Abstract

Content

- Introduction

- 1. Theme urgency

- 2. Goal and tasks of the research

- 3. Economic essence and structure of circulating assets in mine conditions

- Conclusion

- References

Introduction

The formation and development of a market economy are inextricably linked to the search for fundamentally new methods of production organization and management.

To date, the problem of economic justification of ways to improve the efficiency of coal mines on the basis of a more rational use of working capital is of particular importance. The place of the enterprise in industrial production, its financial condition, and competitiveness in the market depend on the solution of this problem.

A prerequisite for maintaining the continuity of the enterprise is the constant availability of working capital in the production sector, which includes inventories, work in progress and deferred expenses. For the implementation of the production process, the mine must have in the right amount of supplies of auxiliary materials, spare parts, fuel, workwear, household equipment, etc. At the same time, a shortage of inventories can lead to interruptions in production and business activities. However, their quantity should not be overestimated, since surplus inventories can lead to freezing of funds that could be used for other purposes. Expenses for the maintenance of specially equipped premises and the remuneration of special staff are increasing. There is also a constant risk of losses due to possible damage or theft of material assets. Therefore, an important aspect of the enterprise’s activity is an established mechanism for organizing accounting and control of inventories at the enterprise, starting with their planning and ending with their use in the process of economic activity.

In the vast majority of enterprises, the organization of accounting for working capital assets has not yet formed as an integrated system of collecting information, analyzing it, planning and providing internal users of the enterprise with the aim of making operational, tactical and strategic decisions on its basis. There is no single methodology for the formation of a mechanism for organizing the accounting and management of current assets as a system. The development of such a mechanism will free up additional financial resources of the enterprise, make it more competitive, which determines the relevance of this research work.

1. Theme urgency

One of the factors for the smooth functioning of the mine, as well as the provision of non-distorted financial statements, is an effective system of accounting for working capital in the production sphere, in particular, inventories.

The regulation of the accounting for working capital is mainly carried out on the basis of legislative acts, which disclose the essence of the concepts of current assets

and reserves

, give definitions of work in progress, expenses for future periods. The methodological foundations of the formation of accounting information on working capital and its disclosure in the financial statements are also determined.

As can be seen from the above, there are a sufficient number of regulatory acts accounting. But, despite this fact, in the current accounting system, there are a number of shortcomings that attract the attention of many scientists who offer methods for improving the display of accounting information on working capital in the production sphere.

2. Goal and tasks of the research

Identification of shortcomings and contradictions in the accounting of current assets in the production sector and the development of specific recommendations for its improvement is the goal of research.

Main tasks of the research:

- Search for the most accurate definitions of the concepts of

inventories

,work in progress

. - Identification of methods for determining the normative and actual value of stocks at the enterprise to ensure uninterrupted operation.

- Proposal of the most appropriate approach to determining the value of work in progress.

- Analysis of accounting features for deferred expenses.

- Identification of deficiencies in the accounting of current assets in the production sphere through audit and development of recommendations for its improvement.

Research object: financial and economic activities of mining enterprises.

Research subject: set of theoretical, methodological and practical aspects of current assets accounting.

3. Economic essence and structure of circulating assets in mine conditions

Working capital is the amount of material assets, which is reflected in the accounting on average for each day of the enterprise.

Working capital in the field of production, as a rule, is represented by the following categories: inventories, low-value wearing items, work in progress, semi-finished products of their own manufacture and expenses for future periods [1].

Coal mining is not carried out at the mine, as a result of which there is no accounting for work in progress and semi-finished products of own manufacture.

The largest share in the structure of working capital in the production sector at coal mines is accounted for by inventories, namely: auxiliary materials and spare parts that do not materially and materially form finished products, but contribute to the implementation of the technological process.

In this regard, it is advisable to pay more attention to the category of inventories and consider it by process.

The activities of the mine are represented by the basic and general production processes. The main processes of the mine are represented by a treatment excavation and preparatory workings. For their implementation, a large number of auxiliary materials are needed.

The extraction of minerals can be carried out manually (by kayles), using simple mechanisms (jackhammers), drilling and blasting operations, and excavating machines. When conducting cleaning operations in the face, auxiliary materials are used: wood (for fixing the bottomhole space), explosives (for separating the rock mass), fuel (for servicing mining and local transport equipment), spare parts (to ensure the working condition of local equipment) [1, 3].

At the preparatory work site during mining, explosives, detonators, cords are used for drilling and blasting operations; forest materials for the construction of temporary lining; metal and reinforced concrete arch supports, puffs for permanent fastening of mine workings; spare parts for equipment repair; fuels and lubricants for maintenance of equipment.

The group of general production processes includes: ventilation, surface work, mine transport and repair and restoration site [4].

The following production stocks are used at the ventilation section, which supplies clean and contaminated air to underground mine workings: ventilation pipes for forced ventilation, spare parts for maintaining the ventilation section equipment (fans, electric motors, etc.), fuel and lubricants for equipment maintenance.

Elements of arch support for the replacement of those damaged under the influence of rock pressure, rails during repair of the rail track, ventilation and hydraulic pipes, cable, fuels and lubricants for maintenance of mine workings are used at the site of belt-restoration work.

For each process, it is necessary to determine the need for material resources, taking into account their nomenclature, sizes, and quality. After determining the need, you need to organize the receipt of the necessary material assets in various ways. The company continuously monitors the movement of inventories taking into account their income, retirement, internal movement. Particular attention should be paid to the change in the value of inventories due to their reuse, since when redeeming mining or replacing parts of metal equipment, most of the material assets can be restored [6].

Low-value wearing items in the conditions of the mine are represented by overalls, safety shoes, personal protective equipment, various tools and devices. At the enterprise, it is important to correctly determine the need for such material values, as well as correctly carry out their accounting both in the warehouse and in production, and in accounting [7].

A prerequisite for improving the operation of the mine is the availability of deferred expenses that have their own characteristics of formation and write-off.

Thus, there are a number of issues for each element of current assets in the production sector. Elements of the working capital of the mine are presented in Figure 1:

Figure 1 – The structure of the working capital in production

(animation: 7 frames, continuous repetition, 32.63 kilobytes)

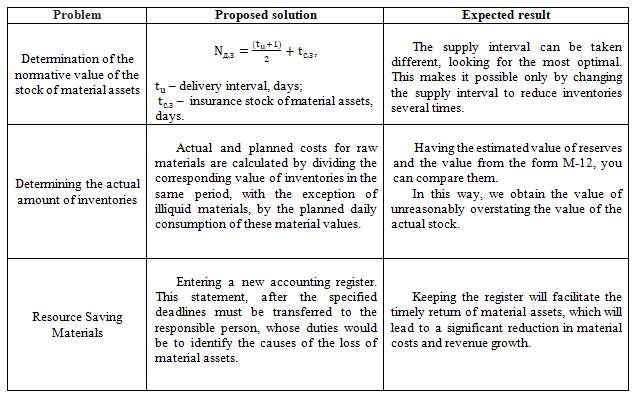

As a result of the analysis of all these problems, it is supposed to solve the most important problems in our opinion, namely: determining the normative and actual values of inventories, imperfection of the system of reuse of values. The developments on these issues are presented in Figure 2:

Figure 2 – Analysis of the working capital problems in the production sector

Conclusion

In the framework of this work, the economic essence of the current assets of a coal enterprise was investigated, regulatory legal regulation, as well as accounting features of these assets were considered.

Thus, working capital in the production sector once participates in the production process and fully transfers its value to the manufactured products.

Production working capital includes the following components: inventories, low-value and wearing items, work in progress, semi-finished products of our own manufacture and expenses for future periods.

As studies have shown, there are many problematic issues in organizing the accounting of working capital in the production sphere, among them: determining needs, setting standards, organizing the accounting and storage of resources, resource conservation and others. With due attention to each of them, it is possible to significantly optimize the work of the enterprise and increase the efficiency of its work.

At present, the features of accounting for deferred expenses and the audit of current assets are poorly studied. Master's work is not yet completed. Final completion: summer 2020. The full text of the work and materials on the topic can be obtained from the author or his leader after the specified date.

References

- Гавриленко, В. А. Экономический анализ деятельности промышленных предприятий: монография / В. А. Гавриленко. – Донецк: ДВНЗ

ДонНТУ

. – 2009. – 383 с. - Чуев, И. Н. Комплексный экономический анализ хозяйственной деятельности / И. Н. Чуев, Л. Н. Чуева. – М.:Дашков и Ко. – 2009. – 368 с.

- Юркова, І. М. Класифікація виробничих запасів на вугледобувних підприємствах / І. М. Юркова // Економічний форум. – 2013.– Вип. 3. – С. 217-223.

- Бутинець, Ф. Ф., та ін. Бухгалтерський управлінський облік: навч. пос. – Житомир: ЖІТІ. – 2000. – 567с.

- Сопкo, В. В. Бухгалтерський облік: Навчальний посібник для студентів спеціальності

Облік і аудит

вищих навчальних закладів / В. В. Сопко. – Тернопіль: Астон. – 2005. – 496 с. - Миронова, Ю. Ю. Облік незавершеного виробництва на підприємстві / Ю. Ю. Миронова // Журнал

Облік і аудит

. – 2011.– Вип. 7. – С. 97-99. - Данилевич, Е. А. Бухгалтерский учет в горной промышленности: учебник / Е. А. Данилевич, С. И. Уткина, Л. М. Гуменюк. – Москва: Недра. – 1988. – 222с.