Abstract on the topic of the final work

This abstract is used as an example with the permission of its author, Master of DonNTU Anna Grinchenko.

Content

- Introduction

- The essence and content of expenses as an object of accounting

- The state of the problem and the legal regulation of expenses

- Objectives of improving the accounting of expenses and the formation of accounting policy

- The structure of expenses as an object of bookkeeping

- Primary cost accounting

- Analytical accounting of expenses

- Synthetic cost accounting

- Заключение

- Conclusion

Introduction

The transition to a market economy and the full independence of enterprises in solving production and economic problems has radically changed their behavior. In the current situation, the owners of enterprises, it would seem, should work to increase competitiveness both in the direction of reducing production costs and improving its quality. However, as practice shows, everything has changed to the contrary. Most of the privately owned enterprises turned out to be artificially unprofitable, which led to a significant budget deficit and an increase in inflation.

Many scientists have worked on these problems, however, today the method of cost accounting and calculating the cost of production has a number of shortcomings and inaccuracies. One of the most important shortcomings is still the integrated approach in identifying unproductive losses of material and financial resources [2].

The purpose of cost accounting and product cost calculation is to fully and reliably determine the actual costs associated with production, as well as to calculate the cost of production. The novelty of the work lies in the analysis of accounting practices to identify contradictions and inconsistencies in accounting. The paper will consider the main reasons for the occurrence of such contradictions in accounting with the development of specific recommendations for their elimination. The aim of this work is to identify these contradictions and deficiencies in cost accounting, such as accounting, expenditures on capital and current repairs, the devaluation and revaluation surplus on liquidation and sales of fixed assets, which lead to the distortion of their balance value on the example of OP "mine them. A. A. Skochinskogo" GP "DUEK".

The goal assumes the solution of such tasks as:

- consideration of the nature and content of production costs;

- reflection of the peculiarities of accounting at the enterprise for accounting for production costs, calculating the cost of production (works, services);

- reflection of primary, analytical and synthetic accounting of production costs;

- identification of the rules and features of the preparation of financial statements in the enterprise.

The object of the study is the accounting and audit of expenses. The subject of the study – methods of accounting of costs of the enterprise, the search for contradictions and inconsistencies in the accounting of expenses on the example of OP "mine them. A. A. Skochinskogo" GP "DUEK" and the definition of the objectives of improving cost study state of the problem and the legal and regulatory costs, analysis of the practice of accounting costs and auditing costs for analyzed enterprise.

The essence and content of expenses as an object of accounting

Cost accounting occupies a decisive place in the economy of the enterprise, since it is based on the economic indicators of production.

Accounting for the company's expenses is regulated by P (C)BU-16 "Expenses". According to this standard, expenses are recognized as either a decrease in the assets of an enterprise or an increase in its liabilities that lead to a decrease in the equity of the enterprise.

Expenses are recognized as expenses of a certain period at the same time as the income for which they are made is recognized. Expenses that cannot be directly related to the income of a particular period are recognized as expenses in the reporting period in which they were incurred. If an asset provides economic benefits over several reporting periods, the expense is recognized by systematically allocating its value between the corresponding reporting periods.

The value of cost accounting is in the following tasks:

- Non-admission of unjustified write-off of expenses;

- Non-admission of overestimation of the cost of products, works and services rendered;

- Cost control;

- Non-admission of unproductive expenses at the enterprise, etc.

The object of expenditure is considered to be the products, works, services or type of activity of the enterprise that require expenses related to their production. An expense element is a collection of economically homogeneous expenses.

The accounting of expenses in the enterprise can be carried out in 3 ways: using only 8 "Expenses by elements" or 9 "Expenses of activity" class of accounts, or using both 8 and 9 class of accounts.

The expenses taken into account when determining the object of taxation consist of operating expenses and other expenses. Operating expenses include the cost of goods sold, works performed, and services rendered.

All production costs are ultimately included in the cost of individual products, works, services, or groups of similar products. Administrative expenses, sales expenses, and other operating and ordinary expenses are charged to the financial result at the end of the reporting period.

The state of the problem and the legal regulation of expenses

At the present stage, the problem of reducing and correctly estimating costs is of particular relevance. The search for reserves to reduce them helps many farms to avoid bankruptcy and survive in a market economy. Consideration of this issue allows you to find out the trends in this indicator, the implementation of the plan at its level, the impact of factors on its growth, reserves, and also to assess the work of the enterprise to use the opportunities to reduce the cost of production.

The cost of production, the cost estimate, and hence the profitability, are closely related to the number of employees, its coefficients of the list composition and the structure of the staff. If the number of workers will increase rapidly compared to the change in volume of production, or decline at a slower pace, then this ratio will lead to the outpacing growth of wages compared with productivity growth, and therefore increase unit costs. A noticeable fluctuation in the cost of production, and hence profit, occurs under the influence of price growth and inflation indices. It often happens that with a decrease in the volume of output, unit costs also decrease. This is due to the outperformance of the price growth index in comparison with the inflation index. Conversely, if, along with an increase in output, there is an increase in unit costs, then this should be linked to the outstripping growth of the inflation index in comparison with prices.

A decrease in the share of depreciation in the cost price, along with a drop in production volume, leads to a sharp reduction in the depreciation fund of the enterprise, as the main source of constant and timely compensation for worn-out equipment in the required quantity and quality. In the end, this leads to increased wear and tear of the active part of fixed assets, to stagnation in the introduction of scientific and technological progress and the weakening of the material and technical base of production with all the negative consequences leading to higher costs and lower profitability, i.e. to the decline in the competitiveness of the enterprise. [1].

The methodology of accounting for expenses and the attribution of depreciation and amortisation to the cost of production was described in detail and disclosed in his work "Features of the reform of accounting for operations with fixed assets and its impact on equity" by Prof. Gavrilenko V. A. He considered the problems of attributing capital investments to the cost price, and not to current expenses, as well as accounting for the revaluation of fixed assets. He proved the illegality of comparing the concepts of capital and current repairs, as well as the illegality of attributing revaluations and capital repairs to expenses.

The organization of accounting is in inseparable unity with the system of legislative regulation. The regulatory and legal framework for cost accounting is presented in the following documents:

- Law of the Donetsk People's Republic on Accounting and Financial Reporting;

- Law of the Donetsk People's Republic on the tax system;;

- National accounting regulations (standards) ;

- Accounting regulations (standards) -16;

- Method of recommendation 373 " On the formation of the cost of production (works, services) in industry»;

- Method of recommendations on accounting for the cost of production of finished coal products

- Orders, orders concerning the organization of accounting and the application of accounting policy, which are accepted by the head of the enterprise

The legal regulation of tax relations in the Donetsk People's Republic is based on the main provisions of the DPR Legislation on taxes and fees (the Law on the DPR Tax System), orders and methodological recommendations. The legislation on taxes and fees regulates the power relations on the establishment, introduction and collection of taxes and fees in the DPR, as well as relations arising in the process of tax control, appealing against acts of tax authorities, actions (inaction) of their officials and bringing to justice for committing a tax offense.

At the enterprise level, the regulation of accounting is regulated by the provisions of the order on accounting policy. The accounting policy of each enterprise is an important step in the organization of accounting.

The main principle that must be followed when maintaining expense accounting is the principle of accrual and correspondence of income and expenses, according to which, in order to determine the financial result, it is necessary to compare the income of the reporting period with the expenses incurred to obtain these incomes. At the same time, income and expenses are recorded in accounting and reporting at the time of their occurrence, regardless of the time of receipt and payment of money.

Objectives of improving the accounting of expenses and the formation of accounting policy

The main task in improving cost accounting is to find and eliminate unproductive expenses (losses) in the enterprise. Unproductive expenses - a group of expenses that includes expenses for unproductive use of resources, payment of unproductive time costs, payment of penalties and fines, and other expenses related to this category. Non-productive expenses are fixed and included in the cost of the goods. The exclusion of this factor allows you to reduce the cost and the total price of the product.

Structure of expenses as an object of accounting

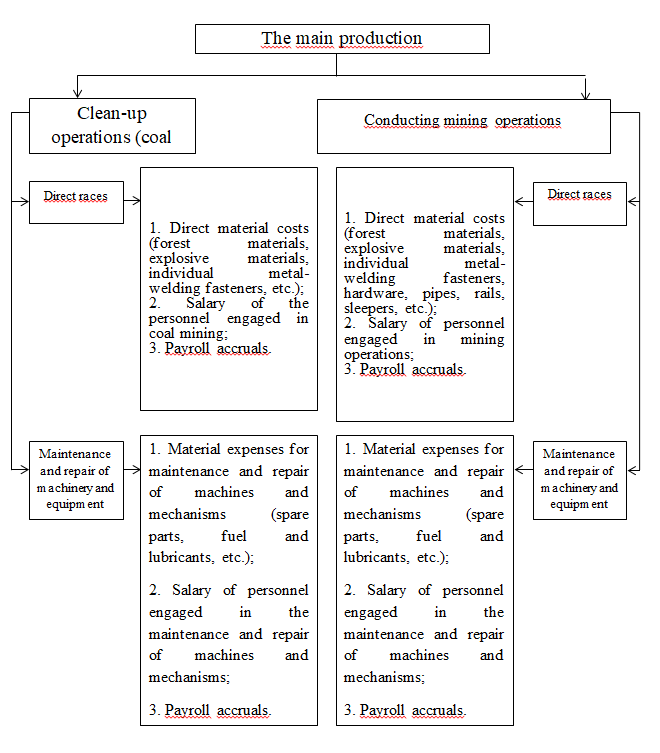

The composition of expenses as an object of accounting for each enterprise may differ. For example, the expenses of a coal mining enterprise will be the costs of the main production, which is represented by cleaning operations (coal mining) and mining operations, which will include such elements as direct material costs, wages of workers employed on the site and deductions for social activities.

- General production costs at the mine include:

- Expenses of the repair and restoration site;

- Expenses of the dust and ventilation service;

- In-house transport costs;

- Maintenance costs for trunks and lifting machines;

- Costs for maintenance of the surface;

- Expenses for other types of activities (expenses for preparation and development of production, expenses for invention and rationalization, non-capital expenses for improving production technology, expenses for improving product quality, expenses for servicing environmental activities).

Figure 1-Main production costs

Figure 2-General production costs

Primary cost accounting

- Material costs.

The accounting of expenses on materials is conducted on the basis of daily filling in by each site of primary documents on the release of materials. As a result, according to the results for the month, these documents for all sections are turned into cumulative statements for each type of material separately for this period, which are transmitted to the accounting department. On the basis of the district cumulative statements, a consolidated grouped statement of material consumption is compiled. At the same time, if the consumption of materials significantly exceeds the limit set for them, this will indicate unproductive losses of these materials [2].

- Limit-fence card (no. M-8, M-9, M-28, M-28a)

- Act-requirement for replacement (additional leave) of materials (no. M-10):

Used to account for the release of materials in excess of the established limit or when replacing materials. It is the basis for writing off materials from the warehouse. Invoice-a requirement for the release (internal movement) of materials (no. M-11). They are used to account for the movement of material values within the enterprise and their release by the economy of its enterprise located outside its territory, as well as to third-party organizations. Invoice-the requirement to be issued in two copies and signed by the chief accountant or a person authorized to do so.

- Payment for electricity, water supply and other utilities. An invoice for payment is issued after the conclusion of a written agreement between the parties, as an addendum to it, but sometimes it can also be issued as an independent document. The invoice is always issued by an employee of the accounting department. After the form is completed, the document is passed to the head of the organization, who certifies it with his signature. An invoice for payment is issued in two copies, one of which is sent to the consumer of the service or the buyer, the second remains with the organization that issued it.

- Accounting for electricity costs. The electricity consumption (at the sites) for the maintenance and repair of machines and mechanisms for all processes is determined on the basis of meter readings and established tariffs. Electricity consumption in the whole enterprise is determined by a two-part tariff. For the spent active electricity for all processes and for the declared capacity.

- Fuel cost accounting. Fuel consumption at the enterprise directly depends on the amount of output.

- Forms of primary accounting documentation for accounting for salary costs and deductions for social events: Report on time-based work:

- This document is used in the conditions of mass production on conveyor lines with a regulated rhythm of work and on production lines with a free rhythm, provided that the operations are assigned to each worker.

- Report on piecework. The production task is issued in the form of a contract for piecework for one shift or for a longer period. It indicates the amount of work and the time limits for their implementation.

- The statement of accrual of bonuses. The responsibility for filling out this paper in the vast majority of cases falls on the payroll accountant.

- A note on granting leave. This document includes all the necessary information used for calculating vacation pay and it is on the basis of it that the employee receives the vacation funds due to him by law before the vacation.

- Sick leave (Temporary disability certificate). It is used in the enterprise to determine the employee's sick pay.

Analytical accounting of expenses

The data at the end of the period is determined by adding the received materials and subtracting the dropped materials from the data at the beginning of the period. The basis of consolidated accounting is the compilation of grouping statements on the basis of which the formation of generalized indicators, such as production costs for the enterprise as a whole, takes place.

For analytical accounting of the costs of the work are summarized tabularly. In the summary tablegame the wages represented by codes that are assigned to every mind in the context of the overall structure (payment according to the processes, forms, etc.). Along with a General summary statement composed of the front tabularly for each employee, which reflects deductions for social events.

General production costs at the enterprise are divided into variable, constant. For the distribution of general production costs, first choose the distribution base. At this enterprise, the distribution base is direct material costs.

All expenses for the enterprise as a whole, regardless of which synthetic accounts they are accounted for, are reflected (collected in the context of corresponding accounts) in a single register. This Journal provides a summary of all production costs by elements and cost items. To do this, from the "Total" column of the logs 1, 2, 3, 4, 6, 7 to the Log 5, data on the costs of the enterprise is transferred, which are reflected in the corresponding registers after the construction of the logs.

When processing primary accounting documents for wages and the expenditure of material resources, entries in the cost accounting registers are made directly from the primary documents. Accrued wages, expenditure of materials, deductions for social events, and other costs are distributed in the areas of costs (by accounts, sub-accounts, items, etc.) when the data is reflected in the Journal 5. Transcript sheets can be used for distribution.

Enterprises that do not use Class 8 accounts "Expenses by elements", as part of Journal 5, keep section III "Expenses of activity". Data on line 9 "Total for section III" from column 3-16 of Journal 5 is transferred to the General Ledger. The results of the rows in columns 3-16 and in columns 18-23 (from the logs 1, 2, 3, 4, 6, 7) they are shown in the corresponding line of column 24 as actual expenses for the specified areas (items) of expenses of operational and emergency activities, and in column 25 such data are accumulated for reporting for the period from the beginning of the year. In column 2, on lines 1.1 - 1.6 of section III, enterprises indicate the objects of costs (types, groups of products, services of the main production, construction objects, auxiliary (auxiliary) production). In columns 3 and 4 of this section and sections III A and III B, enterprises can direct the expenditure of production stocks according to the amount of their accounting value and the amount of distributed transport and procurement costs.

Synthetic cost accounting

Synthetic accounting of expenses in the enterprise is represented by various types of activities. During the reporting period, transactions are made for each of these activities. The company's working correspondence accounts are presented below:.

- Coal mining (treatment works)

- Direct costs

Dt 231 "Production" Kt 20 "Raw materials and materials" - Reflects the cost of stocks (forest materials, explosive materials, individual metal-welding supports, etc.) used for coal mining (cleaning operations). Dt 231 "Production" Kt 661 "Payroll calculations" - Reflects the wages of employees engaged in coal mining. Dt 231 "Production" Kt 651 "Insurance payments" - A single social contribution is accrued for the wages of employees engaged in coal mining. Dt 231 "Production" Kt 13 "Depreciation" - Accrued depreciation of equipment used in coal mining.

- Maintenance and repair of machines and mechanisms

Dt 232 "Maintenance and repair of machines and mechanisms "Kt 20" Raw materials and materials" - Reflects the cost of stocks (spare parts, fuel and lubricants, etc.) used in the maintenance and repair of machines and mechanisms. Dt 232 "Maintenance and repair of machines and mechanisms "Kt 661 " Payroll calculations" - Reflects the wages of employees engaged in the maintenance and repair of machines and mechanisms. Dt 232 "Maintenance and repair of machines and mechanisms "Kt 651 " Insurance payments" - A single social contribution is accrued for the wages of employees engaged in the maintenance and repair of machines and mechanisms. Dt 232 "Maintenance and repair of machines and mechanisms "Kt 13 "Depreciation" - Accrued depreciation of equipment used in the maintenance and repair of machines and mechanisms.

- Direct costs

- Conducting mining operations:

- Direct costs

Dt 233 "Auxiliary areas" Kt 20 "Raw materials and materials" - Reflects the cost of stocks (forest materials, explosive materials, individual metal-welding supports, hardware, pipes, rails, sleepers, etc.) used during mining operations. Dt 233 "Auxiliary sites" Kt 661 "Payroll calculations" - Reflects the wages of employees engaged in mining operations. Dt 233 "Auxiliary sites" Kt 651 "Insurance calculations" - A single social contribution is accrued for the wages of employees engaged in mining operations. Dt 233 "Auxiliary sections" Kt 13 "Depreciation" - The depreciation of the equipment involved in carrying out mining operations is calculated.

- Maintenance and repair of machines and mechanisms

Dt 232 "Maintenance and repair of machines and mechanisms "Kt 20" Raw materials and materials" - Reflects the cost of stocks (spare parts, fuel and lubricants, etc.) used in the maintenance and repair of machines and mechanisms. Dt 232 "Maintenance and repair of machines and mechanisms "Kt 661 " Payroll calculations" - Reflects the wages of employees engaged in the maintenance and repair of machines and mechanisms. Dt 232 "Maintenance and repair of machines and mechanisms "Kt 651 " Insurance payments" - A single social contribution is accrued for the wages of employees engaged in the maintenance and repair of machines and mechanisms. Dt 232 "Maintenance and repair of machines and mechanisms "Kt 13 "Depreciation" - Accrued depreciation of equipment used in the maintenance and repair of machines and mechanisms.

- Direct costs

The main production

- Repair and restoration site (re-fastening of mine workings, repayment of mine workings (extraction of forest materials, metal-welding support, spare parts, cables, hardware, etc.):

Dt 911 "General production costs" Kt 20 "Raw materials and materials" - Reflects the cost of auxiliary materials (metal-welding supports, wooden puffs, rails, sleepers, hardware, etc.), for re-fastening of mine workings. Dt 911 "General production expenses" Kt 661 "Payroll calculations" - Reflects the wages of employees engaged in re-securing mining workings. Dt 911 "General production expenses" Kt 651 "Insurance calculations" - A single social contribution is accrued for the wages of employees engaged in re-securing mining workings. Dt 911 "General production expenses" Kt 13 "Depreciation" - The depreciation of the equipment involved in the re-fastening of mining workings, the repayment of mining workings is calculated.

- Dust-ventilation service (installation of ventilation doors, lintels, shelves, etc. facilities):

Dt 911 "General production costs" Kt 20 "Raw materials" - Reflects the cost of auxiliary materials (special spare parts, flexible ventilation staves, etc.). Dt 911 "General production expenses" Kt 661 "Payroll calculations" - Reflects the salary of employees of this service. Dt 911 "General production expenses" Kt 651 "Insurance calculations" - A single social contribution is accrued for the salary of employees of this service. Dt 911 "General production expenses" Kt 13 "Depreciation" - Accrued depreciation of equipment used in the installation of ventilation doors, lintels, shelves, etc. structures.

- In-house transport (cargo delivery, delivery of cargo, repair of machinery and equipment, maintenance of transport for the movement of goods): < p>Dt 911 "General production costs" Kt 20 "Raw materials" - Reflects the cost of auxiliary materials (replacement of individual sections of rails, switches, sleepers, etc.). Dt 911 "General production expenses" Kt 661 "Payroll calculations" - Reflects the salary of employees of this service. Dt 911 "General production expenses" Kt 651 "Insurance calculations" - A single social contribution is accrued for the salary of employees of this service. Dt 911 "General production expenses" Kt 13 "Depreciation" - Accrued depreciation of equipment involved in the delivery of goods, delivery of goods, repair work of machinery and equipment, maintenance of transport for the movement of goods.

- Maintenance of trunks and lifting machines (maintenance and repair of lifting machines, maintenance and repair of fans): < p>Dt 912 "General production costs for the repair of machinery and equipment "Kt 20 " Raw materials" - Reflects the cost of auxiliary materials for the repair of trunks (sheet metal, rails, concrete, forest materials, rubber, grouting materials, cables, pipes, etc.) Dt 912 "General production expenses for the repair of machinery and equipment "Kt 661 " Payroll calculations" - Reflects the wages of employees of this service. Dt 912 "General production expenses for the repair of machinery and equipment "Kt 651 " Insurance calculations" - A single social contribution is accrued for the salary of employees of this service. Dt 912 "General production expenses for the repair of machinery and equipment "Kt 13 "Depreciation" - Accrued depreciation of equipment involved in the maintenance and repair of lifting machines, maintenance and repair of fans.

- Surface maintenance (maintenance of various warehouses, sewage treatment plants, lamp room, all processes in the bytkombinat): < p>Dt 911 "General production costs" Kt 20 "Raw materials and materials" - Reflects the cost of auxiliary materials for trunk repairs (forest materials, spare parts, construction materials, cables, pipes, MBP, etc.) Dt 911 "General production expenses" Kt 661 "Payroll calculations" - Reflects the salary of employees of this service. Dt 911 "General production expenses" Kt 651 "Insurance calculations" - A single social contribution is accrued for the salary of employees of this service. Dt 911 "General production expenses" Kt 13 "Depreciation" - Accrued depreciation of equipment used in the maintenance of various warehouses, treatment facilities, lamp room, all processes in the bytkombinat.

- Other expenses (training of labor, damage and shortage of material values, as well as marriage within the standard, management of general production processes, production support (procurement of auxiliary materials in warehouses and their storage, etc.)): < p>Dt 911 "General production costs" Kt 20 "Raw materials and materials" - Reflects the cost of auxiliary materials for trunk repairs (forest materials, spare parts, construction materials, cables, pipes, MBP, etc.). Dt 911 "General production expenses" Kt 661 "Payroll calculations" - Reflects the salary of employees of this service. Dt 911 "General production expenses" Kt 651 "Insurance calculations" - A single social contribution is accrued for the salary of employees of this service. Dt 911 "General production expenses" Kt 13 "Depreciation" - The depreciation of the equipment involved in the training of the workforce, management of general production processes, and production support is calculated.

- Other activities (expenses for preparation and development of production, for invention and rationalization, non-capital works on improvement of production technology, for improving product quality, for servicing environmental activities): < p>Dt 913 "General production expenses for other types of activities "Kt 20" Raw materials and materials" - Reflects the cost of auxiliary materials for trunk repairs (forest materials, spare parts, construction materials, cables, pipes, MBP, etc.). Dt 913 "General production expenses for other types of activities" Kt 661 "Payroll calculations" - Reflects the salary of employees of this service. Dt 913 "General production expenses for other types of activities" Kt 651 "Insurance calculations" - A single social contribution is accrued for the salary of employees of this service. Dt 913 "General production expenses" Kt 13 "Depreciation" - Accrued depreciation of equipment involved in the preparation and development of production, non-capital work to improve production technology, maintenance of environmental activities.

General production expenses

After determining the cost of finished coal products, the cost of its sale is reflected in the following transaction: Dt 901 "Cost of finished products sold" Kt 26 "Finished products".

The main register of synthetic accounting of expenses is the general ledger. All records are kept in strict chronological order, starting in January and ending in December of the reporting year. The general ledger should contain all information on all synthetic accounts available in the enterprise (and of any form of ownership). That is, the main book is a reflection of the entire economic activity of the organization. Its main purpose is to obtain information for the preparation of the balance sheet. It includes information on incoming and outgoing balances, as well as current turnover for each individual synthetic account. Information is collected only on synthetic accounts, that is, on the current (in the reporting period) turnover of funds or property of the information. Entries are made as follows. All credit turnover is reflected in a single entry for each individual synthetic account. Debit turnover is reflected only in correspondence with the corresponding credited accounts.

After recording, the entered information is reconciled by means of the final summation. First of all, the turnover (their totals) is summed up, and second-the balance for all records. As a result, two equalities must be observed: the amounts of balances on loans and debits, as well as the amounts of turnover on loans and debits. If at least one equality is not true, then you should double-check all the information.

Conclusion

It can be concluded that the accounting of expenses in the enterprise is quite significant, since the correct assessment of expenses allows you to improve the operation of the enterprise, in general. Also, as a result of the analysis of accounting practices, it was found that there are obvious contradictions in standards 7 and 16 that require improvements, since they in some cases (accounting for current and major repairs, accounting for depreciation, markdowns, revaluations, etc.) and violate the accounting principle of "Matching income and expenses". This results in a material misstatement of the financial statements.

The list of sources

- Гавриленко В.А., Економічний аналіз діяльності промислових підприємств. Монографія. – Донецьк: ДВНЗ «ДонНТУ», 2009. – 383 с.

- Гавриленко В.А., Калькулирование себестоимости продукции на промышленных предприятиях: монография / В.А., Гавриленко. – Донецк: ГОУВПО «ДОННТУ», 2018 – 266 с.

- Гавриленко В.А., Особенности реформирования учета операций с основными средствами и его влияния на собственный капитал/Гавриленко В.А., Леонова Л.А.//Журнал «Вестник Института экономических исследований»., № 530–10/2016 – с. 5-13

- О бухгалтерском учете и финансовой отчетности [Электронный ресурс] : закон Донецкой Народной Республики № 14-ІНС от 27 фев. 2015 г. : действующ. ред. // Официальный сайт Народного Совета Донецкой Народной Республики. - Электрон. дан. - Донецк, 2015. - Режим доступа: Дата обращения: 29.05.2019. - Загл. с экрана.

- О бухгалтерском учете и финансовой отчетности [Электронный ресурс] : закон Донецкой Народной Республики № 14-ІНС от 27 фев. 2015 г. : действующ. ред. // Официальный сайт Народного Совета Донецкой Народной Республики. - Электрон. дан. - Донецк, 2015. - Режим доступа: Дата обращения: 29.05.2019. - Загл. с экрана.

- О налоговой системе [Электронный ресурс] : закон Донецкой Народной Республики № 99-ІНС от 25 дек. 2015 г. : действующ. ред. // Официальный сайт Народного Совета Донецкой Народной Республики. - Электрон. дан. - Донецк, 2015. - Режим доступа: . - Дата обращения: 29.05.2019. - Загл. с экрана.

- Об оплате труда [Электронный ресурс] : закон Донецкой Народной Республики № 19-ІНС от 6 мар. 2015 г. : действующ. ред. // Официальный сайт Народного Совета Донецкой Народной Республики. - Электрон. дан. - Донецк, 2015. - Режим доступа: - Дата обращения: 29.05.2019. - Загл. с экрана.

- Об организации бухгалтерського учета: [Электронный ресурс] приказ Министерства угля и энергетики ДНР Государственное предприятие «Донецкая угольная энергетическая компания» № 23 от 11 мар. 2016 г. : действующ. ред. // Официальный сайт Народного Совета Донецкой Народной Республики. - Электрон. дан. - Донецк, 2015. - Режим доступа: - Дата обращения: 29.05.2019. - Загл. с экрана.

- Об охране труда [Электронный ресурс] : закон Донецкой Народной Республики № 31-ІНС от 3 апр. 2015 г. : действующ. ред. // Официальный сайт Народного Совета Донецкой Народной Республики. - Электрон. дан. - Донецк, 2015. - Режим доступа: . - Дата обращения: 29.05.2019. - Загл. с экрана.

- Онищенко Т., Альбом бухгалтерских проводок/Онищенко Т., Мякота В. – 8-ме вид., перероб. і доп. – Х: Фактор, 2004 – 304 с

- П(С)БУ Положение (стандарты) бухгалтерського учета [Электронный ресурс]: сайт. – Электрон. дан. – Режим доступа: Загл. с экрана.

- Піроженко О., Як заповнити первинну документацію/О.Піроженко, В.Кузнєцов, О.Андрусь, М.Михайлицька. – 5-те вид., перероб. і доп. – Х.:Фактор, 2012 – 320 с. (серія «Як заповнити…»)