Abstract

Содержание

- Introduction

- 1. Theme urgency

- 2. Goal and tasks of the research

- 3. System of risk–control

- Conclusion

- References

Introduction

Presently there are such progress of markets trends, as globalization, internationalization, height of competition, passing to differentiation of the produced products, sent to individual satisfaction of necessities of customers, increase of requirements to quality and cost of commodity (services). These factors change the structure of economy, and, change the structure of risks of enterprise.

1. Theme urgency

In spite of presence of row of important works on application of quantitative methods of estimation of efficiency and degree of risks of administrative decisions of enterprise, the problems of research and development of methods and case frames remain рисками of virtual enterprise not decided fully. Description and algorithmization of processes of the strategic planning on the basis of complex application of analytical and imitation models taking into account the features of activity and development of enterprise are presently absent.

The actuality hired, related to the decision of problem of search, development and introduction of such forms and management methods by рисками that would allow to bring down their influence to the minimum possible level, is visible in this connection.

2. Goal and tasks of the research

An aim hired is to get useful information from a set of parameters (risk factors) and work out the system for the design of structure of risks.

For development of the system of design of risks it is necessary to decide next tasks:

- To study the theory–methodology base of management risk of enterprise.

- To work out the structure of the system of risk–control.

- To work out the methods of design of structure of risks.

- To realize the methods of design of structure of risks.

Research object: development of methods of design of structure of risks process on the basis of industrial enterprise.

Research subject: development of model of structure risks of enterprise.

3. System of risk–control

In the conditions of dynamically changing external and internal environment there is a necessity of operative adjustment of the productive program of enterprise. A similar situation results in the necessity of introduction of complex control system taking into account external and internal factors.

- swift rates of introduction of NT, increasing rates of modernisation;

- weak development of transport–logistic infrastructure;

- a vagueness of actual situation is in a business–environment;

- a vagueness of actual situation is in a business–environment;

- problems are in the prospects of development;

- chaoticness of the currency adjusting;

- strong influence of the political state of affairs;

- increasing inflexibility of ecological requirements (legislation, cleaning systems);

- a deficit of skilled shots is in a region;

- problems of in–plant training of personnel are in a region;

- integration processes are in the scales of industry, region, country.

To the internal factors it is possible to take:

- technology, modernisation, organizational factors of enterprise;

- violation of financial stability and liquidity;

- insufficient co–ordination of assortment politics;

- instability of skilled composition;

- high expenses on a rearmament and modernisation of production;

- instability and violations of succession of management conception;

- high degree of wear of equipment;

- subzero mobility of the system of the technical and technological providing of production.

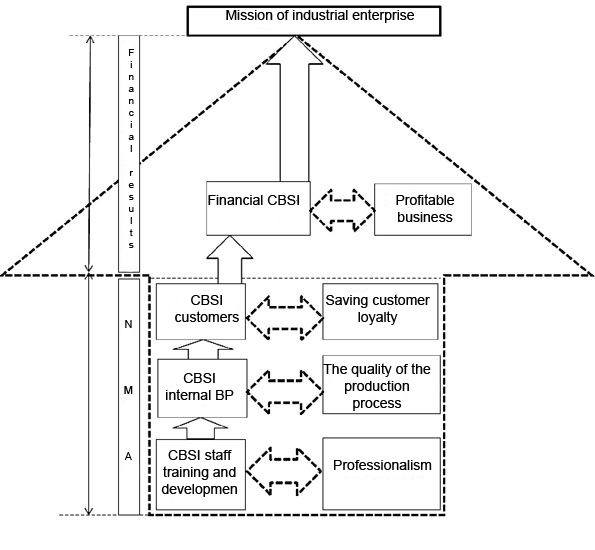

Co–ordination of internal administrative processes, external and internal environment of enterprise the system of risk–control (SRC) carries out. She will realize the complex algorithm of management an actual situation and perspective development of enterprise. Within the framework of this technology on the basis of monitoring of the balanced system of key indexes (CBSI) [5, 11] the analytical providing of diagnostics of rejections is realized, determinations of critical values and development of events on indemnification of negative influences of business processes (BP) for providing of competition development of enterprise.

In actual terms the market of products of enterprise becomes more difficult, the rates of development of him are accelerated, a predictability falls, values of descriptions of demand of флюктуируют by unforeseeable character.

CBSI on the base of four basic constituents of business (financial, client, internal, educating) allows to realize monitoring of co–ordination of short–term and of long duration aims, financial and unfinancial results, concordances external and internal and factors, basic and auxiliary parameters of enterprise (fig. 1).

Figure 1 – Example of an industrial enterprise CBSI

The search of new approaches of analysis of the systems, synthesis and realization of administrative decisions at the management of enterprise is required. Thus forming and introduction of the complex system of risk–control [2, 4-5] enterprise become necessary taking into account external (deficit of shots, deviation demand, expenses of the infrastructural providing and other) and factors into a production (technologies, modernisation, organizational factors). In the process of forming of aims of enterprise within the framework of approach of the systems the use of SMART of criteria is expedient.

In the process of functioning at the market of enterprise passes changing of phases of development of life cycle [1, 7]. The indexes of CBSI of stability of functioning change depending on the degree of reliability of organization of internal business processes and are the low bound of competitiveness of enterprise.

The structure of risk brief–case and level of each of types of risk substantially depend on the stage of life cycle of enterprise.

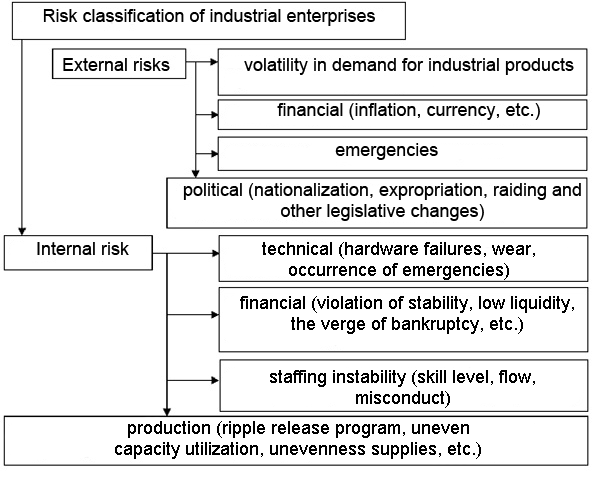

The basic signs of classification of external and internal risks of enterprise are shown on a fig. 2, 3 [8].

Figure 2 – Risk classification of industrial enterprises

(animation: 3 frames, 5 cycles of repeating, 13,1 kilobytes)

Coordination of internal management processes, internal and external environment of the enterprise carries out controlling, controlling purpose of the organization is derived from the objectives of the enterprise.

Figure 3 – Classification of internal and external risks of an industrial enterprise

Conclusion

Risk can and should be controlled, that is, to use certain measures to maximize predict the risk events and apply appropriate measures to reduce risk. Enterprise Risk Management is interconnected with the concept of " risk management."

In the master's work suggests one possible approach to risk assessment and management of the enterprise, based on the application of strategic management tools and statistical modeling, which allows to take into account the stochastic nature of environmental parameters and the study of the production system.

This master's work is not completed yet. Final completion: January 2015. Full text of the work and materials on the topic can be obtained from the author or his manager after that date.

References

- Абрамов А. В. Инновационная экономика: учеб. пособие. СПб.: СПбГМТУ, 2013. 96 с.

- Балабанов И. Т. Риск–менеджмент. М.: Финансы и статистика, 2000. 192 с.

- Бережнов Г. В. Стратегия устойчивого развития предприятия // Российское предпринимательство. 2002. № 10 (34). C. 24–30.

- Гусева И. Б. Методологические основы формирования системы контроллинга на промышленных предприятиях : дис. д–ра экон. наук: 08.00.05. Н. Новгород, ГОУВПО «НГТУ», 2008. 551 с.

- Каплан Р., Нортон Д. Сбалансированная система показателей. От стратегии к действию. М.: Олимп Бизнес, 2006. 304 с.

- Клейнер Г. Б., Тамбовцев В.Л., Качалов P.M. Предприятие в нестабильной экономической среде: риски, стратегии, безопасность / под общ. ред. С. А. Панова. М.: Экономика, 1997. 288 с.

- Кутанин Ю. В. Механизм организации контроллинга на промышленном предприятии : дис. канд. экон. наук: 08.00.05. М.: ННОУ ВПО «МГумУ», 2010. 162 с.

- Маринцев Д. А., Суржиков А.В. Понятие и классификация рисков в деятельности промышленных предприятий // Российское предпринимательство. 2013. № 9 (231). C. 75–79.

- Токаренко Г. С. Основы риск–менеджмента в предпринимательской деятельности // Финансовый менеджмент. 2006. № 1.

- Токаренко Г. С. Система риск–менеджмента компании // Финансовый менеджмент. 2006. № 2. С. 132–146.

- Шестерикова Н. В. Формирование стратегии устойчивого развития предприятия на основе сбалансированных показателей : дис. канд. экон. наук: 08.00.05. Н. Новгород: ФГБОУ ВПО «НГУ», 2009. 238 с.