Abstract

Content

- Introduction

- 1. Theme urgency

- 2. Goal and tasks of the research

- 3. Overview of research and development

- 4. Current and planned results

- Conclusion

- References

Introduction

Insurance is one of the most important socio-economic institutions, whose activities are actually affects an increase in the efficiency of social development, contributes to maintaining the achieved level of well-being, as well as solutions to pressing problems of public and personal safety. The great practical importance of insurance is that it is a system oriented to damages caused to the property or the identity of persons dangerous random events.

At the end of 2011 in Ukraine, 438 insurance companies licensed to conduct insurance business. Interestingly, in recent years more than 50% of the total receipts of insurance payments account for private insurance, about 20% - the proceeds of property insurance businesses and individuals, and 16% - for compulsory insurance and only 5% - for liability insurance. But nowadays the amount of contributions and the personal automobile insurance has been steadily growing. Thus, the Ukrainian insurance market occur changes in the development of certain types of insurance.

1. Theme urgency

The relevance of determining the optimal system of discounts for vehicle insurance is to attract new customers to the insurance company and its limitations on filing small claims. The choice of the discount will depend from profit of the insurance company.

2. Goal and tasks of the research

The aim of the study is to analyze system of the land vehicles insurance operating in Ukraine and abroad, the research bonus-malus system using mathematical modeling methods and the definition of an optimal system of discounts bonus-malus system for a particular insurance company.

The purpose of the study leads to the nature of the tasks:

- To calculate the probability distribution of policyholders discounts for groups of the current discounts system;

- To calculate the profit forecast for the bonus-malus discounts system;

- To determine the optimal system of discounts for a particular insurance company by mathematical modeling.

The object of study is the system of discounts "bonus-malus" which is used for vehicle insurance and the profit company can get using this system.

The subject of the study are models and methods of discounts and vector probability distribution over the levels of insurance calculating.

The information base for the study served as the statements of some insurance companies, as well as materials published in periodicals and special publications. We used thematic resources available online.

The practical significance of the study is defined by the ability to use his findings and provisions for the development of concepts and target the program for the particular insurance company development.

3. Overview of research and development

In the automobile insurance industry two overriding are identified: motor vehicle insurance and compulsory insurance CASCO citizen of the vehicle owners. The objects of compulsory insurance, the risks of which they should be insured, and the minimum size of insurance premiums are determined in the Law of Ukraine "About insurance" [1].

Among to the total number of insurance types could be attributed to the automobile liability insurance and to the vehicle itself. At the same time, in accordance with the current legislation of Ukraine, if Hull is a voluntary form of insurance, the insurance of civil responsibility is vested in both the compulsory and voluntary insurance. Under the contract of voluntary liability insurance car owners could increase the amount of insurance payments under the amount specified in the contract of compulsory insurance.

At present, the legal regulation of auto insurance in Ukraine are the main legislative acts: the laws of Ukraine "About insurance" [2], "About vechile insurance", the head 67 of the Civil Code of Ukraine and a list of by-laws, in particular, the license terms of introducing compulsory insurance of civil liability of owners of vehicles, approved by order of the State Commission for Regulation of Financial Services Markets of Ukraine dated 23 December 2004 № 3178, the Regulation on the features of contracting compulsory insurance liability of owners of vehicles, approved by order of the State Commission for Regulation of Financial Services Markets of Ukraine dated April 11, 2006 number 5619, the Charter of the Motor (Transport) Insurance Bureau of Ukraine, and so on.

The domestic auto market has been actively developed, and being one of the most dynamic markets. World crisis has worsened his condition - about 28.7% in 2008, decreased charges for car insurance [3], which was the consequence of the fall in consumer lending. Increased insurance rates: if before the crisis tariff CASCO for cars was 7.3% of the sum insured per year, then in 2009 - is 10.8% [4].

Insurance rates play a significant role in attracting clients. It is important for insurer to insure a car from the largest number of risks with the lowest cost, the insurer must attract more insurance premiums, but make fewer insurance claims. This explains the relevance and practical importance of the set problem.

The essence and the problem of auto insurance are considered in O. Vovchak, S. Osadets, V. Trinchuk, T. Yavorskaya [5-8], etc.

In the formation of the insurance rate, a system of individual discounts, called "bonus-malus" [1]. Coefficient "bonus-malus" on each hull is approved by the insurance company on their own. The more insurance claims, the lower class. And the fewer, the higher class.

However, a study of insurance claims for a specific driver (or lack thereof) does not guarantee that in future years there will be a similar situation, and even the possibility of their (insurance claims) occurrence a can be calculated fairly conventional.

The driver can repeatedly create prerequisites of an accident, but after a certain period of time, never get into an accident. However, such a driver's chance of getting into an accident in future periods is much larger and, consequently, higher probability of occurrence of the insured event than accurate driver of the vehicle, which does not violate the rules of the road.

Thus, in the "bonus-malus" must take into account not only the number of insurance claims, and a number of small and large offenses such as speeding traffic, running a red light, parking in unauthorized places, etc. This information allows the insurance company to determine the probability of occurrence of insured events for a particular driver more accurately. Availability of such data by the emergence since the beginning of this year, CCTV cameras on highways. In addition, information on violations of traffic rules by drivers is available in the forms of warnings.

In automobile insurance, despite the large number of variables, a priori, in each tariff class, you can see the big difference in the quality of driving.

The subject of bonus-malus - the person for which bonus-malus class to calculate:

a) the registered owner of the vehicle;

b) the registered owner of the vehicle, if the owner is a natural person, and if specified in the public register of the traffic police;

c) specified in the State Register of GAI owner (regardless of whether the owner of a natural or legal person), if the owner of the vehicle - a legal entity;

d) specified in the State Register of traffic police by the owner if the owner is a legal entity, but the owner of the vehicle - a natural person.

Bonus-malus class - a class of risk, defined for a particular bonus-malus vehicle group specific bonus-malus subject:

a) class malus - an increase of insurance risk;

b) class bonus - reducing the risk insured;

c) class bonus-malus the first insurance contract - the class without some risk.

Insured event - it's an accident that resulted in losses of applied and the insurance company has taken at least one solution on Compensation Insurance, with the exception of an accident when a vehicle driven by a person who uses the tool unlawful manner, that is, if the vehicle at the time of an accident dropped out of the possession of the owner or authorized user is not his fault, but because of the wrongful acts of another person, and this can be documented.

In the late 1950s, put forward the idea of the adjustment of tariff rates, which would be carried out according to the "stories" of insurance claims for each insured. Such a system is called "bonus-malus" [9], which penalizes insurers responsible for one or more accident allowances to insurance premium (Malus), and encourages policy holders who have not committed insurance claims discount (bonus). The main purpose of these systems - apart from increasing interest in defensive driving - is better accounting of individual risk for each, eventually paid premium corresponding to its natural frequency of insurance claims.

Current and planned results

1) The basic characteristics of the "bonus-malus";

2) Investigated three different systems of "bonus-malus": Belgian, Brazilian and Ukrainian;

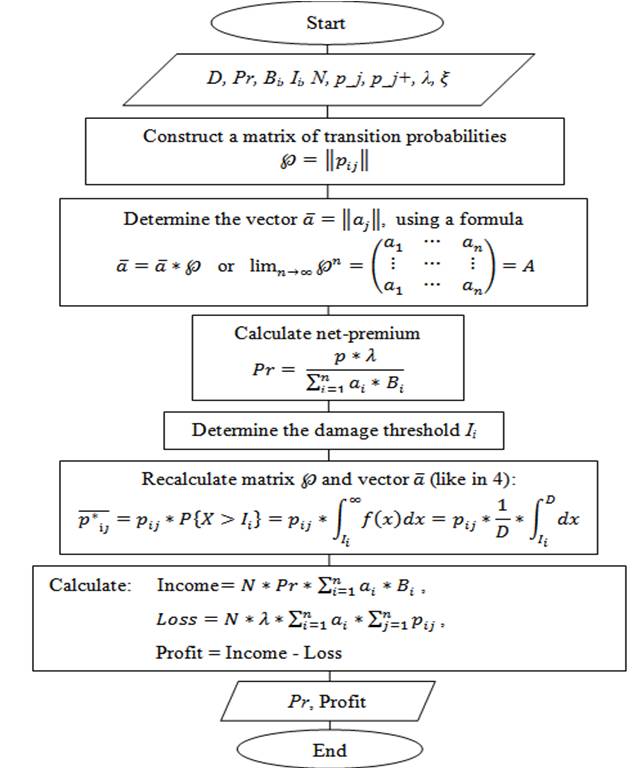

3) An algorithm of the income of the insurer using the established system of "bonus-malus" calculation;

Figure 1 - The algorithm of the insurer income and net-premium calculation

4) A numerical study of the model on the statistics of the insurance company and the optimal system of discounts for the company determined;

5) It is planned to modify Ukrainian system of discounts, in order to make it more profitable for insurers and loyal to policyholders.

Conclusion

According to the goal of research in the work of an analysis of existing rebates "bonus-malus" by the methods of mathematical modeling, which revealed a wide variety of systems in the world. Each country has its own system, and some - there are several. The insurance company has the right to choose the system itself that it will use working with insurers.

On the basis of this analysis were requirements to the selected system. This was followed by using a "bonus-malus" discounts system mathematical model for forecasting profits, which has determined the probability distribution of policyholders discounts for groups and income calculates of the insurer using the installed system.

On the basis of the model was an algorithm of profit calculation and net premiums written, with which the numerical investigation of the model. The algorithm was implemented apparatus of Markov chains and the theorem of Markov chain regular vector stabilizing. We studied three different systems: Belgian, Brazilian and Ukrainian. Numerical study was performed according to the statistics of the insurance company "AXA Insurance", specifically - CASCO insurance.

During comparing the results obtained optimal system of discounts was found, which gives the greatest return for a fixed number of customers. Such a system is the Belgian system of "bonus-malus" discounts.

References

1. Про обов’язкове страхування цивільно-правової відповідальності власників наземних транспортних засобів: Закон України №2902-IV від 22 вересня 2005 р. (із змінами і доповненнями) // Відомості Верховної Ради України (ВВР). – 2006. – №1. – с. 3.

2. Про страхування: Закон України від 18 жовтня 2001 р. (із змінами і доповненнями) // Відомості Верховної Ради України. – 2011. – №2. – с. 2

3. Страховой рынок Украины в 1 квартале 2009 г. [Електронний ресурс]. – Режим доступу: http://forinsurer.com/news/09/06/05/18990.

4. Краще застрахуватися комплексно [Електронний ресурс]. – Режим доступу: http://a2.utoukraine.com.ua.

5. Вовчак О.Д. Страхові послуги / Вовчак О.Д., Завійська О.І.– Львів: Компакт-ЛВ, 2005. – 656 с.

6. Осадець С.С. Страхування. 2-ге вид., перероб. і доп. / С.С. Осадець. – К.: КНЕУ, 2002. – 599 с.

7. Тринчук В.М. Експертне дослідження щодо розвитку ринку автострахування України в умовах невизначеності / Тринчук В.М. // Страхова справа. – 2007. – №4 (28). – с. 52-59.

8. Яворська Т.В. Страхові послуги / Яворська Т.В. – К.: Знання, 2008. – 350 с.

9. Jean Lemaire. Bonus-malus systems in automobile insurance / Jean Lemaire: Kluwer Academic Publishers, 1995. – 563 с.

10. Jean Lemaire. Bonus-Malus Systems: The European and Asian Approach to Merit-Rating / Jean Lemaire: North American Actuarial J. – 1998. – №2. – с. 26-38