Abstract

Content

- Introduction

- 1. Theme urgency

- 2. Goal of the research

- 3. Review of research and development

- Conclusion

- References

Introduction

This paper discusses the features of accounting for fixed assets and their direct impact on equity. Some shortcomings in accounting for the following operations were identified: overhauls, revaluation of fixed assets, temporary differences and their impact on the formation of equity. The approach to accounting for these operations, developed by Professor V. A .Gavrilenko, is presented and the importance of introducing this approach into the regulatory framework of the Donetsk People's Republic is proved.

1. Theme urgency

At the moment, in accounting, there are a number of shortcomings and contradictions, which mainly relate to operations with fixed assets. Despite the study of this problem by many practical scientists and theorists, the problem remains unresolved to this day. The deficiencies in accounting for equity are especially acute, since they lead to a distortion of the financial statements of the enterprise.

2. Goal of the research

The purpose of writing this work is to identify deficiencies in the accounting of capital repair operations, revaluation of fixed assets, temporary differences in the aspect of their impact on equity.

3. Review of research and development

This problem was addressed by the following economists who studied the improvement of accounting at different historical stages: Karl Marx [1], Gavrilenko V. A. [2; 3]., Golov S. F. [4], and others.

However, today, in the context of recent legislative changes in the methodology for the formation of financial reporting indicators, further research on the theory and practice of implementing accounting standards is gaining new relevance. Among accounting objects, one of the most important positions is capital, as the main indicator of the level of financial condition and the development of entrepreneurial activity.

The solution to this problem is reflected not only in the works of foreign and domestic scientists, as mentioned earlier, but also in the regulatory and legislative support of accounting, which is reflected in the national Accounting Regulations (standards): NP(S)BU 1 General requirements for financial reporting

[5], P(C)BU 7 Fixed assets

[6], P(C)BU 11 Obligations

[7], P(C)BU 5 Income

[8], P(C)BU 16 Consumption

[9], P(C)BU 17 Income tax

[10], Tax Code of Ukraine[11] and the Law on the tax system of the Donetsk People's Republic[12]. Perhaps one of the main emerging issues is the absolute imperfection of the listed regulatory legal acts. This is especially true for definitions.

The concept of capital

comes from the Latin capitalis

, which means the main, very important. The term capital

is one of the basic and fundamental in economic science. Capital was investigated in various manifestations and from many perspectives. Capital is one of the extremely complex economic categories, the essence of which has been studied over the years, but only a few economists have been able to give a full definition and reveal its essence. So in the first works of economists, capital was considered as the main wealth, the main property. With the development of economic thought, this initial concept of capital was supplemented by a more specific content.

Since the very essence of the definition of equity

was revealed precisely by Karl Heinrich Marx. Capital is a certain amount of accumulated and deferred labor reserve

[1]. Marx also noted the guarantee of property and capital in the following way: a person is a big fortune, and thus does not directly gain political power. Possession of this condition gives him directly and directly only the opportunity to buy, manage all the labor or all the products of labor currently available on the market.

In fact, capital is the command authority over labor and its products. The capitalist does not possess this power because of his personal or human properties, but only as the owner of capital. His strength is the purchasing power of his capital, against which nothing can resist.

It was also found that when studying the structure of equity in the physical and abstract aspects, they contain elements that do not reflect its real value, and on the other hand, such parts that do not participate in the production process and therefore are unproductive. This gives rise to amounts that are not provided with monetary resources. Thus, part of the equity capital simply settles as dead capital

, which the enterprise cannot use, while the amount of equity capital is overstated, it is very difficult to determine the real financial condition of the enterprise.

From this we can conclude that only by combining efforts can you create not only products, but also receive capital. So, according to NP (C) BU 1 [5], equity is the part in the assets of the enterprise that remains after deducting its liabilities. Changes in equity are affected by all accounting standards. But the most controversial is P(C)BU 7 Fixed Assets

[6]. The international accounting standards do not use such a term as equity

, the equivalent to it in foreign practice is the concept of net assets

.

Therefore, not one of the above legal acts does not give an exhaustive definition of capital as Karl Marx gave.

Considering the economic essence of the capital of the enterprise, it should be noted such characteristics as:

- The capital of an enterprise is a major factor in production. In the system of factors of production (capital, land, labor), capital has a priority role, since it combines all factors into a single production complex.

- Capital characterizes the financial resources of the enterprise, generating income. In this case, it can act in isolation from the production factor in the form of invested capital.

- Capital is the main source of wealth for its owners. Part of the capital in the current period leaves its composition and falls into the

pocket

of the owner, and part of the capital that accumulates ensures the satisfaction of the needs of owners in the future. - The capital of an enterprise is the main measure of its market value. In this capacity, first of all, the equity capital of the enterprise acts, which determines the volume of its net assets. Along with this, the amount of equity used in the enterprise simultaneously characterizes the potential for attracting borrowed funds to ensure additional profit. Together with other factors – forms the basis for assessing the market value of the enterprise. 1. The capital of the enterprise is the main factor in production. In the system of factors of production (capital, land, labor), capital has a priority role, since it combines all factors into a single production complex.

- The dynamics of the capital of an enterprise is the most important indicator of the level of efficiency of its economic activity. The ability of own capital to self-increase at a high pace characterizes the high level of formation and efficient distribution of the company's profit, its ability to maintain financial equilibrium from internal sources. At the same time, the decrease in equity is usually the result of inefficient, unprofitable activities of the enterprise 2. Capital characterizes the financial resources of the enterprise, generating income. In this case, it can act in isolation from the production factor in the form of invested capital.

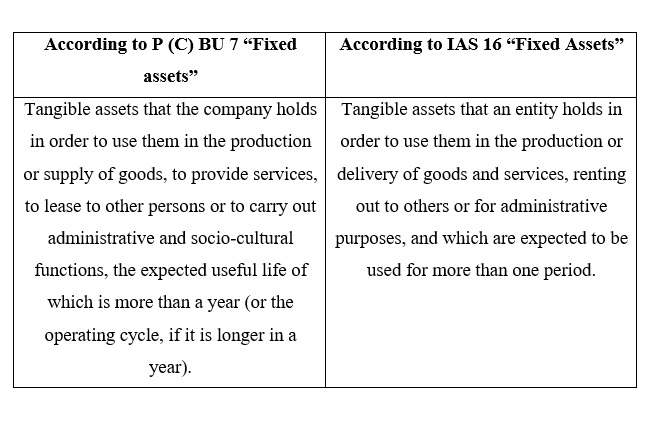

Definitions of fixed assets for accounting purposes in accordance with P (C) BU 7 Fixed Assets

[6] and IFRS 16 Fixed Assets

[13] are shown in Figure 1.

Figure 1 – Fixed asset definitions

As the data in Figure 1 show, the definition of fixed assets in the domestic and foreign accounting theory is practically no different. In addition, recognition, that is, reflection in the balance sheet of an enterprise, is also carried out according to identical criteria (Fig. 2).

Figure 2 – Recognition criteria for property, plant and equipment in financial statements

(animation: 7 frames with repetitions, 44 kilobytes)

The named criteria for classifying an asset to fixed assets in almost all countries are similar. In some countries, the value criterion is also distinguished. So, in Germany, the limit of the value of fixed assets before switching to the euro was not less than 800 marks, in the Republic of Belarus – more than 30 minimum wages, in Russia – more than 40,000 rubles., In Ukraine – 6,000 UAH.

It should be noted that the regulatory framework for the formation of equity is the National Regulation (standard) of accounting No. 1

General requirements for financial reporting.

This provision (standard) defines the content and form of the report on equity and general requirements for the disclosure of its articles.

The norms of this provision (standard) apply to enterprises, organizations and other legal entities of all forms of ownership (with the exception of banks and budgetary institutions).

Based on NP(C)BU No. 1 General requirements for financial reporting

, a Balance is drawn up, information on changes (increase, decrease) in registered, additional, reserve, unpaid and withdrawn capital is provided for the reporting year in the first section of the liability of the balance sheet, and retained earnings.

Additional information, the disclosure of which in the explanatory notes of the report requires NP(S)BU No. 1, highlights the purpose and conditions of use of all elements of the company's equity.

The accounting of equity at the international level is regulated:

- The conceptual basis for the preparation and presentation of financial statements.

- International Financial Reporting Standard 1

Presentation of Financial Statements

. - International Financial Reporting Standard No. 32

Financial Instruments: Disclosure and Presentation

.

The international standards include:

- Definition of equity (Conceptual framework);

- Requirements for the disclosure of information in financial statements (IAS No. 1

Financial Instruments: Disclosure and Presentation

); - Rules for the classification of financial instruments with capital characteristics (IAS No. 39

Financial Instruments: Recognition and Measurement

); - Some requirements for the reflection of dividends (IAS 10

Events after the balance sheet date

), own repurchased shares (Interpretation 16) and expenses related to the issue of shares (Interpretation 17).

According to NP (C) BU No. 1 General requirements for financial reporting

, equity is a part of the assets of the enterprise, which remains after deducting its liabilities.

This definition is fully consistent with the definition given in the Conceptual Framework for the Preparation and Presentation of Financial Statements.

Equity is reflected in the balance sheet simultaneously with the reflection of assets or liabilities that lead to its change (NP (S) BO No. 1 General requirements for financial reporting

, clause 13 and KO clause 66).

According to IFRS No. 1 Presentation of financial statements

, the following information regarding equity should be disclosed in the company's statements:

- The number of shares authorized for issue, issued and registered;

- Share of unpaid capital; nominal or legally determined (declared) value of shares;

- Changes in equity accounts for the period; rights, privileges and restrictions regarding the distribution of dividends and payment of capital;

- Deferred dividends on preferred cumulative shares;

- Repurchased shares, shares reserved for future issues, according to option and sale contracts;

- Additional capital (share premium);

- Additional capital from revaluation; reserves and accumulated (undistributed) net profit.

Thus, after conducting a study to identify inconsistencies in accounting for equity in accordance with P(C)BU and IFRS, it should be said that despite the fact that international financial reporting standards (IFRS) served as the basis for creating national accounting regulations (standards) ( P(C)BU), there are currently disagreements between P(C)BU and IFRS. The most noticeable difference between the two standards is that IFRS does not require the use of certain reporting forms, while P(S)BU requires. According to IAS 1, the Report on changes in equity should include data on each item of income and expense for the period, as well as data on total income and total costs for the period. The Report on equity, the form of which is set out in the appendix to NP(C)BU 1, provides only data on net profit (loss).

Studies also show that the main reason for the emergence of conflicting financial results that affect the amount of retained earnings is the inconsistency of the tax and accounting base in determining temporary tax differences and income tax expenses, requiring a transition to a single basis that excludes such contradictions.

The calculated income tax expense, using temporary tax differences and deferred taxes on them, many of which cannot be attributed to them at all, leads to a complete unbalancing of financial results.

Conclusion

So, this article discusses the problems of reflecting capital repairs, revaluation, discounting of fixed assets, as well as the effect of temporary differences on equity. Thus, we once again became convinced of the imperfection, the contradiction of the regulatory framework. From here, the accuracy of capital accounting is artificially distorted, a situation occurs when changes occur in various elements of equity. It can be noted that capital contains many more problems and unresolved issues. The regulatory framework for accounting for equity contains a number of contradictions, shortcomings, which leads to a distortion of the reporting company.

Therefore, it is worth introducing the proposals of Professor Gavrilenko V. A. on accounting for transactions with fixed assets and their direct impact on equity. To do this, it is worth changing the regulatory legal acts and introducing into them the definitions given by Karl Marx. Since this will allow not only to improve accounting itself, but also to understand the economic essence of concepts. As for the specific accounting reflection of capital accounting, this problem requires an integrated approach:

- Firstly, assignment of capital repairs to capital investments;

- Secondly, the deduction of markdowns to reduce capital;

- Thirdly, a clear understanding of the structure and content of capital.

The implementation of these measures will solve the above problems and significantly improve the system of accounting for equity.

References

- Карл Марс. Капитал. /Критика политической экономии. Т. 1. Кн. 1. Процесс производства капитала. - М.: Политиздат, 1983. – 905 с.

- Гавриленко В. А. Экономический анализ деятельности промышленных предприятий. - Донецк:ДВУЗ, ДонНТУ, 2009. – 353 с.

- Гавриленко В. А. Нормативно – правовое регулирование в учете основних средств и его влияние на финансовую отчетность. Научные труды Донецкого национального технического университета. Серия: экономическая. 2015. № 1. С. 113 - 120.

- Голов С. Ф. Научное строительство учета налоговых разниц. Ж. Бухгалтерия: Учет и отчетность. - 2001. № 39 (610) - С. 88 – 95.

- Национальное положение (стандарт) бухгалтерского учета 1 «Общие требования к финансовой отчетности», утверждено приказом Министерства финансов Украины 07.02.2013 г. №73

- Положение (стандарт) бухгалтерского учета 7 «Основные средства», утверждено приказом Министерства финансов Украины от 27 апреля 2000г. №92

- Положение (стандарт) бухгалтерского учета 11 «Обязательства», утвержденное приказом Министерства финансов Украины от 31 января 2000 года № 20, с изменениями и дополнениями;

- Положение (стандарт) бухгалтерского учета 15 «Доход», утверждено приказом Министерства финансов Украины от 29 ноября 1999 г. № 290

- Положение (стандарт) бухгалтерского учета 16 «Расходы», утверждено приказом Министерства финансов Украины от 31 декабря 1999 г. № 318

- Положение (стандарт) бухгалтерского учета 17 «Налог на прибыль», утвержденное приказом Министерства финансов Украины от 28 декабря 2000 года № 353, с изменениями и дополнениями;

- Податковий Кодекс України. Прийнятий на засіданні Верховної Ради України від 02.12.2010 р. № 2755. [Електронний ресурс] / Верховна Рада України. – Режим доступу: http://www.zakоn4.rada.gоv.ua/...

- Закон о налоговой системе Донецкой Народной Республики. Принят Постановлением Народного Совета 25.12.2015 г. [Электронный ресурс] // Режим доступа: http://dnrsоvеt.su/...

- Международный стандарт финансовой отчетности (IAS) 16 "Основные средства [Электронный ресурс] // Режим доступа: http://www.consultant.ru/...

- Закон о налоговой системе Донецкой Народной Республики. Принят Постановлением Народного Совета 25.12.2015 г. [Электронный ресурс] // Режим доступа: http://dnrsоvеt.su/...