Abstract

Content

- Introduction

- 1. Goal and tasks of the research

- 2. Conceptual framework and standardization environment for cost accounting.

- Conclusion

- References

Introduction

Theme urgency. . In modern conditions, the problem of effective expenditure management is becoming more acute for enterprises, as the prospects for the development of the enterprise begin to depend largely on the behavior of costs, the degree of their manageability. Ability in periods of worsening of the situation to systematically and rationally reduce costs increases the chances of survival.

At the same time, accounting for production costs and calculating the cost of production in the accounting system at industrial enterprises is the most difficult and important accounting process. It is important in the organization, management of production and planning of the enterprise, because it is based on economic indicators of production.

The category of expenditures is typical for all business entities, regardless of their type of activity, form of ownership, size. Expenses directly and indirectly affect virtually all areas of the enterprise's operation, determining its pricing policies, production volumes, profit margins, financial performance indicators, the competitiveness of products and enterprises as a whole, the efficiency of company management, etc. In general, expenses reflect the price of all economic resources attracted by the enterprise and, thus, simply characterize the effectiveness of its activities.

The production process for any industrial enterprise is the main stage, where the prime cost of production is directly formed. Therefore, all the shortcomings in the work, both production workshops and accounting units lead to an increase in production costs.

Particularly significant impact is the unproductive loss of raw materials and finished products at all stages of the production process, the absence of a comprehensive methodology for their evaluation and accounting.

Using the cost index, the enterprise has the ability to monitor the efficiency of using material, labor and financial resources, determine the economic efficiency of introducing new equipment, and establish an objective price for products. That is why the prime cost is one of the most important generalizing indicators of the enterprise's activity and the main instrument of regulation of its financial position.

1. Goal and tasks of the research

To identify shortcomings and contradictions in the accounting and audit of the costs of the enterprise and the development of specific recommendations for their improvement is the goal of research.

Main tasks of the research:

- Consider the legal framework for accounting and assessment of costs;

- Study the classification and evaluation of the recognition of cost accounting;

- Identify problematic aspects of accounting policy and the formation of a tax base for accounting for expenditures;

- Familiarize with the organization of accounting of expenses in the conditions of the enterprise;

- Consider the audit and the main directions of accounting and control costs;

- Identify shortcomings and contradictions in the accounting and audit of the costs of the enterprise;

- Develop recommendations for improving the accounting and auditing of the company's expenses.

Research object: financial and economic activity of enterprises.

Research subject: theoretical and practical aspects of accounting and auditing expenses

2. Conceptual framework and standardization environment for cost accounting.

In the course of its activities, the enterprise carries out material and monetary costs. Depending on the role they play in the process of reproduction, they are divided into three groups:

- Expenses related to the main activity of the enterprise. This is the cost of production and sale of products, the so-called current costs, which are reimbursed from the proceeds from the sale of products (services);

- Expenses related to investment activities, that is, expansion and renewal of production. One-time costs for simple and extended reproduction of fixed assets, increase in working capital and the formation of additional labor for a new production. Sources of financing these costs are depreciation, profit, issuance of securities, loans and the like;

- Expenses for the social development of the team (social, cultural, recreational, housing and other needs). These costs are not related to the production process, and therefore the source of their financing is profit [6].

The greatest share in the total volume of the company's expenses is the cost of production.

Distinguish between economic and accounting costs. Economic costs are all kinds of payments to suppliers for raw materials and material resources. These costs consist of external (explicit) and internal (implicit or implicit). External costs are payments to suppliers of material resources, payment of wages, accrual of depreciation, etc. This group of expenses will constitute accounting costs, which actually correspond to the expenses of our enterprises.

Internal costs should be implicit, implicit in nature, because they reflect the use of resources owned by the owner of the enterprise in the form of land, premises, assets, etc., for which he formally does not pay. The entrepreneur actually realizes these expenses, but not in explicit form, but in monetary terms. Hence, accounting costs are the difference between economic and implicit costs.

The concept of "economic costs" is generally accepted, accounting - are calculated in practice to determine the actual amount actually incurred costs, taxable profits and the like. Expenses are almost always made in kind and in cash. Planning and recording costs in kind is important for the organization of production. However, for the evaluation of production results, a monetary estimate of costs is necessary.

According to Ukrainian National Accounting Standards - 1 «General requirements for financial reporting», «expenses are the reduction of economic benefits in the form of asset retirement or increase in liabilities that lead to a decrease in equity capital (with the exception of a decrease in capital due to its withdrawal or distribution by owners) » [3].

Methodological principles for the formation in the accounting of information on the costs of an enterprise and its disclosure in the financial statements in the DNR are determined by the Ukrainian Accounting Standards 16 «Expenses». Also in UAS 9 « Inventories», UAS 26 «Payments to employees», UAS 17 « Tax on profits » and is regulated by the Tax Code of the DNR [2].

When inspecting the regulatory framework, it is impossible not to pay attention to international accounting standards, IAS-2 « Inventories», IAS-23 «Borrowing Costs» and others [5].

The fundamentals of the organization of accounting are regulated by the Law of the DNR «On Accounting and Financial Reporting» № 14-IHC of 27.02.2015 (as amended). This law applies to all legal entities, regardless of their organizational and legal forms and forms of ownership [1].

According to UAS 16 «Expenses», «expenses are reflected in accounting simultaneously with reduction of assets or increase in liabilities. Expenses are recognized as expenses of a certain period, together with recognition of the income for which they are incurred. If the asset provides economic benefits for several accounting periods, the costs are recognized by the systematic allocation of its value (for example, in the form of depreciation) between the relevant reporting periods» [4].

«Not recognized as expenses and are not included in the income statement:

- payments under agreements of the commission, agency agreements and other similar contracts in favor of the committent, the principal and the like;

- preliminary (advance) payment of stocks, works, services;

- repayment of received loans;

- other decreases in assets or increases in liabilities that do not comply with the criteria given in clause 6 of this Regulation (standard);

- expenses, which are reflected by a decrease in equity in accordance with the provisions (standards) of accounting;

- book value of currency» [4].

«All the company's expenses, according to UAS 16, are divided into production, operating and other operating expenses» [4].

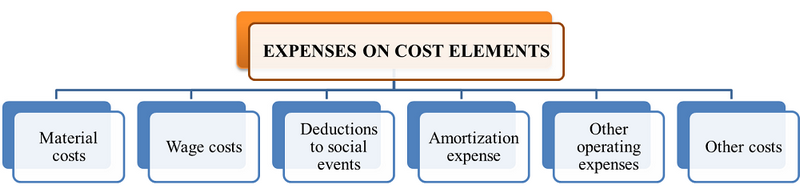

Expenses on cost elements are grouped as follows (Fig. 1):

Figure 1 – Expenses on cost elements

In terms of activities, expenditures are divided in this way (Fig. 2):

Figure 2 – Classification of expenses by type of activity

(animation: 8 frames, 15 cycles of repeating, 133 kilobytes)

Thus, costs are a reduction in economic benefits in the form of asset retirement or an increase in liabilities that lead to a decrease in equity (with the exception of a decrease in capital due to its seizure or distribution by owners) (according to UNAS -1 «General requirements for financial reporting»). Methodological principles for the formation in the accounting of information on the costs of an enterprise and its disclosure in the financial statements in the DNR are determined by the UAS 16 «Expenses»

Conclusion

Analyzing the above, we can formulate the following conclusions

Accounting for the company's expenses is constantly developing and improving in connection with the improvement of computer equipment and communication environment, methodology and organization of accounting as the main information source about the costs of the enterprise. The production process for any industrial enterprise is the main stage, where the prime cost of production is directly formed. Therefore, all the shortcomings in the work, both production workshops and accounting units lead to an increase in production costs. Particularly significant impact is the unproductive loss of raw materials and finished products at all stages of the production process, the absence of a comprehensive methodology for their evaluation and accounting.

Using the cost index, the enterprise has the ability to monitor the efficiency of using material, labor and financial resources, determine the economic efficiency of introducing new equipment, and establish an objective price for products. That is why the prime cost is one of the most important generalizing indicators of the enterprise's activity and the main instrument of regulation of its financial position.

In the conditions of the existing calculating mechanism, the total cost of production includes all the price increases caused by excessive losses of raw materials and finished products at all stages of the production process. To eliminate the causes of this situation, it is necessary to change the mechanism of primary and synthetic accounting of raw materials and materials and the general calculation methodology based on the compilation of material balances.

The main disadvantage of the current practice of accounting and calculation of costs is that the total costs include all the rise in price caused by excessive losses of raw materials at all stages of the production process. The lack of a methodology for determining such rise in prices makes it difficult to formulate estimates, which leads to the adoption of inadequate managerial decisions. An integrated approach in this matter should be based on determining the productive costs for the production of all products.

The main condition for the implementation of the proposed recommendations are: maintaining a clear daily accounting of all products, losses and wastes by their types, indicating the quality characteristics; the establishment of normative coefficients of losses, waste and products of their processing at all stages of the production process, which must be approved and mandatory for implementation in the industry.

So, the category of expenses is typical for all business entities, regardless of their type of activity, form of ownership, size. Expenses directly and indirectly affect virtually all areas of the company's operation, determining its pricing policy, production volumes, profit margins, financial performance indicators, the competitiveness of products and enterprises as a whole, the efficiency of company management, etc.

This master's work is not completed yet. Final completion: May 2018. The full text of the work and materials on the topic can be obtained from the author or his head after this date.

References

- Закон ДНР «О бухгалтерском учете и финансовой отчетности» № 14-IHC от 27.02.2015, действующая редакция по состоянию на 19.01.2016 [Электронный ресурс].- Режим доступа: http://dnrsovet.su/zakon....

- Налоговый кодекс ДНР: [Электронный ресурс]. - Режим доступа: http://dnrsovet.su/....

- Национальное Положение (стандарт) бухгалтерского учета 1 «Общие требования к финансовой отчетности»[Электронный ресурс].- Режим доступа: http://zakon2.rada.gov.ua....

- Положение (стандарт) бухгалтерского учета 16 «Расходы» [Электронный ресурс].- Режим доступа: http://zakon3.rada.gov.ua....

- Международные стандарты бухгалтерского учета 1 «Представление финансовой отчетности», 2 «Запасы», 16 «Основные средства», 19 «Вознаграждения работникам» [Электронный ресурс].- Режим доступа: https://buhgalter911.com....

- Юрченко К. Класифікація витрат виробництва в нових умовах господарювання //Вісн.Терноп.акад.нар.госп.- 2008.Вип. 7/2- с.101-104.