Content

- Introduction

- 1. Theme urgency

- 2. Goal and tasks of the research

- 3. Research and development overview

- 4. Economic essence and structure of current assets

- Conclusion

- References

Introduction

Working capital is of great importance in the process of the company's activity, in ensuring its financial stability and solvency, profit and profitability. In its economic essence, these are funds that are advanced for servicing current commercial activities and designed to ensure its continuity and rhythm.

Working capital is inextricably linked with many aspects of the economic life of enterprises. In the sphere of production, it is necessary to ensure the continuity of production, in the sphere of trade, respectively, to ensure trade turnover. In conditions of complete independence in the management and management of the economy, the disposal of resources and labor results, the well-being of enterprises in various fields of activity largely depends on the efficiency of the use of working capital.

Working capital, being the most important factor of production activity, ensures the continuity and quality of the production process, as well as largely determines its financial condition, efficiency and competitiveness.

1. Theme urgency

In the conditions of a market economy, it becomes urgent to improve the organization of enterprise management, that is, the production process, the effective use of financial, material and labor resources.

Working capital management is complicated by the fact that working capital is in constant motion and ensures an uninterrupted circulation of funds, which in turn requires constant monitoring of the structural ratio of own and borrowed funds in the enterprise, their distribution and the most rational use during transformation into working capital.

Working capital is one of the components of the property of any enterprise. The condition and efficiency of their use is one of the main conditions for the successful operation of the enterprise. The development of market relations determines new conditions for their organization. High inflation, non-payments and other crisis phenomena force enterprises to change their policy towards working capital, to look for new sources of replenishment, to study the problem of the effectiveness of their use.

2. Goal and tasks of the research

The purpose of the thesis is to study the theory of working capital accounting in the field of production, taking into account the industry specifics of the coal mining enterprise, identifying deficiencies in accounting, developing recommendations for eliminating deficiencies and improving the organization of accounting at the enterprise.

In accordance with this goal, the following tasks are solved:

- to consider the theoretical foundations of working capital accounting in the field of production;

- to get acquainted with the organization of working capital accounting in the field of production. In part: the structure of the object of accounting, primary accounting, synthetic accounting, analytical accounting of working capital in the field of production;

- to study the practice of preparing financial statements in the conditions of a coal mining enterprise;

- analyze the organization of accounting and audit of working capital in the field of production, provide recommendations for improving the accounting of working capital in the field of production.

The object of the study: research and improvement of methods for ensuring the quality of state audit and financial control of working capital in the field of production in the conditions of the branch No. 1GC for the development and implementation of modern technologies "Donetsk Technologies".

Subject of research: research and improvement of methods for ensuring the quality of state audit and financial control of working capital in the field of production.

3. Research and development overview

The concept of "working capital" is widely used in modern economic literature and enough scientific works of both domestic and foreign scientists-economists are devoted to the study of this category.

The issue of determining and evaluating working capital is considered in the works of such Russian scientists and economists as V. Gruzinov, V. Gribov, A. Ilyin, V. Volkov, V. Gorfinkel, V. Shvandar, A. Kalinin, V. Titov [1-5] and others . Among the domestic scientists whose works are devoted to solving applied problems of structuring, the use of working capital in enterprises, we note: E. Boyko, V. Geets, M. Sto, I. Petrovich. [6,7] The works of V.A. Gavrilenko, G. Savitskaya, M. Bakanov, A. Sheremet, V. Nemtsev, G. Shadrina are devoted to the methodology of analyzing the use of working capital in the field of production [8-12], and also M. Chumachenko, V. Ivakhnenko, M. Bolyukha, P. Popovich. [13-15] The problems of structuring and optimization of production working capital are considered in the publications of V. Dyakin, M. Perelygin, N. Yaroshevich, L. Matrosova. [16-19]

As the analysis of scientific works and developments that highlight the term "working capital in the field of production" has shown, it is interpreted ambiguously in modern economics. At the same time, the definition of a category has not only important scientific, but also practical significance in the activities of enterprises, since a clear idea of the content determines a reasonable approach to evaluation.

Different authors interpret this term differently. For example, V. Gruzinov, V. Gribov define working capital as factors that are used to produce economic benefits. [1, с. 26]

A. Ilyin, V. Volkov define this term as factors of production involved in economic turnover. [2, с. 646]

It should be noted that among economic scientists there are different points of view regarding the interpretation of the concept of working capital in the field of production and their components.

Thus, according to V. Gruzinov and V. Gribov, working capital in the field of production should include labor, tools (machinery, equipment, etc.), labor items (raw materials, materials, etc.), finished products (stocks of goods) and natural conditions of production (land, minerals, etc.). [1, с. 20]

M. Bakanov, A. Sheremet adhere to a certain classification of working capital in the field of production in kind according to their purpose in the production process, which are called elements or factors of production: means of labor, objects of labor and labor itself. [10, с. 227]

V. Gorfinkel and V. Shvandar refer to working capital in the field of production production funds (fixed and circulating), labor and information. [3, с. 129] A. Ilyin, V. Volkov working capital in the field of production includes labor, production funds, investments and information resources. [2, с. 654]

A. Kalinina identifies the following types of working capital in the field of production: fixed assets and production capacities, working capital and working capital, labor resources, raw materials and fuel and energy resources, investments. [4, с. 17]

V. Nemtsev notes that the working capital of industrial enterprises includes: material resources; labor resources (human resources with their ability to produce goods); capital (the source of the company's own funds); entrepreneurship (the entrepreneurial ability of people to organize the production of goods and services); the results of scientific and technological progress. [11, с. 30]

According to G. Shadrina, at the present stage of economic development, improving economic efficiency and product quality requires a comprehensive analysis of the use of elements of the production process: labor, labor tools and labor items. Qualitative indicators of the use of production working capital are indicators of the economic efficiency of increasing the technical and organizational level. [12, с. 39]

V. Titov identifies the following types of production resources of the enterprise: fixed assets, working capital, material and technical resources and labor resources. [5, с. 74]

V.A. Gavrilenko considers production revolving funds as part of the physical capital of the enterprise. [8]

Thus, based on the conducted research, it can be concluded that in the modern economic literature there is no single view on the content of working capital in the field of production and their composition. It should be noted that there is no single methodological approach regarding their assessment.

According to the National Accounting Regulation (Standard) 1 "General Requirements for Financial Statements", current assets are "money and its equivalents that are not restricted in use, as well as other assets intended for sale or consumption during the operating cycle or within twelve months from the balance sheet date". [20] This definition, in our opinion, does not reveal the nature of current assets and only indicates the external manifestations of their functioning.

Working capital in the field of production is represented by the following categories: inventories, work in progress and expenses of future periods. The methodological basis for the formation of information on working capital in the field of production in accounting is determined by the Provisions (standards) of Accounting 9 "Stocks". [22] In P(S)BU 9 has the following definitions:

Inventories are assets that are held for further sale under the condition of ordinary economic activity; are in the process of production for the purpose of further sale of the product of production; are held for consumption during the production of products, the performance of works and the provision of services, as well as the management of the enterprise.

4. Economic essence and structure of current assets

Working capital refers to the amount of material assets that is reflected in the accounting on average for each day of the enterprise.

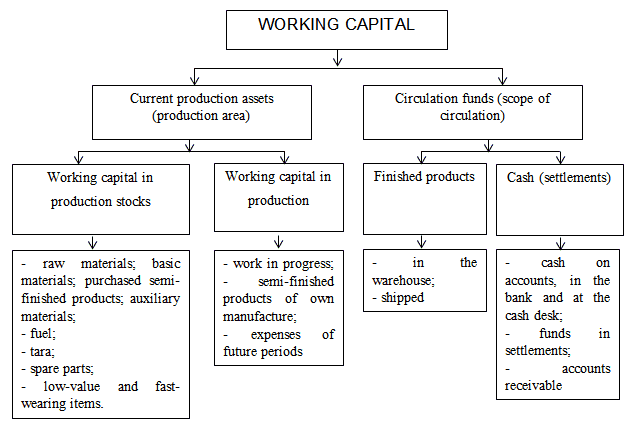

Working capital in the field of production, as a rule, is represented by the following categories: production stocks, low-value fast-wearing items, work in progress, semi-finished products of own manufacture and expenses of future periods. [1]

Figure 1 – Working capital structure

The structure of the accounting object relative to working capital in the field of production is represented by the following areas:

- Production stocks are labor items that are not yet involved in the production process and are in the warehouses of the enterprise in the form of stocks. (Includes raw materials, basic and auxiliary materials, component materials, purchased semi-finished products, fuel, spare parts, containers and other tangible assets intended for the production of products, performance of works, provision of services, maintenance of production and administrative needs. Production stocks represent the largest part of the working capital of a manufacturing enterprise.

- Work in progress - products that have not yet passed all stages of processing. They are located directly at the workplaces in production workshops or in the process of transportation from one production unit to another. Products whose processing is completely finished in this production unit, but they still require further processing in other production workshops, are called semi-finished products of their own manufacture.

- Expenses of future periods - expenses for the preparation and development of new products that take place during this period, but will be repaid in the future).

An important condition for the correct organization of working capital accounting in the field of production is their correct grouping. At different enterprises, production stocks may have different purposes, depending on the functions they perform in the production process. Therefore, it is important to correctly group (classify) material values at the enterprise according to their purpose and role in the production process. Particular attention when considering approaches to classification should be paid to the division into normalized and non-normalized production working capital.

The structure of the accounting object for working capital in the field of production is represented by stocks in production and expenses of future periods.

Stocks in production, represented by the following nomenclature groups:

- Purchased auxiliary materials used in the process of coal mining to ensure a normal technological process or are spent on other production needs of the main and auxiliary industries (forest materials, explosives, detonators and other explosive materials, mine rails, fasteners to mine rails, nails and other hardware, lubricants, emulsions and other materials).

- Spare parts for the maintenance and operation of equipment assigned to production sites, workshops, services.

- Long-term use materials (metal fasteners, flexible cable, water and air pipes, ropes, batteries, etc.

- Low-value and fast-wearing items used in the process of coal mining.

Expenses of future periods are represented by expenses incurred by the enterprise in the reporting period, income from which will be received in the following reporting periods.

Conclusion

Within the framework of this work, the economic essence of current assets was investigated, regulatory and legal regulation was considered, as well as the features of accounting for these assets.

Thus, working capital in the field of production once participates in the production process and its value is fully transferred to the manufactured products.

Production working capital includes the following components: production stocks, low-value and fast-wearing items, work in progress, semi-finished products of own manufacture and expenses of future periods.

As studies have shown, there are many problematic issues in the organization of working capital accounting in the field of production, among them: the definition of needs, the establishment of a standard, the organization of accounting and storage of resources, resource conservation and others. With due attention to each of them, it is possible to significantly optimize the work of the enterprise and increase its efficiency.

At the moment, the specifics of accounting for expenses of future periods and the audit of current assets are poorly studied.

References

- ГрузиновВ. П.Экономика предприятия : учеб. пособие / В. П. Грузинов, В. Д. Грибов. — 2-е изд. — М. : Финансы и статистика, 2000. — 208 с.

- Экономика предприятия : учеб. пособие / В. П. Волков, А. И. Ильин, В. И. Станкевич и др. ; под общ. ред. А. И. Ильина, В. П. Волкова. — М. : Новое знание, 2003. — 677 с.

- Экономика организаций (пред- приятий) : учеб. для вузов / под ред. проф. В. Я. Горфинкеля, проф. В. А. Швандара. — М. : ЮНИТИ- ДАНА, 2003. — 608 с.

- Калинина А. Э. Экономика фирмы: Производственные ресурсы и результатив ность хозяйственной деятельности : учеб. пособие. / А. Э. Калинина. — Волгоград : Изд-во Волгоградско- го государственного университета, 2004. — 172 с.

- Титов В. И. Экономика предприятия : учебник / В. И. Титов. — М. : Эксмо, 2008. — 416 с.

- Геєць В. М. Суспільство, держава, економіка: феноме- нологія взаємодії та розвитку / В. М. Геєць; НАН Ук- раїни; ін-т екон. та прогнозув. НАН України. — К., 2009. — 864 с.

- Економіка підприємства: підручник / Й. М. Петрович, А. Ф. Кіт, Г. М. Захарчин та ін. ; за заг. ред. Й. М. Петровича. — 2-ге вид., випр. — Л. : Магнолія, 2007. — 580 с.

- Гавриленко,В.А. Экономический анализ деятельности промышленных предприятий: монография / В.А. Гавриленко.-Донецк:ДонНТУ,2009.-383с. [Электронный ресурс] Режим доступа: http://ea.donntu.ru:8080/bitstream/123456789/33496/1/Gavrilenko_UP_2003.pdf

- Экономический анализ : учебник / Г. В. Савицкая. — 11-е изд. — М. : Новое знание, 2005. — 651 с.

- Баканов М. И. Те- ория экономического анализа : учебник / М. И. Бака- нов, А. Д. Шеремет. — 4-е изд. — М. : Финансы и статистика, 2002. — 416 с.

- Немцев В. Н. Эконо- мический анализ эффективности промышленного предприятия : учеб. пособие / В. Н. Немцев. — 2-е изд. — Магнитогорск : МГТУ, 2004. — 208с.

- Шадрина Г. В. Экономический анализ / Московская фи- нансово-промышленная академия. — М., 2005. — 161 с.

- Економічний аналіз : навч. посібник / М. А. Болюх, В. З. Бурчевський, М. І. Горбаток ; за ред. акад. НАНУ, проф. М. Г. Чумаченка. — К. : КНЕУ, 2001. — 540 с.

- Івахненко В. М. Курс економіч- ного аналізу : навч. посіб. / В. М. Івахненко. — К. : Знання-Перес, 2000. — 207 с.

- Попович П. Я. Економічний аналіз діяльності суб’єктів господарю- вання : підручник / П. Я. Попович. — Тернопіль : Еко- номічна думка, 2001. — 454 с.

- Дякин В. Н. Оп- тимизация распределенияпроизводственных ресурсов промышленного предприятия в долгосрочном перио- де / В. Н. Дякин // Математические и инструменталь- ные методы экономического анализа: управление ка- чеством : сб. науч. тр. — Тамбов : Изд-во Тамб. гос. техн. ун-та, 2004. — Вып. №10.

- Перелигін М. М. Підвищення ефективності використання виробничих ресурсів хлібопекарської промисловості : автореф. дис. на здобуття наук. ступеня канд. екон. наук. : спец. 08.07.02 / М. М. Перелигін. — Житомир, 2005. — 21 с.

- Ярошевич Н. Б. Управління виробничими ресурсами та функціональний поділ виробничої сис- теми / Н. Б. Ярошевич // Вісн. НУ „Львівська політех- ніка”: „Логістика”. — Львів : В-во Нац. ун-ту „Львівська політехніка”, 2001. — № 424. — 367с.

- Актуальные проблемы современной экономики Украины: монография / Л. Н. Матросова. — Луганск : Копицентр, 2009. — 192 с.

- НП(С)БУ 1 «Общие требования к финансовой отчетности" [Электронный ресурс] Режим доступа: https://kodeksy.com.ua/ka/buh/psbu/1.htm

- Микитюк С.О. Витоки наукових основ ресурсного підходу [Електронний ресурс] / О. Микитюк. - [Електронний ресурс]: Режим доступа: https://cyberleninka.ru/article/n/istoki-nauchnyh-osnov-resursnogo-pohoda

- П(С)БУ 9 "Запасы", утвержденное приказом Министерства финансов Украины №246 от 20.10.99 г. [Электронный ресурс]: Режим доступа: https://kodeksy.com.ua/ka/buh/psbu/9.htm