settlement – the estimated area with a specific location. Therefore, the project for RMV of the lands of settlements in the GIS should begin with the formation of a cartographic basis. In order for the obtained assessment results to be used for various purposes, it is recommended to work with cartographic data prepared in a single coordinate system, for example, USK-2000 or SK-63.

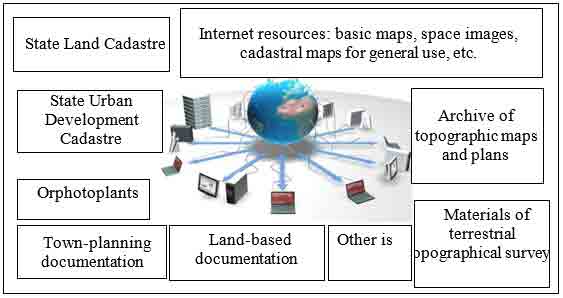

The main sources of cartographic and spatial information about the object of assessment are shown in fig.5.

The coordinates of the locality and the index-cadastral map are requested from the state land cadastre. These materials can be presented in the form of exchange files or graphic materials created in AutoCAD. In the first case, it is necessary to expand the tool base of ArcMAP 10.2 to read data from the exchange file and create a polygonal layer with drawing borders. In the second case, it is enough to import the source layer from AutoCAD to ArcMAP 10.2 and then convert the resulting layer to a Shape file [1].

Figure 5 – TSources of information for a cartographic basis of RMV of land settlements

In order to proceed with the assessment of land should create a situational scheme of the settlement with the help of information layers. Each of the infor-mation layers includes semantic information, as well as the possibility of its intro-duction in the future. In the future, with the expansion of the database, the number of information layers increases (fig. 6).

Topics are being created that relate to the economic planning zoning of the set-tlement, the areas (zones) of distribution of individual local factors, the areas of distribution of the main agricultural production groups of soils, and a cadastral map of Ukraine is also added.

In the case of updating a topographic map based on materials from orthophoto plans, land cadastre or town planning documentation, attention should be paid to linking the coordinates of the axes of streets, quarters and, in some cases, buildings and structures.

Figure 6 – SInformation layers

(animation: 6 frames, 5 cycles of repeating, 130 kilobytes)

p>

Conclusion

On the basis of the studied experience of RMV lands for taxation, a new tech-nology was proposed, based on the ArcGIS 10.2 GIS and allowing to automate the process of calculating Km2 and the formation of economic planning zones. This technology has been tested in the implementation of the RMV of the lands of Yenakiyevsk city council. Since the RMV is performed according to the legislation once every 5 years, the most time consuming process will be the assessment per-formed for the first time using the proposed technology. All further assessments at the stage of forming the initial database will include work only on updating the materials of past assessments, which significantly increases the cost-effectiveness of the assessment works.

References

- Гермонова Е.А. Мороз А.В., Буслова А.В., Подготовка картографических данных в ГИС ArcMAP 10.2 для нормативной денежной оценки земель населенных пунктов. / Донбасс будущего глазами молодых ученых. Сборник материалов научно-технической конференции. 21 ноября 2017г., с. 120-126.

- Закон «О налоговой системе» № 99-IHC от 25.12.2015, действующая редакция по состоянию на 02.11.2018.

- Временное положение о налоговой системе ДНР с изменениями и дополнениями по состоянию на 31.12.2015.

- Указ Главы Донецкой Народной Республики от 20.03.2018г. №68 «Об индексации нормативной денежной оценки земель».

- Постановление № 9-1 от 02.06.2014г. «О применении Законов на территории ДНР в переходный период».

- Райнхольд Вессели, А. В. Ланкин. Государственная кадастровая (массовая) оценка для целей налогообложения – российский и зарубежный опыт. /Экономические стратегии № 2/2008, 124-131 с.

- Палеха Ю.М., Свінарьов А.В. ГІС і оцінка земель населених пунктів // Землевпорядний вісник. – 2009. – № 20. – С. 21-26.