- Introduction

- Most of the work

- 1. Scientific‑theoretical bases of formation of depreciation policy

- 2. Methodical bases of formation of depreciation policy at the enterprise

- 3. Methodical recommendations on the formation of depreciation policy at the enterprise in modern conditions

- Conclusions

- List of references

Introduction

The relevance of the topic

Depreciation policy is an integral part of economic policy. It acts as a major lever of state influence on economic processes in the country. First of all depreciation policy affects the process of renewal of basic production assets, the acceleration of scientific and technical progress, investment activities, and through them on the efficiency of social production.

Goal and tasks of research

Objective: The Aim of the master’s work is the further development of methodical bases and development of methodological recommendations on the formation of the depreciation policy of the enterprise in modern conditions.

The main research tasks:

- reveal the content of the depreciation policy of the enterprise.

- to consider methods of depreciation.

- to identify the availability of the company's main funds, through an analysis of the presence, composition and structure of assets of the enterprise.

- to carry out the analysis of efficiency of use of fixed assets by calculating the respective indicators.

- be familiar with the method of depreciation used by the company, identify the advantages and disadvantages.

- to calculate an alternative method of depreciation of fixed assets to more efficient uses.

Research object: is the process of forming the depreciation policy of the enterprise.

Research subject: Theoretical basis and methodological bases of formation of depreciation policy.

Analysis of studies. The issues of charging, accounting and use of depreciation within the depreciation policy of the enterprise engaged in such scientists as Kosovo E. C., Kuzmenko S. N., T. A. Vasilieva., S. P. Yaroshenko., Fuchs A. U., A. G. Zagorodny., Sagan T. L., Stadnicki Y. U., Tkachenko L., Gorodenka L. V., P. Orlov., S. Orlov., Rosillo V. I. and others.

Research methods. Studies in the master's works are carried out on the basis of General and special methods of scientific cognition. Common methods of scientific cognition is usually divided into three large groups:

- methods of empirical research (observation, comparison, measurement, experiment).

- methods that are used as the empirical and theoretical level studies (abstraction, analysis and synthesis, induction and deduction, modeling, and others).

- methods of theoretical investigation (ascent from the abstract to the concrete and others).

The scientific novelty of research consists in development of theoretical bases and the development of methodological recommendations on the formation of the depreciation policy of the enterprise.

Testing results of the work: The Main scientific and applied aspects of the work were presented at all–Ukrainian scientific–practical conferences: conference of students and young scientists Modern problems of management of investment and innovative activity

in 2014,Depreciation policy as the contemporary mechanism of management of investment activities

.

Most of the work

The introduction discusses the relevance of the theme of master's work given the purpose of the research, the object, subject and methods of research, revealed the practical value of the results.

1.Scientific‑theoretical bases of formation of depreciation policy

In the first section Scientific-theoretical bases of formation of depreciation policy

deals with the essence of the depreciation of its classification, the necessity for formation of the effectiveness of the amortization policy in modern conditions.

Classical economic theory states that depreciation is gradual transfer of cost of fixed assets on a product that is made with their help, targeted funds accumulation and their consistent use in the reconstruction of worn‑out assets.

The main components of depreciation policy should become an annual system of revaluation of fixed assets and depreciation, stimulating accelerated renewal of fixed assets; system of control and accountability over the use of depreciation funds.

The depreciation policy of enterprises in modern conditions must be based on conceptual approaches (figure 1).

Figure 1 – Conceptual approaches in depreciation policy

(animation: 16 frames, number of retries indefinitely, 55,8 kilabi)

In the article the Theoretical aspects of the analysis of depreciation as a basis of formation of the amortization policy

[4], is In. Th. Bakai gives definitions of depreciation: depreciation is a complex economic mechanism, quantitatively reflects the loss of tools cost of fixed assets, which are depreciated over their estimated useful lives (operation), and the gradual transfer and on the newly developed products with further accumulation of funds for playback (acquisition) of fixed assets

.

A significant contribution to the development of theoretical and methodological approaches to the solution of problematic issues amortization and depreciation policy made modern Ukrainian scientists S. Borisenko, O. Borodkin, F. Efimov, M. Vasilyuk, N. Vygovskaya, C. Goals,G. Kireitsev, J. Krupka, E. Mnich, V. Orlov, Yu. Osadchy, M. Pushkar, P. Sabluk, A. Fuks, P. the khomyn, G. Chumachenko, V. Shvets, etc [1].

The depreciation policy of the company largely reflects the depreciation policy of the state at different stages of economic development. Based on the established state principles, methods and norms of depreciation deductions. However, every company has an opportunity to individualize their depreciation policy, taking into account the specific conditions that define its parameters.

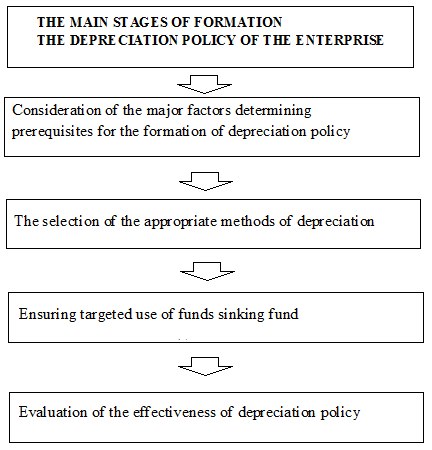

First of all, depreciation policy is a part of the state economic policy component of investment, innovation and tax policy, which through the establishment of scientific methods, standards and other tools to provide the reproduction of fixed capital of the enterprises and branches of the national economy in time and space with the purpose of maintenance and increase of its competitiveness. There are several basic stages of the depreciation policy of the enterprise (figure 2).

Figure 2 – Main stages of the formation of the depreciation policy of the enterprise.

2.Methodological basics of using the depreciation policy at the enterprise

In the second chapter the Methodological basics of using the depreciation policy at the enterprise

review methods of depreciation policy, which are used in various enterprises.

Every company has an opportunity to individualize their depreciation policy, taking into account the specific conditions that define its parameters.

At the micro level in implementing effective depreciation policy is a renewal process of the active part of basic production assets and increase the technical level of production. All this, in turn, creates sufficient basis to reduce production costs and maximize profits, which are the primary focus of accrual of depreciation [2].

Depreciation calculated using the following methods:

- Straight–line method:

• advantages – this method is easy calculation. the cost of the fixed asset object is deducted in equal parts during the whole period of its operation.

• disadvantages – not considered moral deterioration of operating system objects and the factor of increase of the cost of repairs as its operation (especially in recent years, the use of the fixed asset object).

- Method of reducing residual value:

• benefits – during the first years of operation of the fixed asset object accumulated a significant amount of funds required for its restoration.

• disadvantages – it is necessary to have a liquidation value needed to calculate the depreciation rate. If the liquidation value zero, then the component (LS : SS)1/T will also be zero. Thus annual depreciation will be equal to the original value.

- The method of rapid decrease of residual value:

• benefits – during the first years of operation of the fixed asset object accumulated a significant amount of funds required for its restoration. This method gives the opportunity for the first half of the useful lives of the fixed assets to reimburse up to 60 – 70 % of their value.

• disadvantages – in this method, there is no flaws.

- Cumulative method:

• advantages – in the early years, when the intensity of use of the fixed asset object maximum, depreciated large part of its value;

– in the first years of accumulated funds for the replacement of depreciated fixed asset object;

– enables increase in repair expenses depreciation operating system objects falling on the last years of their use without a corresponding increase in cost of production (cost of production) due to the fact that the amount of accrued depreciation in the years decreases.

• disadvantages – a certain degree of complexity.

- Production method:

• advantages – this method is very rational. It is convenient to use when determining the depreciation of vehicles, depending on its mileage, machines and any production equipment.

• disadvantages – due to the difficulty of determining the elaboration of the individual items of fixed assets. While it is not clear how to apply this method in connection with the introduction of a mandatory minimum term asset depreciation.

3.Recommendations for the implementation of the amortization policy at the enterprise in modern conditions

In the third section recommendations for the implementation of the amortization policy at the enterprise in modern conditions

it is planned to develop recommendations to use one of the methods of depreciation policy at the enterprise.

Today there are no clear rules (guidelines) for the choice of the method of depreciation, which would be the best for enterprises of various organizational‑legal forms and industries, property, plant and equipment and how to use them.

Companies can charge depreciation of fixed assets (excluding other noncurrent intangible assets) in accordance with the Regulation (standard) of accounting fixed assets

, approved by the Order of the Ministry of Finance on April 27, 2000 № 92, which entered into force on 1 July 2000 using the following methods: straight‑line; decrease of residual value; accelerated decrease of residual value; cumulative; the production.

The last three are methods of accelerated depreciation. In addition, the company may apply the rules and methods of depreciation, provided by the tax legislation. But, unfortunately, that in practice forced the company to apply only the methods of depreciation. Because it is unlikely the company will now risk to charge depreciation one of the other five methods, because their use is not provided by tax legislation.

Conclusions

Depreciation policy should control the use of depreciation deductions from their destination, meaning it should not slow down technological progress and economic development.

As a result of these measures can be expected to improve the financial results of economic entities activities, creating conditions for the formation of additional investment resources of business entities [3].

The depreciation policy of the company largely reflects the policy of the state, since it is based on the principles, methods and norms of depreciation deductions, approved legislative and normative acts of the Cabinet of Ministers of Ukraine.

The main goal of the amortization policy-increase at the expense of internal sources of the stream own financial resources. In the practice of management, as a rule, is carried out in two ways:

• the formation of the amortization fund (the straight path);

• reduce the amount of tax on profit.

The essence of the amortization policy can be formulated as follows: depreciation policy is an integral part of public policy, which is to optimize the flow of private funds are reinvested in productive activities.

References

- Korotkevich A. K. Basic contradiction depreciation policy of the state // the economist. – № 3, – 2000.

- Thannickal Yu, Sagan So. Amortization policy in Ukraine: history, current state, ways of development // the Economist. – 2002. – № 12.– art.34–38.

- Arnuk C. About the main directions of reforming the depreciation policy // Finance of Ukraine. – 2008. – № 9. – p.93.

- Bulletin of the Technical University of Podillya № 2, Part–1. Khmelnitsky, 2003.

- The economy of an enterprise / edited V. A Garfinkel, V. A Schwander. Year: UNIT–DANA, 2007.

- Business Economics textbook for universities edited C. Garfinkel, In. Sandra – M: unity, 2003. 608 p.

- Business Economics textbook for universities edited C. Garfinkel, In. Sandra – M: unity, 2004. 598 p.

- Business Economics textbook for high schools, edited by E. Kantor – St. PETERSBURG: Piter, 2003 – 352 p.

- Gordienko,–V. catalytic role depreciation policy / C.–Gordienko,–Y. Cluckin,–E. the NARS. – 2008. – № 7. – 54–55 p.

- Руднев Ю. А.,Саприцкий Э. Б. Оптимизация амортизационной политики предприятий как равно изновых направлен оценочной деятельности [Электронный ресурс]. – Режим доступа: http:// www.valuer.ru/ocenshik/s0569807.htm.

- N.–Kondakov. Formation and use of the amortization Fund of reproduction of fixed assets in 2002. // Chief Accountant. 2003. № 2 p. 66–73.

- Balatskii–T, Zabelin–O.

About the policy of depreciation

// the Economist. 2008 № 4. p.47–56.