Abstract

Contents

- Introduction

- 1. Theoretical basis of risk management

- 2. Risk factors and risk management principles

- 3. Methods and tools for risk assessment and management

- Conclusion

- References

Introduction

The urgency of the research in the area of risk management at the enterprise is due to the need to develop an integrated, comprehensive approach to risk management, which is coordinated throughout the organization. The ability to effectively influence the risks enables the company to operate successfully, have financial stability, high competitiveness and stable profitability.

Based on the above, the purpose of writing this thesis is to analyze the risk management system in an enterprise operating in the market conditions.

The purpose of the study predetermined the formulation and solution of a number of interrelated tasks:

- analysis and evaluation of the existing concept of risks;

- analyze the theoretical aspects of risk assessment and risk management methods;

- to study methodological approaches in the theory of risk management at an enterprise;

- analyze existing risks and methods of risk management at the enterprise;

- to develop a complex of measures on risk management at the enterprise.

1. Theoretical basis of risk management

Risk analysis can be defined as a process of solving a complex task requiring consideration of a wide range of issues and carrying out a comprehensive study, including assessments of technical, economic, managerial, social, and in some cases, and political factors.

Risk analysis should answer the three main questions:

- What can a bad thing happen? (Identification of Hazards).

- How often can this happen? (Frequency analysis).

- What are the consequences? (Impact Analysis).

The main element of risk analysis is the identification of hazards (detection of possible hazards), which can lead to negative consequences. The most commonly understood process of risk analysis can be presented as a series of successive events.

- Planning and organization of work.

- Identification of hazards.

- Identification of hazards.

- Preliminary assessment of hazard characteristics.

- Risk assessment.

- Frequency analysis.

- Impact analysis.

- Uncertainty analysis.

- Development of risk management recommendations.

The first, from which any risk analysis begins, is the planning and organization of work.

The risk analysis is conducted in accordance with the requirements of the regulatory acts in order to ensure entry into the risk management process, but a more precise choice of tasks, means and methods of risk analysis is usually not regulated. The documents emphasize that the analysis should correspond to the complexity of the processes under consideration, the availability of the necessary data and qualifications of experts conducting the analysis. Moreover, more simple and understandable methods of analysis are preferable to more complex, not completely clear and methodically secured. Therefore, at the first stage, it is necessary to indicate the reasons and problems that caused the need for risk analysis; define the analyzed system and give its description; select the appropriate group of specialists (team) to conduct the analysis; establish sources of information about system security; specify initial data and limitations that determine the limits of risk analysis; to clearly define the objectives of risk analysis and the criteria for acceptable risk. [2]

The next stage of risk analysis is the identification of hazards. The main task - the identification (based on information about this object, the results of examination and experience of such systems) and a clear description of all the inherent dangers. This is the crucial stage of the analysis, since the risks not identified at this stage are not subject to further consideration and disappear from the field of vision.

There are a number of formal methods for identifying dangers. As a general rule, a preliminary assessment of hazards is given in order to select the further direction of the activity: to stop further analysis in view of the insignificant nature of the hazards; carry out a more detailed risk analysis; to develop recommendations for the reduction of hazards. [7].

The initial data and the results of the preliminary assessment of the hazards are duly documented. In principle, the risk analysis process can end at the stage of identification of hazards.

If necessary, after identifying the hazards, go to the risk assessment stage.

Finally, the final stage of the risk analysis of the technology system is the development of recommendations for reducing risk (risk management) in the event that the degree of risk is higher than acceptable.

According to the work carried out in this way, all normative documents prescribe the preparation of a report, the requirements for which content are strictly formulated and apply to the issues listed above.

The multiplicity of the results of the analysis and the possibility of compromise solutions give reason to believe that the analysis of risk is not always a strictly scientific process, subject to verification by objective methods.

Risk assessment is a common process of risk analysis and assessment. It is expedient to consider these two main components inseparably, since the risk assessment procedure is based on the results of the analysis and usually reduces to the definition, exceeds the acceptable acceptable (acceptable) value or not. The purpose of risk assessment is not only to obtain its quantitative or qualitative characteristics, but also to rank (compare) these characteristics, prioritize and develop solutions aimed at reducing risks. In this case, the costs and benefits of the decision are estimated. [9].

The risk forecast is his assessment at a certain point in the future, taking into account the trends in changing the risk conditions.

Fig. 1.1. Methodological apparatus for risk analysis

External risks include risks that are not directly related to the activity of the enterprise or its contact audience (social groups, legal entities and / or individuals who have a potential and (or) real interest in the activities of a particular enterprise). The level of external risks is influenced by a very large number of factors - political, economic, demographic, social, geographical, etc.

Internal risks include risks arising from the activities of the enterprise itself and its contact audience. Their level is influenced by the business activity of the enterprise management, the choice of the optimal marketing strategy, policy and tactics, and other factors: production potential, technical equipment, level of specialization, level of labor productivity, safety techniques [7]

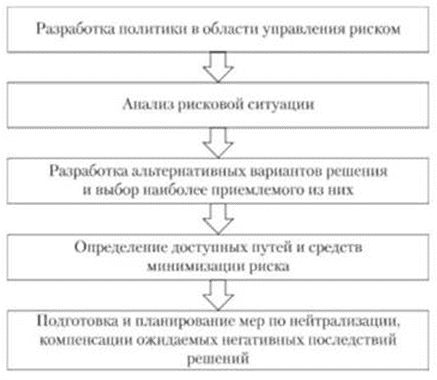

In a risk situation, the person in charge faces the need to develop alternative solutions and then choose the most appropriate one. At the same time, if the verb "risk" is associated with actions in spite of the existing dangers, neglecting them, then risk management involves analyzing the causes, sources and risk factors, realistic risk assessment on the way to the intended purpose, assessing the effectiveness of various risk management methods and at the same time Time to avoid unnecessary risk and unjustified losses. Choosing an option that minimizes risk often leads to low results. Risk management includes the following actions.

Fig. 1.2. Risk Management Action Complex

One of the first steps in risk management is to identify the risks involved. There are different risk classifications for this purpose. Classification of risks means systematizing a multitude of risks based on some features and criteria that allow the pooling of subsets of risks into more general concepts.

2. Risk factors and risk management principles

In this regard, it is very important in our opinion:

- First, the full account of external and internal factors that influence the nature of the organization of risk management at the enterprise;

- Second, the priority of individual areas of risk management development for a particular enterprise (taking into account the activity profile: financial or non-financial).li>

Among the external factors determining the organizational basis of risk management at the enterprise (price volatility, globalization of commodity and financial markets, tax asymmetry, technological achievement, etc.), in our opinion, the strengthening of the globalization factor for Russian enterprises should be highlighted. then it will lead to growth for Russian producers of competition both on the external and on the domestic (Russian) commodity markets, which inevitably will affect the growth of the degree of manifestation of various business and financial risks in their activities. The organization of risk management at a particular enterprise is naturally affected by factors of internal order, such as the need for liquidity, risk aversion, agency costs, and others. [2].

It should be noted that external and internal factors of organization of risk management at the enterprise are interconnected, that is there is a certain correlation between them. This is due to the fact that the various types of risks themselves are interconnected and interdependent.

Basic rules of risk management:

- You can not risk more than your own capital can afford.

- It is necessary to think about the consequences of the risk.

- You should not risk many for the sake of small.

- A positive decision is made only if there is no doubt.

- If there are any doubts, negative decisions are made.

- One can not think that there is always only one solution. Probably there are others [3].

The implementation of the first rule means that before deciding on a risk capital investment, it is necessary:

- determine the maximum possible amount of loss under this risk;

- compare it with the amount of capital invested;

- compare it with all of its own financial resources and determine whether this loss of capital will lead to the bankruptcy of the investor.

The amount of loss from investing capital can be equal to the volume of this capital, a little less or more of it.

3. Methods and tools for risk assessment and management

Different techniques are used to reduce the risk. The most common are:

- diversification;

- acquisition of additional information on the selection and results;

- limitation;

- self-insurance;

- insurance;

Diversification is the process of allocating investment between different capital investment objects that are not directly related to the purpose of reducing the risk and loss of income. Diversification helps to avoid a portion of risk in the distribution of capital between diverse activities.

Limiting is setting a limit, i.e. Limit amounts of expenses, sales, credit, etc. Limiting is an important measure of risk reduction and is used by banks when issuing a loan, when entering into an overdraft agreement, etc. It is used by business entities for the sale of goods on credit, loans, the determination of capital investments, etc.

Self-insurance means that an entrepreneur prefers to insure himself than to buy insurance in an insurance company. Thus he saves on the cost of capital for insurance. Self-insurance is a decentralized form of creating natural and monetary insurance (reserve) funds directly in the managing entity, especially those whose activities are at risk.

Self-insurance is logical, when the cost of insured property is relatively small in comparison with the property and financial parameters of the entire business. For example, a large corporation is not expedient to insure through its insurance company its equipment, which is installed in a small room rented by it, through an insurance company. Self-insurance also makes sense when the likelihood of a loss is extremely small, when the company owns a large amount of the same type of property. So, transnational oil companies, owning several hundred tankers, practice self-insurance. The calculation is very simple and logical: the loss of one tanker per year, which is unlikely, will cost the company less than the cost of insurance premiums for all tankers. [8].

Each of the listed risk reduction tools has both certain advantages and disadvantages. Therefore, certain combinations of these "suppression" risks are commonly used.

The final stage in the analysis of risk reduction means is the formulation of a general project risk management plan.

This plan should include: the results of the identification of all project risk areas, the list of key risk identifiers in each area; the results of the rating assessment of risk indicators reflecting their significance to achieve the objectives of the project; results of statistical analysis of risk, sensitivity analysis and global risk analysis of project acceptance; Recommended strategies for reducing risk in each area of activity associated with the implementation of the project; a list of procedures for monitoring the risks of an entrepreneurial project.

Conclusion

Organization risk management is a continuous process that covers the entire organization; carried out by its staff at all levels; used in the design and formulation of a strategy; applies throughout the organization, at each level and in each unit, and includes an analysis of the portfolio of risks at the organization level; is aimed at identifying events that may affect the organization and management of risks in such a way that they do not exceed the readiness of the organization to take risks (risk-appetite); gives the management and the board of directors an appropriate guarantee of achievement of the goals.

Specific methods and techniques that are used in making and implementing decisions under risk conditions depend to a large extent on the specifics of entrepreneurial activity, the strategy adopted to achieve the goals set, the particular situation, etc.

The risk management system first of all presupposes their estimation, the results of which allow to choose in the future the most optimal way of reducing risks. In entrepreneurship the following ways of reducing risks are most commonly used: acquisition of additional companies, companies with a well-established system of introduction of new technologies; attraction of external experts-competitors with a narrow specialization; introduction of innovations; maximize the use of past experience.

References

- Абрамов С.И. Оценка риска инвестирования.// Экономика строительства, 1996, № 12, с. 2-12.

- Балабанов И.Т. Основы финансового менеджмента. М.: Финансы и статистика, 1996, 180 с.

- Балабанов И.Т. Риск-менеджмент. – М.: Финансы и статистика, 1996.

- Бланк И.А. Стратегия и тактика управления финансами. – Киев: ИТЕМлтд, АДЕФ-Украина, 1996.

- Бачкаи Т. и др. Хозяйственный риск и методы его измерения. Пер. с венг. , М.: Экономика, 1979, 184 с.

- Градов А.П. и др. Стратегия и тактика антикризисного управления фирмой. – Спб.: Специальная литература. -1996. -510 с.

- Романов В.С. Управление рисками: этапы и методы // Факты и проблемы практики менеджмента: Материалы научно-практической конференции 30 октября 2006 г. – Киров: Изд-во Вятского ГЛУ, 2006 г. – с. 71–77

- Станиславчик Е.Н. Риск-менеджмент на предприятии. Теория и практика. М.: «Ось-89», 2002. – 80 с.

- 9. Хохлов Н.В. Управление риском. – М.: Юнити-дана, 1999. – 239 с.