Abstract on the topic of graduation work

Content

- Introduction

- 1. Relevance of the topic

- 2. The purpose and objectives of the study, the planned result

- 3. Current liabilities of the enterprise: structure, formation and use

- 3.1. Research and Development Review

- 3.2. The essence and content of current obligations as an object of accounting and government audit

- 3.3. Directions of governmental audit of the current obligations of the enterprise

- conclusions

- List of sources

Introduction

The water supply system of the Donetsk region is a unique complex of water supply and hydraulic structures, which includes the Severskiy Donets-Donbass (SDD) canal, the Second Donetsk and Yuzhnodonbass water pipelines, reservoirs and filtration stations, centralized water supply pumping stations and sewerage facilities.

At this stage of development of the republic, water supply and sewerage enterprises are in a rather difficult, one might even say, crisis situation. Lack of working capital for an enterprise often becomes the reason for the formation of losses from operating activities. In this situation, control over the correctness of the calculation of the current obligations of the enterprise is one of the important prerequisites for overcoming the crisis. The issue of short-term crediting of settlements for current liabilities is becoming important in solving the issue of improving the financial condition of a business entity.

1. Relevance of the topic

The internal economic nature of current liabilities determines those characteristics that affect the recognition of this category as such. The economic activity of enterprises is closely related to settlement transactions that form current liabilities. Liabilities are inherently funds attracted from external sources that make it possible to expand the economic activities of the enterprise, while ensuring the growth of its profitability, and, consequently, an increase in equity capital.

Effective management of accounts payable provides reserves for the temporary release of funds, however, the delay in repayment, lack of control over the state of accounts payable can lead to additional costs for the company. In addition, a violation of the maturity of obligations leads to their accumulation and, as a consequence, depreciation of funds for creditors. In general, this negatively affects the financial condition of enterprises in the republic.

Business entities are acutely faced with questions about the justification of the occurrence of accounts payable, the prevention of delay in repayment or bringing the debt to a state of hopelessness, its correct and reliable reflection in accounting and reporting, the implementation of a state audit of the emergence and repayment of current obligations, which is possible only if effective management and control systems.

The listed areas of optimization of the enterprise, along with the indicated shortcomings in the current legislation regarding the accounting of accounts payable, determine the relevance of the research topic.

2. Purpose and objectives of the study, planned results

The purpose of the master's thesis is to study the organization of accounting and state audit of the current obligations of the enterprise, as well as to identify internal reserves for their optimization.

To achieve this goal, the following tasks were set and completed:

1.determine the theoretical foundations of accounting and auditing of the company's current liabilities;

2. consider the organization of accounting for the current liabilities of the enterprise;

3. investigate the mechanisms of government audit of current capital liabilities.

Object of research: financial and economic activities of PUVKH KP

Company Water of Donbass

associated with the current obligations of the enterprise.

Subject of research: accounting and government audit of the company's current liabilities.

The theoretical and methodological basis of the work is the scientific works of domestic authors on the current obligations of the enterprise, the legislative and regulatory framework governing operations with current obligations, the data of enterprises and information obtained from open Internet sources regarding research problems.

The scientific novelty of the results obtained lies in the theoretical substantiation and development of organizational, methodological and practical recommendations for improving the accounting and state audit of the current obligations of the enterprise.

3. Current liabilities of the enterprise: structure, formation and use

3.1. Research and Development Review

Liabilities are the indebtedness of the entity arising from past events and the repayment of which in the future is expected to result in a decrease in the entity's resources embodying economic benefits.

Management decisions are made based on information about current obligations, which is formed in the accounting system. In this regard, there is a need to improve the theoretical and methodological aspects of recognition, classification, documentation, assessment and display of current liabilities in the accounting system, as well as methods of analysis, state audit of current liabilities and determining their impact on the company's solvency in modern economic conditions.

Domestic and foreign scientists have devoted their work to the study of these problems.

So S.I. Travinsky considers current liabilities as liabilities that are subject to repayment at the request of creditors, as well as a part of liabilities that will be repaid during the operating cycle or one year, starting from the balance sheet date [1].

V.V. Kachalin believes that current liabilities are liabilities, for the liquidation of which current assets are used that could be used in the ordinary activities of the enterprise [2].

In turn, T.A. Efimova, L. Chizhevska, S.L. Bereza, N.M. Tkachenko's obligations are divided into: monetary and non-monetary; current and future; long-term and current; actual, estimated and conditional [3].

Economists N.S. Abalmasov, V.S. Tereshchenko propose the following approach to determining current liabilities: these are short-term financial liabilities that must be settled during the current operating cycle of the enterprise or within a year from the date of the balance sheet compilation liabilities that are paid at the request of creditors or are expected to be liquidated within twelve months [4].

In turn, foreign investigators, such as: Kermit D. Larson, John J. Wilde, B. Chiapetta argue that current liabilities are liabilities that must be settled within one year, however, if the operating cycle exceeds one year, then they can be paid during this period [5].

M. Buffett, D. Clark believe that current liabilities are debts and other liabilities that the company must repay within one financial year, that is, these are funds that the company owes to suppliers for goods and services provided on credit [6].

A B. Needles, H. Anderson and D. Caldwell divide current liabilities according to the degree of probability into actual, estimated and contingent [7].

Thus, on the basis of the research carried out, it can be concluded that in the modern economic literature there is no single view of the category of

current liabilities

, their assessment methods and the internal eonomic essence. It should be noted that there is no single methodological approach regarding their accounting and government audit.

The uncertainty of the theoretical interpretations of the indicated indicator, the differences in the practical aspects of its use, complicate the speed and objectivity of assessing the results of the enterprise, the competitive position of the enterprise and the strategic directions of its development.

3.2. The essence and content of current obligations as an object of accounting and government audit

The study of the theoretical foundations of accounting and government audit of current liabilities in the system of sources of formation of the company's assets confirmed that the main component of the obligations of any enterprise is its accounts payable.

In turn, it has been proven that the economic category of

obligations is

much broader than the concept of

accounts payable

. Accounts payable is one of the types of obligations, since such obligations, to secure payments of vacations, retirement benefits and other types of security, guarantee obligations, deferred tax liabilities, contractual

obligations, do not fall under the definition of payables.

A liability is recognized if its measurement can be reliably measured and it is probable that future economic benefits will decrease as a result of its settlement. If at the balance sheet date the previously recognized liability is not subject to redemption, then its amount is included in the income of the reporting period.

From the point of view of accounting, the use of the concept of

obligation

is narrower than from the legal one. In practice, liabilities are recorded in the accounting only if there is a debt for them, that is, the obligations that are provided for by the contract and are subject to fulfillment

in the future are not debt and are not reflected in the accounting. Thus, current liabilities arise after the receipt of goods, works, services, advance and payroll, taxes, fees, etc., that is, as a result of past events.

At the same time, the past event should be interpreted as the first of two events of a business transaction carried out in order to increase economic resources (receipt of goods, works, services, advances, payroll, taxes, fees, etc.) in the expectation of receiving from their use greater benefit than the expected decrease in resources upon settlement of obligations. The definition of the content of the first and second events in relation to various business transactions is given in Table 1.

Table 1

Content of events on business transactions,

associated with the emergence and repayment of obligations

|

Business transaction |

The first event that gives rise to obligations |

The second event, which is carried out with the aim of extinguishing obligations |

|

Getting a loan |

Cash receipts |

Loan repayment through money transfer |

|

Purchase of inventory, acceptance of works, services |

Receipt of stocks, receipt of work, services from a supplier (contractor) |

Payment to the supplier (contractor) of the cost of the received stocks, works, services |

|

Sale of goods, works, services |

Receiving an advance payment or advance from buyers |

Shipment of goods, works, services to buyers |

|

Product manufacturing, service and enterprise management |

Payroll, pension and social insurance contributions, taxes deducted as expenses |

Payment of wages, payment of contributions to pension and social insurance, payment of relevant taxes to the budget |

|

Shipment of goods, products, performance of works, services or receipt of an advance from buyers |

Calculation of taxes payable to the budget upon receipt of income |

Payment of taxes to be charged to the budget upon receipt of income |

|

Receiving a profit |

Calculation of income tax |

Payment of income tax |

In each case, the settlement of a liability is associated with the disposal of assets, and therefore, with a decrease in future economic benefits as a result of the disposal of the enterprise's resources, and often the extinguishment of one liability gives rise to another liability.

The absence at the date of the financial statements of sufficient conditions for the recognition of those liabilities that were previously recorded on the balance sheet of the enterprise means the need to write them off with the simultaneous recognition of the income of the reporting period (that is, the liability is not subject to extinguishment).

The maturity date of the obligation is the period during which the obligation must be extinguished. For the purpose of recognition, classification and measurement in accounting, a distinction is made between:

–The period from the moment the obligation arises until the moment of repayment;

–the period from the date of the financial statements to the maturity date.

Current liabilities are reflected in the balance sheet at the repayment amount.

The structure of current liabilities is represented by the following categories:

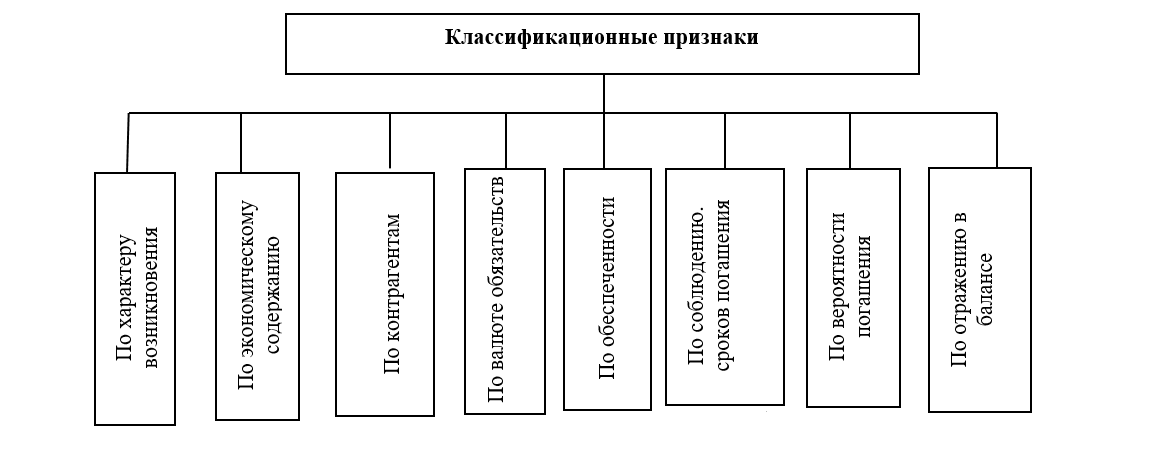

–Short-term bank loans;

–Current debt on long-term liabilities;

–short-term bills issued;

–accounts payable for goods, works, services;

–Current debt on settlements on advances received, on settlements with the budget, on settlements on off-budget payments, on settlements on insurance, on settlements for wages, on settlements with participants, on internal settlements;

–Other current liabilities.

When classifying the designated categories, it is advisable to adhere to the classification features shown in Fig. 1

|

Figure: 1. Classification signs of current liabilities

At the same time, the main tasks of accounting for current liabilities are:

1) ensuring correct and timely documentary reflection of transactions for the emergence and repayment of current obligations;

2) ensuring control over the current obligations of the enterprise;

3) ensuring control over the writing off of bad accounts payable;

4) determination of the actual size of the company's current liabilities as of the reporting date;

5) systematic management accounting;

In each field of activity, in each branch of the economy and for each enterprise, accounting and state audit of current obligations has specific features. Understanding the specifics of the category structure allows not only better managing it, but also focusing on exactly what should ensure their effective use.

3.3 Directions of governmental audit of the current obligations of the enterprise

The task of rational and effective use of funds by economic entities is currently one of the priorities for ensuring the development of the most important areas of the economy, ensuring food security and the development of high-tech industries

The audit of the effectiveness of the use of funds is implemented through the application of the following principles and approaches:

1. Correspondence of the laid down solutions (technical, organizational, financial, etc.) to the goals and economic interests. Determination of the economic efficiency of the use of funds is reduced to the clarification of such correspondence (or inconsistency).

2. Focus on the criterion for determining economic efficiency –net profit. This means that the main fragments used to determine efficiency, expressing the result of the commensuration of costs and benefits, on the basis of which all indicators of economic efficiency are constructed, should, by their economic nature, express net profit.

3. Conducting economic calculations for the entire period of production, the use of resources, including various phases, as well as the stages of the budget process.

4. Modeling real cash flows associated with the use of resources for the period.

5. Formation of all types of cash flows in full compliance with the requirements of the organizational and economic mechanism operating on the territory of the state. The organizational and economic mechanism is the rules governing the interaction of the owners of the organization with the state, with subcontractors. The organizational and economic mechanism includes:

–business rules;

–obligations;

–financing conditions;

–features of accounting policies;

–special conditions for the turnover of products and resources.

6. Taking into account the time factor. The most important aspect is taking into account the unequal value of different costs and benefits. Cash flow inequality is overcome by discounting or compounding.

7. Taking into account only forthcoming costs –the principle of determining efficiency, which must be reflected mainly when it is implemented in the existing production.

8. Taking into account all the most significant consequences. When determining effectiveness, both economic and other consequences should be considered.

9. Accounting for the impact of inflation on products and resources used.

10. Determine the preference of one of a number of performance indicators when used together to assess the use of funds.

Identifying deviations and searching for their solutions to eliminate them, as well as optimizing the work of a business entity in a designated area is the main goal of organizing a state audit of current obligations.

In the course of organizing a governmental audit of current liabilities, the analysis should be carried out in a comprehensive manner using a system of complementary indicators, which are expediently combined into three groups: quantitative indicators, qualitative indicators, indicators of covering current liabilities.

The proposed system of coefficients for analyzing current liabilities by groups is shown in Fig. 2.

|

Figure: 2. The system of coefficients for the analysis of current liabilities

The state audit of the structure of current liabilities, their turnover, determining the degree of solvency and liquidity of the enterprise, is carried out on the basis of financial reporting data, as well as by calculating the maximum amount of current liabilities under the influence of such factors as income, operating expenses, current assets of the enterprise.

The algorithm for conducting a governmental audit of the current obligations of an enterprise (Fig. 3) in order to establish the shortcomings of its functioning consists in sequentially passing certain stages from directly determining the object of the audit, goals, setting audit objectives and collecting information for its conduct, to analyzing the structure, turnover and coverage current liabilities, determination of the maximum amount of current liabilities permissible for a particular enterprise

|

Stage name |

Goals / objectives |

Audit mechanism |

|

First step |

Defining the object of the audit |

Current responsibility |

|

Defining the purpose of the audit |

Establishing the company's solvency, the efficiency of using its resources |

|

|

Formulation of the problem |

Analyze: –The structure of current liabilities; –The turnover of current liabilities; –solvency and liquidity; Determine the boundary rate of current liabilities Summarize the results of the analysis in order to make managerial decisions regarding the effectiveness of managing current obligations. |

|

|

Second phase |

Collection and preparation of information required for audit |

Financial statements. Statistical reporting. Notes to the financial statements |

|

Stage three |

Analysis of the structure of current liabilities |

Calculation of quantitative indicators |

|

Stage four |

Analysis of the turnover of current liabilities |

Calculation of quality indicators |

|

Fifth stage |

Analysis of solvency and liquidity |

Calculation of indicators of coverage of current liabilities |

|

Sixth stage |

Determination of the limit amount of current liabilities |

Calculation of the average monthly balance of current liabilities for an enterprise under the influence of factors such as operating income, operating expenses, cash current assets |

|

Seventh stage |

Summarizing audit results |

Making management decisions regarding the optimization of settlements for current liabilities |

To do this, using correlation and regression analysis, economic and mathematical models are used to predict the ability of an enterprise to repay its current obligations. At the same time, if the actual amount of current liabilities for the analyzed period exceeds the maximum amount obtained as a result of the calculation, the company is considered insolvent and requires adjustments to its functioning.

The given structure of research directions for current liabilities will make it possible to develop organizational and practical recommendations aimed at further developing the organization and methodology for accounting and government audit of current liabilities.

conclusions

The success of the operation of the enterprise directly depends on the efficiency of using the available resources in the process of economic activity. At the same time, the completeness of information is provided by the system for maintaining primary documents and accounting registers. Only the efficient functioning of this system, as well as the timely adoption, on the basis of the information coming from this system, management decisions will make it possible to optimize the current obligations of the enterprise, and therefore increase its competitiveness and survival.

The practical significance of the research results is determined by the fact that the application of the recommendations and methods for organizing accounting and state audit of current obligations developed in the master's thesis will contribute to an increase and increase in the efficiency of using the enterprise's resources.

List of sources

1. Травинский С.И. Классификация текущих обязательств в законодательстве и бухгалтерском учете [ Электронный ресурс]. –Режим доступа: http://bukuniver.edu.ua/Applications/zbirnik/n6/31_Klas.pdf

2. Качалин В.В. Финансовый учет и отчетность в согласовании со стандартами GAAP / В.В. Качалин. –четвёртый изд. –М .: Дело, 1998. –432 с.

3. Ефимова Т.А. Бухгалтерский учет : учеб . пос. / Т.А. Ефимова , Л. Чижевска , С.Л. береза; под ред. проф. Ф.Ф. Бутинця . –Житомир: ЖИТИ, 2000. –672 с.

4. Абалмасов Н.С. Совершенствование бухгалтерского учета текущих обязательств в Украине на основании международного опыта // Н.С. Абала –массовая , В.С. Терещенко [ Электронный ресурс]. –Режим доступа: http: //www.rusnauka. com / 11_EISN_2010 / Economics /64247.doc.htm

5. Ларсон Кермит Д. Основные принципы бухгалтерского учета . В 2 т. / Ларсон Кермит Д., Уайльд Джон Дж., Чиапетта Бар; пер. с англ., по наук. ред. Г. В. Григораш , Т. В. Герасимовой . –Днепропетровск : Баланс Бизнес Букс, 2007. –1336 с.

6. Баффет М. Как найти идеальную для инвестора компанию / М. Баффет , Д. Кларк. –Попурри , 2009. –79 с.

7. Нидлз Б. Принципы бухгалтерского учета / Б. Нидлз , Х. Андерсон, Д. Кол- дуэлл . –М .: Финансы и статистика, 2004. –496 с.

8. Сафарова А.Т. Проблемы оценки текущих обязательств в бухгалтерском учете [ Электронный ресурс]. –Режим доступа: http://vlp.com.ua/files/ 90_1.pdf

9. Гавриленко,В.А. Экономический анализ деятельности промышленных предприятий: монография / В.А. Гавриленко.-Донецк:ДонНТУ,2009.-383с. [Электронный ресурс] Режим доступа: http://ea.donntu.ru/handle/123456789/25203

10. Тесленко Т.И. Учет текущих обязательств на предприятиях различных форм собственности / Т.И.Тесленко // Вестник Национального университета государственной налоговой службы Украины.- 2008. –№ 1 (40). –С. 119-123.

11. Зеленко С.В. учетно аналитическое обеспечение управления кредиторской задолженностью за товары, работы, услуги / С.В Зеленко //Экономические науки. –2014. –№ 11 (41). –С. 65-71.

12. Сопко В. В., Муковиз В.С., Шарапа А.Н. Особенности определения и регулирования учета кредиторской задолженности. Глобализационные вызовы развития национальных экономик. материалы международной научно-практических конференции. –М.: КНТЭУ. –2016. –С. 635-647.

13. Травинская С.И. Классификация текущих обязательств в законодательстве и бухгалтерском учете [Электронный ресурс]. –Режим доступа: http://bukuniver.edu.ua/Applications/zbirnik/n6/31_Klas.pdf

14. Алимова С., Кулиш Н. В. Расчеты и обязательства как категории бухгалтерского учета //NovaInfo. Ru. – 2017. – Т. 2. – №. 58. – С. 283-287.

15. Богдашкина Ю. С. Учет расчетов с контрагентами //Экономика и социум. – 2016. – №. 3. – С. 178-180.

16. Девяева К. В. Современные проблемы бухгалтерского учета обязательств //Учет, анализ и аудит: проблемы теории и практики. – 2016. – №. 16. – С. 36-38.

17. Дружиловская Т.Ю. Учет обязательств организаций: проблемы и пути решения // Бухгалтерский учет в издательстве и полиграфии. –2016. –№ 4. –С. 35 – 41.

18. Елисеева О. В., Рябов А. Н. Учет операций по списанию задолженности по результатам инвентаризации расчетов с контрагентами //Научные исследования в социально-экономическом развитии общества. – 2017. – С. 214-216.

19. Майер В. А. Организация аудиторской проверки расчетов с поставщиками и подрядчиками //Научный журнал Дискурс. – 2017. – №. 4. – С. 145-149.

20. Скворцова Н. Ю., Мерзлякова Е. Д., Заглядова М. А. Аудит организации учета расчетов с поставщиками и покупателями //Молодежная наука 2016: технологии, инновации. – 2016. – С. 290-293.

21. Тюхова Е. А., Ханенко М. Е., Шапорова О. А. Аудит организации внутреннего контроля по учету расчетов с контрагентами //Современные концепции учета, анализа и аудита в развитии предпринимательства. – 2016. – С. 164-168.