Содержание

Introduction

Actuality. In the conditions of market economy the basic in activity of each enterprise is receiving the maximum profit. With competition development in the market and decrease in rate of return of prospect of development of the enterprise substantially depend on behavior of expenses and management of them. Ability is systematic and rational to operate expenses during the periods of deterioration of an environment increases chances of a survival.

Research of effective management by expenses especially important in the conditions of inflation as data on present expenses need to be verified with data on future expenses. Level of expenses is not only a key indicator of assesment of the work of each concrete enterprise, but also a national economy as a whole. Therefore today when the national economy is in quite serious condition, researches of questions of management by expenses of the industrial enterprise is the extremely actual.

In the conditions of formation of the market relations in Ukraine continuous search and use of the most rational and effective forms and methods of control over expenses is carried out. Creation and development in practice of new nonconventional systems of obtaining information on expenses and results of a production activity, application of new approaches and planning methods, accounting, the account and control provide possibility of the solution of many problems of effective management with the modern enterprise. In a control system of expenses the foreground occupies a choice of a method of development of accounting by means of which the managing subject distributes expenses, analyzes their influence on results of economic activity, and also forms the price and defines price policy of the enterprise.

Work purpose: development of theoretical bases and methodical approaches to management of expenses at the enterprise.

Problems of work. For achievement of the purpose in work the following tasks are put:

— to consider essence and types of expenses which arise in the course of economic activity of the enterprise;

— to reveal essence of prime cost and its structure;

— to define essence of concept «management of expenses» and its urgency in modern operating conditions of the enterprise.

— to analyze the main methods of management;

— to carry out the analysis of features of methods of control over expenses;

— to prove a system approach to management of expenses;

— to offer economic-mathematical model on optimization of expenses at the enterprise;

— to consider and specify a method of the analysis of expediency of expenses;

— to analyze forecasting of expenses of the enterprise.

Object of work: management of enterprise activity.

Work subject: theoretical principles and methodical approaches to management of enterprise expenses.

Analysis of researches. Theoretical and methodical approaches of management of expenses at the enterprise were considered by many scientists - economists, such as Krapivnitsky Page of N, Bakanov M. I., Yu.S Tsal-Tsalko., Turilo A.M., Turila M. M., Greshchak M. G., Kotsyuba of Ampere-second., Great Yu.M., Prokhorov V. V., A.V Skull., Partin G. A., Panasyuk V. M., Pokropivny S. F., Yefimov F. F., etc.

Research methods: As a theoretical and methodological basis of a master's thesis fundamental provisions of the economic theory, scientific works and methodical development of leading domestic and foreign scientists in the field of management of expenses at the enterprise served. In the course of work the following methods were used: an induction and deduction (at definition «management of expenses»), the analysis and synthesis, classification; approaches: information (the analysis of sources of information), a system principle of interrelation with environment, research of expenses as difficult it is complete - economic system (in justification of concepts), a process approach. Information base of research are standard and acts of Ukraine, general provisions of scientific works of domestic and foreign scientists within a studied subject, express information of Goskomstat of Ukraine, materials of research conferences, periodicals and the Internet network.

Scientific result of research: theoretical and methodical justification of questions of management by expenses and processes of optimization of expenses at the enterprise.

Approbation of results of work. The basic scientific and practical provisions of work were presented at all Ukraine scientific and practical conferences: conference of students and young scientists «Modern problems of management of investment and innovative activity» in 2011-2012, «Actual problems of development of financial and credit system of Ukraine» in 2011, «Donbass - 2020: prospects of development by eyes of young scientists» in 2012.

Main content of work

In introduction the actuality of a subject of a master's thesis is considered, the research objective, object, a subject and research methods are given, practical value of results reveals.

In the first section of work «Theoretical bases of management expenses» consider essence of concept of expenses, prime costs and managements of expenses, statistical information on Ukraine also is analyzed.

The category "costs" is widely used both in domestic, and in foreign economic literature. Treatment of expenses it is possible to find in works of economists Millya Dzh., Valrasa, L., Viewfinder Ф., Uiksteda F., Knight F. [24], Bakanova M. I. [11 , page 135], Friedman A.M. [12 , page 270], Butintsa F.F. [13 , page 456], Yu.S Tsal-Tsalko. [25 , page 160], Krapivnitsky Page of M [26], etc.

Therefore it is possible to draw a conclusion that expenses is value terms of absolute size of the consumed resources necessary for implementation of production economic activity of the enterprise and achievement by him for a goal, this concept which are characteristic for activity of any enterprise or the organization, legal or the individual.

Proceeding from opinions of economists (Druri K. [15 , page 25], Village F Heads. [16 , page 43], the Pole of B. [14 , page 60], Greshchak M. G., the Lake Kotsyuba of Page [3 , page 42], and Karpov Other [17 , page 118]) classification signs can be the following:

1) costs for adoption of administrative decisions and planning;

2) costs for control and activity regulation;

3) costs for determination of prime cost;

4) the costs connected with sale of production and its production.

According to the current legislation [4] and to a methodological approaches to formation of production expenses for production manufacturing (rendering of services or works) the concrete enterprise define expenses of usual activity and extreme. To expenses of usual activity carry «Operational expenses».

Operational expenses include such economic elements:

— labor costs;

— assignments on social actions;

— material inputs;

— amortization;

— other operational expenses. [2 , page 40]

The structure of operational expenses on elements for January-November, 2011 is presented in the circular chart (fig. 1)

Fig. 1 – Structure of operational costs on elements

Classification of costs by articles of accounting and economic elements has extremely great value for activity of the enterprises and the organizations. [2 , pages 43] are given In tab. 1 the main calculation articles.

Table 1 - Classification of costs by accounting articles

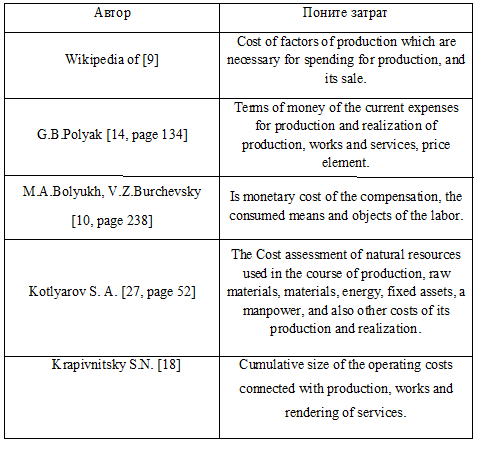

One important indicator characterizing work of the enterprise, product cost, works, services is. Financial results of activity of the enterprise, rates of expanded reproduction, a financial condition of subjects of managing depend on its level. [7] Concept of prime cost study and many scientists studied. They made a rich contribution to an economic science and in general received many positive results. Treatment of product cost are presented in tab. 2.

Table 2– Essence of concept of prime cost

Therefore it is possible to draw a conclusion that prime cost is a complex economic indicator which unites in itself expenses of the generalized work, i.e. costs of the consumed means of production, and expenses of live work, i.e. costs of a salary of employees of the enterprises, and also a part of a net profit of the citizens, intended on social insurance, support of victims of Chernobyl failure, the maintenance of pensioners, the unemployed and medical insurance.

According to statistical data on Ukraine positive dynamics on increase in gross profit in economy branches on 25458,5 million UAH is accurately traced. or for 64,68 % in comparison with 2010. Growth in the industry makes 24382,9 million UAH., that is growth rates in comparison with 2010 made 19,4 %. Such indicators, as trade and car repairs also increased by 27,83 %; wholesale trade, activity of hotels of restaurants, transport of communication and financial activity for 24,77 %, 29,8 %, 2,13 % and 149,75 % respectively. But in comparison with it worsened in such branches of economy of Ukraine, as trade in cars and motorcycles, retail trade, providing municipal and individual services, culture and sports. Profit in the field of health care of protection and providing the social help decreased by 56,14 %. All this can be investigated on fig. 2 [8].

Fig. 2 – Profit (loss) for January-August 2011

On a profit level considerable influence renders a rate of inflation and a price level.

The problems connected with management of expenses of the enterprises, are shined in scientific works, both domestic scientists, and foreign scientists-economists: Butinets F.F. [13 , page 270], Village F Head. [16 , page 75], Druri K. [15 , page 105], Turilo A.M., Turilo A.A. [19 , page 16]. They define management of expenses, as systematic formation of expenses for production and sale of production and control of their level. Also such, as Yasinsky A.I. [8], Partin G. A. [20 , page 31], Greshchak M. G., Kotsyuba of Ampere-second. [19 , page 230] and others.

The concept "management" means the activity of the enterprise (organization) directed on realization of the purposes of object of management under condition of rational use of available resources. Interrelation of functions of management it is shown on fig. 3.

Fig. 3 – Interrelation of functions of management (volum 154Кб, 5 frames, size 14,7 КБ, 5 cycles of repetition)

In tab. 3 some opinions of scientists-economists concerning essence of concept «management of expenses» are presented.

Table 3 - Definition of economic essence of «management of costs»

Costs management - process of purposeful formation of expenses by their types, places and carriers of continuous control of level of expenses and stimulations of their decrease.

In the second section «Development of methodical base of management by expenses» the main methods of management and methods of control over expenses are considered and specified, and also is proved a system approach to management of expenses.

Many scientists were engaged in questions of the analysis and improvement of principles and methods of management, namely: Appenyansky A.I. [38 , page 43], Balabanov I.T. [39 , page 102], Gerchikova I.N. [40 , page 96], Zigert V., Lang L. [41 , page 168], Turilo A.M. [19 , page 21], Partin G. A. [42 , page 39], and other.

According to the motivational characteristic, as a part of methods of management allocate three groups: economic, organizational and administrative and socially - psychological [33]. Interrelation of methods of management it is shown on fig. 4.

Fig. 4 – Methods of management

There are following main methods of control over expenses: standard-kost, direkt-kosting, just-in-time system, functional and cost analysis, target-kosting, method of the analysis and optimization of expenses, ABC analysis, CVP analysis.

Methods of optimization of expenses of made production remains to one of the major factors for adoption of administrative decisions, both on strategic and on operational levels.

In the third section «The recommendation about system improvement by expenses» is offered to develop complex model on optimization of expenses, also to consider and specify a method of expediency of expenses and to analyse forecasting of expenses.

Conclusion

Profitability of the enterprise therefore effective management of expenses which provides minimization of their combined value is extremely important depends on size of expenses.

On level and dynamics of expenses depend not only financial results of the separate enterprises and their structural divisions, but also efficiency of formation of the national income at state level as a whole. Among existing instruments of optimization of expenses the main are instruments of regular management of expenses to which carry the account, control and measures for decrease in their level. The correct management of expenses, in turn, creates the enterprises solid margin of safety and increases its efficiency, so, strengthens its ability to protection of the market interests and ability other things being equal to get big profit.

References

- Великий Ю.М., Прохорова В.В., Н.В.Сабліна, Управління витратами підприємства// Харків: ВД "ІНЖЕК", 2009 р. – 192 с.

- Іванюта П.В., Лугівська О.П., Управління витратами: навч. посіб.//Київ: «Центр учбової літератури», 2011 р. – 316 с.

- Грещак М Г, Коцюба О С Управління витратами. навч-метод. посібник для самост. вивч. дисц. – К.: КНЕУ, 2009 – 350 с.

- Дашкевич О.Ю., Класифікація витрат виробництва//Збірник наукових праць Національного університету державної податкової служби України, 2011 р. № 1 – с. 110

- Головачев А. С., Экономика предприятия: учебное пособие// Москва: Вышэйшая школа, 2011 г. – 320 с.

- Положення (стандарт) бухгалтерського обліку 16 «Витрати», затверджене Наказом Міністерства фінансів України від 31.12.1999 р. № 318., зі змінами і доповненнями.

- Бойко Є.І., Удосконалення системи управління витратами на підприємствах//Науковий вісник НЛТУ України, 2008 - вип. 18.6 – с. 139

- Сайт статистики України//[Електронний ресурс]. Код доступу:http://www.ukrstat.gov.ua/

- Вікіпедія: вільна енциклопедія//[Електронний ресурс]. Код доступу:http://uk.wikipedia.org

- Економічний аналіз: навч. посібник / Болюх М.А., Бурчевський В.З., Горбаток М.І. та ін.; За ред. акад. НАНУ, проф. М. Г. Чумаченка. — Вид. 2-ге, перероб. і доп. — К.: КНЕУ, 2008. — 556 с.

- Баканов М.И., Мельник М.В., Шеремет А.Д., Теория экономического анализа// М.: Финансы и статистика, 2005. — 536 с.

- Фрідман А.М. Економіка торгівельної діяльності споживчого суспільства: Навчальний посібник - видавництво Воронезького університету, 2004. – 540 с.

- Бутинець Ф.Ф., Бухгалтерський фінансовий облік//8-ме вид., доп. і перероб. - Житомир: ПП "Рута", 2009. - 912 с.

- Колчина Н.В., Поляк Г.Б., Павлова Л.П. Финансы предприятий// Москва: Юнити-Дана, 2009 - 447 с.

- Друри К. Введение в управленческий и производственный учет//- М.: Аудит, ЮНИТИ, 2009. - 783 с.

- Голов С. Ф., Костюченко В. М. Бухгалтерський облік та фінансова звітність за міжнародними стандартами. - Київ: Лібра, 2010. - 880 с.

- Карпова Т.П., Управлінський облік//підручник для ВУЗів// М.: Юніті-Дана, 2007 р. – 354 с.

- Кошелева В.А. Управленческий учет издержек / В. А. Кошелева, Крапивницкая Светлана Николаевна ; В.А. Кошелева, С.Н. Крапивницкая// Економіка і маркетинг в ХХІ сторіччі : матеріали ІХ Міжнародної науково-практичної конференції студентів і молодих вчених, м. Донецьк, 23-25 трав. 2008 року / ДонНТУ, Донецька обл.держ.админістрація. - Донецьк, 2008. - С.156-158.

- Турило А. М., Кравчук Ю. Б., Турило А. А. Управління витратами підприємства: навч. посібник. — К.: Центр навчальної літератури, 2010. — 120 с.

- Партин Г.О., Управління витратами підприємства: концептуальні засади, методи та інструментарій: Монографія К.: УСБ НБУ, 2003. – 219 с.

- Данилюк М.О., Лещій В.Р. Управління витратами на промислових підприємствах / Науково-практичний посібник: Наукове видання. - Івано-Франківськ: ПП Супрун, 2006. - 172 с.

- Скригун Н.П., Цимбалюк Л.Г., Удосконалення методики калькулювання собівартості продукції// Вісник Бердянського університету менеджменту і бізнесу, 2009 р. - № 4(8) – с. 62

- Покропивний С.Ф. Економіка підприємства// - К.: КНЕУ, - 2008 р. – 340 с.

- Курило О.Б., Механізм управління витратами машинобудівних підприємств//Національний університет "Львівська політехніка", 2011 р. - № 45 – с. 271

- Ю.С. Цал-Цалко. Витрати підприємства/Цул, 2009 р. – 657 с.

- Кошелева В.А., Крапивницкая С.Н. Пути и инструменты управления прибылью предприятия// Всеукраинская научная конференция студентов «Проблемы управления производственно-экономической деятельностью субъектов хозяйствования», 2008 г. – 141 с.

- Котляров С.А. Управление затратами//М.: 2002 – 159 с.

- Трубочкина М.И., Управление затратами//Москва: ИНФА-М, 2009 г. – 320 с.

- Грещак М.Г., Коцюба О.С. Управління витратами. навч-метод. посібник для самост. вивч. дисц. – К.: КНЕУ, 2009 – 350 с.

- Бєльтюков Є.А., Безнощенко Н.О., Управління витратами на основі функціонально-вартісного аналізу// Вісник Хмельницького національного університету, 2011 − № 2, Т.2 – с. 7

- Васильєва Т.А., Рябенков О.В., Використання АВС-методу в системі управління витратами промислового підприємства// Всеукраїнський науково-виробничий журнал, 2011 − № 4 – с. 181

- Цмоць О.І., Аналіз і вибір методів стратегічного управління машинобудівним підприємством у режимі реального часу// НУ "Львівська політехніка"- Збірник науково-технічних праць, 2010 − Вип.20.3 – 280 с.

- Донець Л.І. - Еекономічні ризики та методи їх вимірювання// [Електроний ресурс]// Код доступу: http://www.net/book_55_glava_29_2.5.3._Метод_аналіз.html

- Осовська Г.В., Осовський О.А., Основи менеджменту// [Електронний ресурс]// Навчальний посібник / К.: "Кондор", 2006.- 664 c. Код доступу:http://ualib.com.ua/br_5525.html

- Драчева Е.Л., Юликов Л.И., Менеджмент//[Електронний ресурс]//Код доступу:http://www.bibliotekar.ru/biznes-29/29.htm

- Поняття, функції та методи управління//[Електронний ресурс]//Код доступу:http://www.refine.org.ua/pageid-1447-2.html

- Ватченко О.Б., Шевченко Я.Г., Методи калькулювання в стратегічному управлінні// Економічний простір, 2011 – № 48/2 – с. 175

- Аппенянский А. И. Человек и бизнес. Путь совершенства / Аппенянский А. И. – М.:Барс, 1995. – 228 с.

- Балабанов И. Т. Основы финансового менеджмента / Балабанов И. Т. – М.: Финансы и статистика, 2000. – 528 с.

- Герчикова И. Н. Менеджмент: [учебник] / Герчикова И. Н. – М. : ЮНИТИ, 1995. – 480 с.

- Зигерт В. Руководство без конфликтов / В. Зигерт, Л. Ланг. – М.: Экономика, 2000. – 335 с.

- Партин Г.О., Управління витратами підприємства: концептуальні засади, методи та інструментарій: Монографія К.: УСБ НБУ, 2003. – с. 219

- Панасюк В.М., Витрати виробництва: управлінський аспект. - Тернопіль: Астон, 2005. - 288 с.

- Партин Г.О., Формування стратегічної моделі управління витратами підприємства// Фінанси України, 2008 г. - № 11- с. 124

- Череп А.В. Управління витратами суб’єктів господарювання Ч.1: Монографія. – 2-е вид., стереотип// Х.: ВД "ІНЖЕК", 2007. – 368 с.

- Керимов В.Э., Учет затрат, калькулирование и бюджетирование в отдельных отраслях производственной сферы//Учебное пособие- М.: 5 изд., 2008 г. – 477 с.

- Радченко К., Таргет-костинг или искусство делать дешевле//Менеджмент и менеджер, 2003 г., - № 11 – с. 45

Note

In writing this essay Masters qualifying work is not finished yet. Final completion is scheduled for January 2013. The full text of the work and materials on the topic of work can be obtained from the author or his supervisor after the specified date.