|

Anastasiia KholinaFaculty of computer science and technology (CST)Department of Applied Mathematics and Imformation Science (AMIS)Speciality

|

Abstract |

Table of contents

IntroductionNowadays an effective program of fund's distribution is the primary goal of any trading system, which is somehow related to the reinvestment of profits [1]. There are two directions for traders of optimizing their trading strategy. The first and most important task is to achieve a positive expected risk-adjusted returns, the second – the definition of what percentage of capital he can risk in each transaction [2]. A subsystem of dynamic money management (DMM) is widely used in solving this problem, it’s based on the mathematical models and allows to multiply the initial capital with a maximum speed of the risk. Money management is the process of analyzing trades for risk and potential profits, determining how much risk, if any, is acceptable and managing a trade position (if taken) to control risk and maximize profitability [3]. 1. Theme urgencySome traders think by mistake that money management is only intended for those who trade on a regular basis or only in the short term. However, there is no type of trade, where it would be impossible to apply the methods of money management [4]. Although the problem of effective money management occurred in Ukraine in the 90s of the 20th century, when a national stock market began to form, currently insufficient attention is paid to the practical application of the algorithms of DMM. Some traders prefer to apportion the fixed part of a trading account for trade, they don’t taking into account the question of the optimal amount, which can be used at a given level of risk. Thus, the dynamic money management can be used in evety economic system, which invests its capital into the environment. It is represented by a number of algorithms, differing from each other on the complexity of its implementation, efficiency, applicability to control a particular economic system. Therefore, before making a decision it is necessary to analyze the effectiveness of each method on a number of indicators to select the most appropriate [1]. 2. Goal and tasks of the researchThe goal of this study is a comparative analysis of dynamic money management algorithms on the basis of the test profitability sequence of economic system based on several criteria. Main tasks of the research:

Research object: DMM algorithms efficiency indicators for managing capital economic system. Research subject: comparative analysis of DMM algorithms on a number of criteria. 3. Review of Research and DevelopmentThe idea of money management occurred in 18th century in Daniel Bernoulli’s research (1738), where he noted that, as a consequence of this, when profits are reinvested, in order to measure the value of risky propositions one should calculate the geometric mean [2].

The mathematician John von Neumann and economist Oskar Morgenstern worked in this field and wrote HarryMorgenstern Markowitz made a great contribution to portfolio theory, first proposed a mathematical model of optimal portfolio, which allows to determine the maximum profitability of the portfolio at a given level of risk portfolio and vice versa. Developed a criterion (Markowitz Criterion), reflecting the ratio of profitability-risk in the formation of an investment portfolio, taking into account the reinvestment of income.

Further development of the idea of money management continued the scientist Larry John Kelly Jr., who brought together game theory and information theory when he published Edward O. Thorp. worked a lot in this direction, developing Kelly’s researches.

Particular interest present the works of Ralph Vince: Bellman, Kalaba, Briman, Walden, Hakansson, Samuelson, Finkelstein, Whitley, Karatzas, Shreve, Zimba, Anderson, Jones, Stendhal, Zamansky, etc. worked in this area [2]. Not so many works of CIS countries' authors, who study the problem of managing capital, are known. Representative of this trend is Zhdanov I. (2009), who suggested that capital management techniques, based on approaches that use the principles of trading strategies and the various indicators (such as money management with the help of moving average money management using MACD, money management through channels and etc.). These techniques are very effective in combination with a successful trading system, trader, helping to increase the overall return on capital [2]. M. Babich, A. Gournac,V. Kovalev,A. Tereshchenko can be also attributed to the russian and ukrainian authors working in this field [5]. In the Donetsk National Technical University professor Alexander Smirnov with his of the develop of money management issues, as well as conducting research on the subject. 4. Research for the theme of master's workIn the master's work a comparative analysis of new dynamic capital management algorithms is taken on the basis of two test profitability sequences, which are represented in the form of yield curves. The yield curve – a graphic representation of changes in the values of P & L (Profit and Loss) at a certain time period. Some traditional models are used in the study :

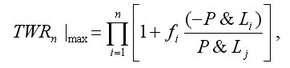

Ralph Vince model consists of finding the optimal part of investor’s capital, which corresponds to the maximum value of the multiplier of the initial capital (TWR – the ratio between final and initial state of the account of the investor):  where f – part of the capital for reinvestment, i.e. the unknown quantity; (-P&Li) – losses or profits, taken with the opposite sign; P&Lj – the most significant loss [6]. The value of the optimal f ranges from 0 to 1 and presents a fear of the investor before the probability of loss. Accordingly, when f =1 the investment risk is minimal, and f =0 is not profitable to the investor to risk hisk capital. Despite the fame, the model proposed by R. Vince has its negative sides and its application in practice is difficult [6]. Traditional algorithms for investors with a fixed value f const determine constant unchanging part of the capital for reinvestment, which characterizes only the fear of the investor before the investment risk, but does not assess them [7]. There were also implemented the original DMM algorithm:

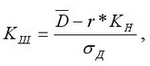

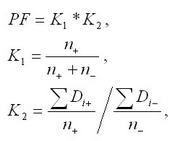

The most important step in capital managing is to evaluate its effectiveness, which is made on a number of indicators used in calculating the value of return and risk. Profitability is one of the most important criteria of money management efficiency. However, in addition to profitability is the reverse side – the risk, do not record it in the evaluation of the effectiveness can distort reality [8]. Analysis of the effectiveness of money management algorithms is held by the following [7]:

Sharpe Ratio is used to determine how well the return of the system compensates the risk accepted by investors. And, therefore, the greater the value of this index, the less risky the algorithm. Another key indicator of the system’s effectiveness is a profit factor (factor of profitability of the trading system) and, consequently, the greater the value of this indicator, the better the system works. ConclusionQualitative multi-criteria analysis money management algorithms is a key way to increase the effectiveness of any economic system, and presents not only theoretical research but also practical interest. After all, there are many different methods and strategies in this area, but the particular interest presents dynamic money management algorithms (DMM). This is due to the numerous advantages of this subsystem:

One of the experts in the field of risk and capital management is an American scientist R. Vince, who proposed his money management model, based on the calculation of This master's work is not completed yet. Final completion: December 2012. The full text of the work and materials on the topic can be obtained from the author or his head after this date. References

|

) at the end of the observation period;

) at the end of the observation period;

) in the range of the study:

) in the range of the study:

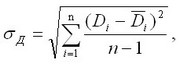

– average value of income (calculated from the autoregressive equation, which is obtained by least-squares method from the values Di),

– average value of income (calculated from the autoregressive equation, which is obtained by least-squares method from the values Di),