Abstract

Content

- Introduction

- 1. Goal and tasks of the research

- 2. Existing types of reinsurance analysis

- 2.1 Basic concepts of the reinsurance process

- 2.2 Reinsurance types classification

- 2.3 Statement of the research problem

- 3. Mathematical model of reinsurance coverege variables classification and formalization

- Conclusions

- References

Introduction

Each insurance company seeks to create a sustainable, stable insurance portfolio, which would consist of the greatest possible number of insurance contracts, but with a low degree of responsibility for each accepted risk. The taken level of risks must comply with the financial capabilities of the insurance company, so if insured event or number of insurance cases advanced, payment of insurance losses compensation would not reflect on its financial position [1].

To protect themselves from possible financial difficulties insurers have resorted to transfer taken risks with help of the Institute of reinsurance to other insurers. Reinsurance is a system of economic relations in the course of which the insurer, taking the insurance risks of various sizes, some of the responsibility for it passes on certain agreed terms to other insurers in order to create a balanced portfolio of insurance [2].

1. Goal and tasks of the research

The goal of research is to analyze the types of reinsurance and creation of an optimal insurance company portfolio reinsurance cover. To achieve this goal it is necessary:

- to conduct a research of the reinsurance types;

- to analyze the advantages and disadvantages of proportional and non-proportional reinsurance species;

- to develop a mathematical model of insurance portfolio reinsurance protection.

The object of research in this paper is the process of reinsurance. The subject of reinsurance are models and schemes.

2. Existing types of reinsurance analysis

2.1 Basic concepts of the reinsurance process

Reinsurance is a special type of insurance. Its meaning is to transfer part of the risk (s) in the responsibility of other specialized insurer [3].

The process of risk transferring named the ceding of risk. The insurer, which transfers the risk named the assignor, and the one that takes this risk – the assignee. The next transfer by assignee (partially or fully) of the risk to the reinsurer is called retrocession. Insurance company, transferred to a third party risk in reinsurance, called retro assignor, and an organization that accepts this risk is called retroassignee [4].

Transferring risks to reinsurance, the reinsurer is entitled to a bonus (commission on profits that the reinsurer can get the implementation by the contract). The bonus is paid annually on the amount of net profit received by the insurance organization [5].

Process of reinsurance outlined above is shown on figure 2.1. This scheme is given in [6].

Figure 2.1 – The scheme of interaction between participants of the reinsurance (animation, 7 frames, 10 reps)

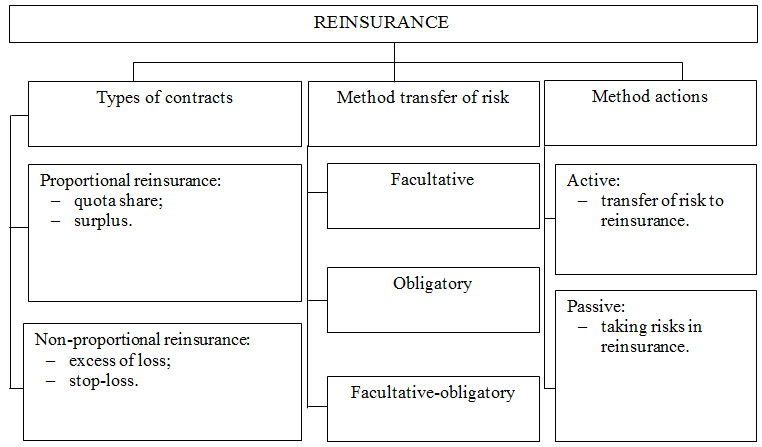

2.2 Reinsurance types classification

In [7] reinsurance is classified according to the following classification criteria:

- types of contracts – proportional and non-proportional;

- method of risk transfer – obligatory, facultative and facultative-obligatory;

- actions method – active and passive.

This classification is shown in figure 2.2.

Figure 2.2 – Diagram showing the relationship of the reinsurance process elements

Proportional reinsurance treaty provides that the reinsurer's share in each transmitted it to cover the risk is determined by the pre-specified ratio of the assignor's own participation.

Quota Share (QS). By its terms, the insurer (reinsurer) transfers to the reinsurer agreed percentage of all the risks taken by them for a specific type of insurance or a group of related insurance. In this part of the reinsurer receives a premium and the reinsurer reimburses all losses paid by the insurance accepted.

Surplus Reinsurance. This is type of reinsurance, where risk for insurance assignor received exceeds a predetermined fraction of its own retention. This excess part of the sum own retention of insurant is called the excess amount, and is being a subject to a proportional redistribution between other parties to the treaty [8].

Non-proportional reinsurance essence is when the compensation, provided by the reinsurer, is determined only by the size of damage and being independent of the insured sum. The share of loss that will pay each of them varies depending on the actual incurred losses amount.

Excess of loss. Reinsurance mechanism comes into action when the final amount of the loss on the insured risk exceeds the limit, specified in the contract amount. The contracts of reinsurers loss excess reimburse only those losses that exceed the insurer (the assignor) the priority.

Stop-loss. The reinsurer participates in damages only in cases where the loss ratio for a given period exceeds the contracted percentage of reinsurance.

Facultative reinsurance method is characterized by the complete freedom of parts to the reinsurance contract. Obligatory reinsurance provides for the mandatory transfer of the reinsurer agreed in advance for all the risks coatings. The reinsurer also have to take these risks in accordance to the terms of contract. When facultative-obligatory reinsurance facultativy provided to the insurer (the assignor), and obligatory – for the reinsurer [9].

Active reinsurance is to transfer, the passive – to accept the risk. In practice, the active and passive reinsurances are often produced by the same insurance company at the same time.

2.3 Statement of the research problem

The study of existing types of reinsurance conducted in section 2.2 showed that all the proportional reinsurance contracts inherent characteristic: losses and premiums on original policies are distributed between the assignor and the reinsurer in the proper proportion, linked to the insurance sum. Non-proportional reinsurance contracts are flexible enough, easy to process and organize.

Quota Share contracts for insurance companies are more balanced and give sustainable financial results. The drawback is that the contract passed and shares for a small risks that the assignor could keep for himself.

This drawback eliminates the surplus contract. The insurer sets two limits - upper and lower. Thus, in the reinsurance passed excess over the lower limit, but not higher than the top.

Excess of loss reinsurance provides financial equilibrium of the whole entire insurance portfolio. However the service of such contracts is technically difficult and disadvantageous to the assignor.

Stop-loss provides coverage after other types of reinsurance in the amount of losses, that exceed a certain percentage of earned premium.

In practice, many modifications of proportional and non-proportional reinsurance treaties applied, but there are no general strategies for using combinations of reinsurance contracts.

In this regard, it is necessary to develop a mathematical model allowing to carry out reinsurance coverage under a separate contract, type of insurance and the insurance portfolio in general.

3. Mathematical model of reinsurance coverege variables classification and formalization

Many types of insurance:

|

(3.1) |

Common set of contracts:

|

(3.2) |

where Di – many contracts of the insurance type number і;

N – number of insurance types;

ni – many contracts of the insurance type number i;

dij – contract number j of the insurance type number.

Contract dij characterized by parameters: sij – insurance amount, tarij – rate, tsij – insurance term, tnij – moment of the contract start, svij – insurance payment, tvij – moment of the insured event:

|

(3.3) |

Revenue for the contract dij:

|

(3.4) |

Revenue for the type of insurance Si:

|

(3.5) |

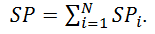

Insurance company portfolio revenue:

|

(3.6) |

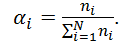

Each type of insurance has its share αi:

|

(3.7) |

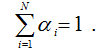

Structure of the insurance portfolio is given by [12-14]:

| α=(α1, α2, ... ,αN) | (3.8) |

|

(3.9) |

Analysis of the structure of the insurance portfolio allowed to distinguish three levels reinsurance cover:

- lower level – for each reinsurance contract;

- medium – reinsurance for each insurance type;

- upper level – the reinsurance portfolio of the insurance company.

On the lower level effective methods of reinsurance are quota share, surplus contracts and combinations which allow to avoid large payments under one contract.

At the middle level in order to avoid losses associated with a large number of insurance payments under the contracts justified the excess of loss contracts is to use.

On the upper level reinsurance task is not to maximize profit but to protect the insurance company from ruin.

Conclusions

An analysis of reinsurance types showed their advantages and disadvantages. All the contracts of proportional reinsurance inherent characteristic: losses and premiums on original policies are distributed between the assignor and the reinsurer in the proper proportion, linked to the insurance sum. Non-proportional reinsurance treaties are sufficiently mobile, easy to process and to organize. This explains the growing interest of insurers to non-proportional treaties.

Mathematical model has developed insurance company portfolio reinsurance cover, which has allowed distinguishing three levels of protection: the lower level, middle level and the upper level.

On the lower level effective methods of reinsurance are quota share, surplus contracts and combinations which allowed avoiding large payments under one contract. At the middle level in order to avoid losses associated with a large number of insurance payments under the contracts justified the excess of loss contracts is to use. On the upper level reinsurance coverage task is not to maximize profit but to protect the insurance company from ruin.

At the time of writing this essay master's work is not yet complete. Final completion: December 2013. Full text of the work and materials on the topic can be obtained from the author or his head after that date.

References

- Архипов А.П. Страхование. Современный курс: Учебник / А.П. Архипов, В.Б. Гомелля; под ред. Е.В. Коломина. – М.: Финансы и статистика, 2008. – 446 с.

- Журавлев Ю.М. Страхование и перестрахование: теория и практика / Ю.М. Журавлев, И.Г. Секерж. – М.: АНКИЛБ, 1993. – 184 с.

- Макаренко Н.Л. Страховоедело / Н.Л. Макаренко, Н.Н. Косаренко. – М.: Национальный институт бизнеса. Ростов-на-Дону: изд-во «Феникс», 2003. – 608 с.

- Базилевич В.Д. Cтраховий ринок України / В.Д. Базилевич. – К.: Знання, 1998. – 374 с.

- Щербаков В.А. Страхование: Учебное пособие / В.А. Щербаков, Е.В. Костяева. – М.: «КНОРУС», 2007. – 312 с.

- Казанцев С.К. Основы страхования: Учебное пособие / С.К. Казанцев. – Екатеринбург: изд. ИПК УГТУ, 1998. – 101 с.

- Український ринок перестрахування. Проблеми та перспективи [Електронний ресурс]. – Режим доступу: http://tristar.com.ua/1/art/ukrainskii _rynok _perestrahovaniia__problemy_i_perspektivy_.html

- Закон України «Про страхування» від 7 березня 1996 року // Відомості Верховної Ради України. – № 85/96. – 1997. – с. 12

- Турбина К.Е. Теория и практика страхования: Учебное пособие / К.Е Турбина. – М.: «Анкил», 2003. – 704 с.

- Абрамов В.Ю. Страхование: теория и практика / В.Ю. Абрамов. – М.: "Волтерс Клувер", 2007. – 221 с.

- Вовчак О.Д. Страхова справа: Підручник / О.Д. Вовчак. – К.: «Знання», 2011. – 391 с.

- Карри И. Прикладная статистика / И. Карри. – М.: МГУ, 2000. – 500 с.

- Колесников Н.И. Факультативное перестрахование имущественных рисков – Н.И. Колесников. – М.: МГУ, 1994. – 172 с.

- Рябикин В.И. Актуарные расчеты / В.И. Рябикин. – М.: Финстатинформ, 1996. – 320 с.