Abstract

Content

- Introduction

- 1. Theme urgency

- 2. Goal and tasks of the research

- 3. THEORETICAL BASIS OF LEASING ACTIVITIES IN THE MODERN ECONOMY

- 4. COMPLEX OF RECOMMENDATIONS ON ACTIVATION OF THE MECHANISM OF MANAGEMENT OF THE LEASING ACTIVITY OF THE ENTERPRISE

- Conclusion

- References

Introduction

The current state of the economy, its integration direction of development, the desire to activate investment processes necessitate the attraction of significant long-term investment resources. These resources, like any others, are limited and expensive, and in times of economic crisis, inaccessible. This encourages business entities to seek and use new alternative methods of financing the economy. One of the most promising and effective methods of investing in fixed assets of an enterprise is leasing.

1. Theme urgency

The use of leasing is especially important for industrial enterprises, the characteristic features of which are: rapid moral and physical deterioration of fixed assets (according to official statistics, it ranges from 70-80%), a short product life cycle, a high level of capital intensity of production, resource-intensive techniques and technologies, ineffective sources of financing for enterprises, insignificant investments in innovations, etc. This situation led to serious problems – a decrease in quality and an increase in the price of products, which led to the loss of competitive positions in the market. Therefore, leasing transactions can become a source of renewal of fixed assets, a promising direction for increasing the volume of production potential and an effective tool for selling our own products.

2. Goal and tasks of the research

The purpose of this work is to develop theoretical provisions and practical recommendations for activating the mechanism for managing the leasing activities of an enterprise.

An integrated approach to the implementation of this goal outlined the range of tasks that were supposed to be solved in this master's study:

• to reveal the essence, types and participants of leasing;

• to determine the features of the organization of leasing activities at the enterprise;

• investigate investment and leasing processes at the macro level;

• analyze the performance indicators of a modern enterprise;

• to develop practical recommendations aimed at activating the mechanism for managing the leasing activities of the enterprise.

The object of the research is the process of activating the mechanism for managing the leasing activities of an enterprise.

The subject of the research – is theoretical and practical provisions for enhancing the mechanism for managing the leasing activities of an enterprise.

The main results of the research performed are:

- the conceptual apparatus was further developed;

- identified the problems of leasing development at the macro level;

- developed practical recommendations aimed at enhancing the mechanism for managing the leasing activities of the enterprise.

- controlled system (object of management) – the sphere of reproduction of the active part of fixed assets through leasing;

- management system (subjects of management) – enterprises, creditors, suppliers, intermediaries, leasing companies, sellers, government agencies.

- Subjects of leasing – the lessor and the lessee.

- Factors of the external environment, such as leasing legislation, tax legislation, macroeconomic situation in the country[10].

- Subsystems for leasing back management (both from the lessor and from the lessee).

- A set of objectives of the enterprise, strategy for the development of the enterprise, policy in the field of technical re-equipment (for the tenant), the financial and economic situation of the enterprise.

- Амшокова, М. Х. Возможности использования лизинга при обновлении предприятиями основных фондов / М. Х. Амшокова // Современные научные исследования и инновации – 2015. – №12 – [Электронный ресурс]. – Режим доступа: http://web.snauka.ru/issues/2015/12/61586

- Багимова, А. Д., Иванченко, Д. А., Мешков, А. В. Инвестиционная привлекательность предприятия как важнейшая характеристика субъекта хозяйствования производства / А. Д. Багимова, Д. А. Иванченко, А. В. Мешков // Ресурсосбережение. Эффективность. Развитие: материалы научно-практической конференции, г. Донецк, 25 октября 2018 г. / ГОУ ВПО

ДонНТУ

. – Донецк: ДонНТУ, 2018. – с. 16-17. - Белкин, С. С. Анализ современного состояния лизингового рынка в Российской Федерации / С. С. Белкин // Научно-методический электронный журнал

Концепт

. – 2017. – Т. 4. – С. 25–36. - Горбатенко, О. А. Проблеми та перспективи розвитку лізингових відносин в Україні / О. А. Горбатенко // Фінанси України. – 2012. – №13. – С.123-126.

- Дараева, Ю. А. Теория бухгалтерского учета. / Ю. А. Дараева // – 2014. – С. 175

- Диамантис, Д. Г. Современное состояние финансовой аренды (лизинга) в России, США и странах Западной Европы / Д. Г. Диамантис // Политика, государство и право – 2014. – № 7 – [Электронный ресурс]. Режим доступа: http://politika.snauka.ru/2014/07/1790

- Доценко, Е. М., Карпухно, И. А Инвестиционный климат в Российской Федерации: Проблемы инвестиционной привлекательности / Е. М. Доценко, И. А. Карпухно // Ресурсосбережение. Эффективность. Развитие: материалы научно-практической конференции, г. Донецк, 25 октября 2018 г. / ГОУ ВПО

ДонНТУ

. – Донецк: ДонНТУ, 2018. – с. 51-53. - Ершова, Т. С., Заричанская, Е. В. Особенности осуществления лизинга в современных условиях / Т. С. Ершова, Е. В. Заричанская // Ресурсосбережение. Эффективность. Развитие: материалы научно-практической конференции, г. Донецк, 25 октября 2017 г./ ГОУ ВПО

ДонНТУ

. – Донецк: ДонНТУ, 2017. – с. 48-51. - Ершова, Т. С., Заричанская, Е. В. Лизинг как важная составляющая инвестиционного механизма обновления технической базы производства / Т. С. Ершова, Е. В. Заричанская // Ресурсосбережение. Эффективность. Развитие: материалы научно-практической конференции, г. Донецк, 25 октября 2018 г. / ГОУ ВПО

ДонНТУ

. – Донецк: ДонНТУ, 2018. – с. 152-155. - Куряева, Г. Ю. Лизинг. Понятие, объекты и субъекты лизинга. Операционный и финансовый лизинг. Проблема развития лизинга в России / Г. Ю. Куряева // Образование и наука в России и зарубежом – 2018. – №1 – [Электронный ресурс]. – Режим доступа: https://www.gyrnal.ru/statyi/ru/335/

- Методические рекомендации по расчету лизинговых платежей: eтв. Мин-вом экономики РФ от 16.04.2010. – [Электронный ресурс]. – Режим доступа: http://www.consultant.ru/document/cons_doc_LAW_10606/

3. THEORETICAL BASIS OF LEASING ACTIVITIES IN THE MODERN ECONOMY

Classic leasing provides for the participation in it primarily of the lessor, who is the owner of the leased item (most often purchased to order), which transfers it to the lessee for periodic lease payments. The lessee is a user or owner of the leased asset, who uses it for its intended purpose and pays recurring lease payments [9]. Another main subject of leasing relations is the seller of the leased asset, who sells the corresponding property to the lessor for its subsequent transfer to the lessee for use and is directly responsible to the lessee for this property (fig. 1).

Figure 1 – Scheme of a leasing transaction and financial flows

(animation: 7 frames, 5 cycles of repeating, 14 kilobytes)

The subject of leasing can be any movable and immovable property related to fixed assets according to the current classification, except for land plots and other natural objects, as well as objects prohibited for free circulation on the market [8].

The essence of the leasing operation is as follows: a potential lessee who does not have free financial resources applies to the leasing company with a business proposal to conclude a leasing transaction. According to this transaction, the lessee chooses the seller who has the required property, and the lessor acquires it and transfers it to the lessee for temporary possession and use for a fee specified in the lease agreement. At the end of the contract, depending on its terms, the property is returned to the lessor or becomes the property of the lessee [3].

4. COMPLEX OF RECOMMENDATIONS ON ACTIVATION OF THE MECHANISM OF MANAGEMENT OF THE LEASING ACTIVITY OF THE ENTERPRISE

When managing leasing operations at enterprises, it is advisable to use a systematic approach. Leasing activities have all the functions of the system:

The rate of increase in the production capacity of enterprises cannot provide the required volume of real estate commissioning. Lack of capacity and high wear and tear of equipment and machinery lead to a gap between potential demand and production volume. To eliminate the loss zone, it is necessary to increase the production capacity of enterprises by developing mechanisms for attracting investments, one of which is leasing. At the same time, the prospect of using leasing as an effective way to invest in fixed assets of enterprises depends not only on the socio-economic conditions prevailing in the country, on the investment policy pursued by the authorities and enterprises, but also on the professional organization of the management of leasing operations.

The unstable financial condition of enterprises, difficulties in obtaining long-term borrowed funds necessitate the search for alternative sources of investment resources in the field of equipment renovation. One of these sources is leasing [6].

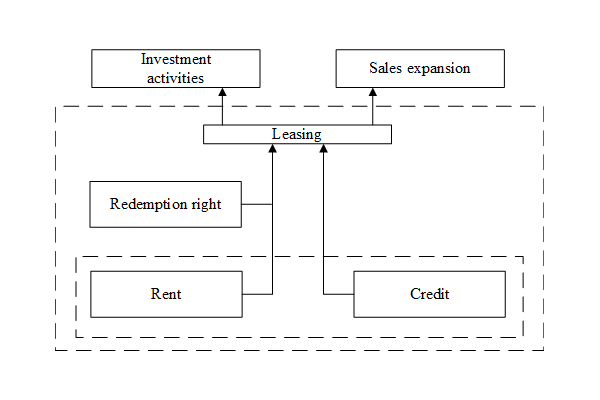

Leasing as an activity subordinated to the achievement of a certain goal requires the formation of an effective management mechanism, taking into account the specifics of the investment environment of enterprises in the implementation of leasing operations. To determine the investment environment, let us consider leasing as a multifactor integrated system of entrepreneurial activity, combining a set of leasing, credit, investment and trade organizational and economic relations (fig. 2)

Figure 2 – Leasing as a multifactorial system of entrepreneurial activity

Based on the system of relationships shown in figure 2, we denote the investment environment and leasing objects:

• the investment environment of enterprises in the implementation of leasing operations is understood as the sphere of reproduction of the active part of fixed assets [2];

• the main subjects of leasing within the designated investment environment are enterprises, government agencies, sellers, leasing companies, intermediaries, suppliers, and creditors;

• the main objects of leasing activities at enterprises should be: means of small-scale mechanization; lifting and transporting equipment; production equipment.

When providing technical re-equipment of enterprises, it is necessary to take into account the peculiarities of objects acquired through leasing: a variety of types and types; high price; high share in the cost of finished products; use for a long period. Taking into account the specifics of leasing objects, we will designate the features of the management of leasing operations at the enterprise [4]. The need to find the most acceptable conditions for the acquisition (from the point of view of reducing state investment construction, the company is forced to look for the best form of investment, and leasing is one of the alternatives, the effectiveness of its application should be justified in a business plan, where the calculation of efficiency and other investment options: loans, equity).

The need to choose the form of leasing depending on the type of the acquired object. The choice of an intensive development path, involving a qualitative improvement in the technical resources of the enterprise, an increase in productivity without changing the quantity, in contrast to the extensive development path (a quantitative increase in the technical resources of the enterprise). The construction company should strive to acquire high-performance equipment, the technical characteristics of which allow it to maintain its performance at a high level throughout its life. First, a significant increase in the number of production assets reduces the adaptive capabilities of the enterprise to a changing market; Secondly, the availability of the latest high-performance machinery and equipment makes it possible to reduce repair costs and increase the increase in the number of construction products.

The existing problems in the field of updating the technical resources of organizations are associated with their insufficient financial capabilities for intensive renewal and, therefore, with difficulties in obtaining long-term loans for these purposes, as well as with a reduction in the state budget, financing of the industry [7]. This problem has two sides:

• external: an enterprise is an open system, and it must carry out its activities in conditions of uncertainty of situations and the variability of the economic environment;

• internal: low efficiency of leasing operations management.

The main problem in the use of leasing is the low clarity of the organizational and economic foundations of leasing. The leasing management mechanism includes elements of the first and second levels of interaction.

First level elements:

Second level elements:

The functioning of the leasing management mechanism is based on the mutual influence and interaction of the elements of the first level – the lessor, the lessee and environmental factors. The lessor and the lessee enter into a lease agreement on the basis of current legislation, the macroeconomic situation in the country, and the need to enter into a lease agreement.

At the same time, this interaction presupposes the operation of the elements of the second-level leasing management mechanism – the leasing management subsystem. These subsystems are planning, organization, coordination and control based on the availability of both the lessor and the subsystem of values and parameters of the lessee, consisting of the following elements: corporate goals, strategy, policy modernization (for the lessee), economic and financial condition of the company. This subsystem determines the parameters of leasing planning, since on its basis it is possible to create control planning points, according to which it will be possible in the future to plan, organize, coordinate and control the leasing activities of the enterprise [5].

The chain of interaction of control subsystems within leasing entities is as follows: initially, on the basis of the subsystem of parameter values and parameters of the enterprise, the planning subsystem is activated. This subsystem is characterized by the fact that it is capable of influencing all the other subsystems of management – the subsystem of control, coordination and organization. The dominant position of the planning subsystem is due to the fact that it is possible to control, organize and coordinate leasing activities only after there is a detailed plan, which will reflect the main technical, economic and organizational parameters of leasing, the main results of these relations, control points by which one can judge the success of the leasing. transactions.

From the standpoint of the systems approach, the effective formation and functioning of the general control system depends on the effective formation and functioning of its subsystems [1]. The work identifies three main subsystems for managing leasing operations at the enterprises of the complex.

The purpose of the first subsystem: to determine the optimal amount of payments to the lessor in comparison with alternative sources of financing [11]. The purpose of subsystem №2: to determine the value of the total depreciation of technical resources and select those that need to be replaced. The result should be a reduction in the overall wear and tear of technical resources. The purpose of subsystem № 3: to ensure the investment attractiveness of the enterprise in order to attract leasing companies to cooperation on mutually beneficial terms.

The efficiency of management of leasing operations and the achievement of each of the subsystems of its goal is influenced by various factors of the external and internal environment, taking into account which it is possible to increase the efficiency of management. Depending on the conditions of the external and internal environment, the formation of a mechanism for managing leasing operations is carried out within one of the four main organizational and economic situations.

Conclusion

Based on the tasks of the leasing management system and the classification of external and internal environmental factors, it is necessary to develop at the enterprise three main subsystems for managing leasing operations in: a subsystem for managing financial relations between the lessor and the lessee, a subsystem for monitoring the state of technical resources of enterprises from the standpoint of the accumulated value of depreciation deductions, a subsystem for managing investment attractiveness of enterprises, allowing to improve management efficiency by regulating economic relations between the lessor and the lessee, identifying technical resources for replacement and ensuring the investment attractiveness of the company to attract leasing companies to cooperation on mutually beneficial terms. Consequently, enterprises need to introduce a leasing management mechanism in order to improve its efficiency.

This master's work is not completed yet. Final completion: June 2021. The full text of the work and materials on the topic can be obtained from the author or his head after this date.