Abstract

Contents

- Introduction

- 1. Theme urgency

- 2. Goal and tasks of the research

- 3. Overview of research and development

- 4. The main directions of the competitive strategy of commercial banks

- 5. Simulation assessment of the level of competitiveness of the commercial bank

- Conclusion

- References

Introduction

At the present stage of commercial banks are in competition for the preservation and improvement of their position in the market of financial services. In Ukraine, on 01.01.2013 has 176 banks, according to the National Bank of Ukraine [1]. Banking competition intensifies in times of financial instability and a significant reduction in customer confidence in the banking institutions. Competition in the banking sector encourages commercial banks to offer customers a broader range of products and services at more affordable prices and better quality, making them a customer-oriented. Without increasing the competitiveness of the bank and the services can not be effectively ceases the activity of the bank, allowing a profit and gain a stable position.

Analysis and evaluation of the competitiveness of the commercial bank allows the bank's management to develop an effective competitive strategy as part of strategic planning. Development of methods for assessing the competitiveness of the bank and the account of the effect of individual factors of competitiveness is an important scientific task that can be achieved by designing an appropriate dynamic simulation model.

1. Theme urgency

Relevance of this topic is enhanced by increasing competition in the banking market in terms of financial instability, a significant decrease in customer confidence in the banking institutions, the desire of banks to avoid unnecessary costs, maximize profits from their activities.

2. Goal and tasks of the research

The aim of the study is to develop a simulation model of assessing the level of competitiveness of the commercial bank, which will manage the efficiency of a commercial bank, as well as help determine the ways to enhance competitiveness.

Realization of this goal necessitates the following tasks:

- Study the theoretical foundations of a development strategy for the commercial bank;

- Research and analysis of the development strategy of commercial bank and factors affecting it;

- Considering the concept and essence of banking competition and competitiveness;

- Study of forms, levels and methods of evaluation of banking competition in the market of financial services;

- Development and formalization in the ideology of system dynamics simulation of a commercial bank;

- Development of a simulation model of assessing the level of competitiveness of the commercial bank.

Object of study : the activities of the commercial bank

Subject of study : the strategy of development of modern commercial bank under the influence of competition.

As part of the master plan to get topical scientific results in the following areas:

- Defining the strategy of development of commercial bank in the market of financial services;

- Identify cause and effect relationships that impact on the competitiveness of a commercial bank;

- Formation methodical approach to the study of the competitiveness of a commercial bank in terms of the basic functions performed by the competition;

- The identification and classification of the factors that directly and indirectly affect the competitiveness of a commercial bank, in a constantly changing market conditions, the analysis and evaluation of which will increase the competitiveness of the credit institution;

- Development of a simulation model of assessing the level of competitiveness of the commercial bank.

3. Overview of research and development

Challenge competitive rivalry in the market a lot of attention paid to in the works of Adam Smith, A. Cournot, F. Edgeworth, J. Robinson, E. Chemberlen, F.Hayek, A. Marshall and others. The main issues of controversy these economists were the concept and essence of competition, its drivers and the impact on the process of market pricing of their followers R. Bertrand, A. Herfindahl, M. Rozenblyud, E. Lind and others, developed the theory of the competition by offering an alternative model of assessment and the use of market power [2].

Greatest generalization theory of competition has become a part of the classical school of political economy in the XVIII century. Adam Smith is considered the founder of the theory, defining in his "An Inquiry into the Nature and Causes of the Wealth of Nations" [4] competition as a competition, which changes the price level – increases with decreasing supply and decreases with an increase in demand. Smith argued that "consumers and sellers compete in the market with favorable terms of purchase and sale" [4]. In his view, that competition is based on the principle of the "invisible hand" of the market, which coordinates the activities of entities making act in the prescribed manner, displacing inefficient production and participants; market competition leads to equilibrium by the interaction of supply and demand for goods.

Representatives of the Austrian School of Economics, Menger [5] and L.von Mises [6] shared the view the competition – it is a struggle for economic resources. I. Kirzner [22] identified competition with the activities of the market, believing that these concepts are inextricably linked to each other. Feature of business entities, in his opinion, there is a need to constantly monitor the potential and prospects making the most profitable decisions.

In the XIX century Neoclassical continued research approach to understanding the competition, but viewed it in the context of competition for scarce economic resources and means to consumers. Hayek [7] examined competition in the context of the discovery of new knowledge. According to him, market information, opportunities and prospects are not concentrated in one place, and to obtain it is necessary to search, using their own expertise and knowledge. F.Hayek seen the new knowledge to the main competition, and profit – the main purpose of the entity. He believed that the process of "discovery" provides information on the presence and amount of resources, the needs of customers, their location, etc.

Among the recent theoretical developments of one of the most significant is the concept of Porter [8]. He criticized the notion that the determining factor of competitiveness and prospects of the company is the market share, highlighting four factors – the forces of competition, and the fifth factor – the rivalry – and considered proper competition. He notes that each of these factors must be considered when developing the strategy of the company because they determine its profitability. When sequential strategy that differed from the strategy of competitors, the market entity has the ability to get better position in the market. To summarize, it should be noted that in the evolution of the socio-economic formations concept of "competition" has suffered substantial development. Competition is objectively important category of today's market, which is interpreted in terms of three major scientific and methodological approaches – behavioral, structural and functional.

Domestic legislation regulates the process of competition in the various sectors of the economy. The basic regulatory framework is the Constitution of Ukraine (Article 42), the Law of Ukraine "On Protection of Consumer Rights" [9], the Law of Ukraine "On Protection Against Unfair Competition" [10], the Law of Ukraine "On Protection of Economic Competition" [11]. Subject of competition is a competitor – or other financial institution providing the market products or services, is regarded by consumers as substitutes for products (services) – Original [12].

Theoretical and practical aspects of banking competition and the competitiveness of commercial banks in the financial services market, considered by scholars such as V.V. Gerasimenko [13], Y.S. Zaruba [14], L.I Fedulova [15], J.P Pikush [16], A.E Sedish [17], etc.

Y.A Zaruba, believes that "the competitiveness of the bank – a comprehensive, integrated feature of its activities, which reflect the degree of success of the operation of the bank in a competitive market in the course of storage and expansion of its market position, which implies the ability to use resources effectively and get in a moderate-risk profit of not less than the corresponding figure competitors"[14].

According to J.P. Pikush, the competitiveness of the bank – the ability to carry out effective profitable activity at a certain level in a competitive market for financial services [16].

Despite the breadth of research in the field of banking competition, evaluation of the competitiveness of the commercial bank is considered only at the conceptual level. For a more detailed analysis of the assessment of the competitive commercial bank and the determination of its development strategy, requires practical implementation of a dynamic simulation model.

4. The main directions of the competitive strategy of commercial banks

Obviously, for the same purpose can move in different ways. For example, you can increase profits by reducing costs. But you can achieve this by increasing the utility and the consumer of the product produced by the credit institution. Different banks, depending on the circumstances, on the basis of their potential and their power to make different decisions about how they will solve this problem. Selecting the way to achieve the objectives and shall be the decision about the bank's strategy. As can be seen, if the establishment meets the objectives of the question, to which the credit institution shall endeavor, if the plan of action to achieve the objective answers the question of what to do to achieve this goal, the strategy answers the question of which of the possible ways of how the organization will go to the goal. The choice of strategy means choosing the means by which the organization is to achieve its objectives [18].

Selection strategy and its implementation are the main content of strategic management. There are two opposing views on the understanding of the strategy. The first understanding of the strategy is based on the following process. Accurately defined end state to be achieved through a long period of time. Next is fixed, we need to do in order to achieve that end state. After this a plan of action, broken down by time intervals (five-year and quarter), the implementation of which should lead to the ultimate, well-defined objective. Basically, it is the understanding of the strategy existed in systems with a centrally planned economy. With this understanding of the strategy – it is a concrete long-term plan to achieve a specific long-term goals, and develop a strategy – it's finding the target and making a long-term plan

In the second understanding strategy, which is used in strategic management, strategy – a long-term qualitatively determining the direction of the organization relating to the scope, means and forms of its activity, the system of relationships within the organization, as well as the organization's position in the environment, leading the organization to its objectives [18]

Figure 1 – The criteria for determining the competitiveness of the bank and its services

(animation: 4 frames, 5 cycles of repeating, 104 kilobytes)

Comprehensive study of foreign and intra-factors allow a sufficient degree of accuracy to determine the level of competitiveness of the bank and its main competitors, as well as the competing credit products and services offered to the population. In determining competitive banking strategy commonly used already developed world economic science and policy approaches. The most common strategic alternatives for the business sector are growth and contraction. There are different variants of the growth strategy. The most well-known and applicable to banking is the matrix of "goods-markets" American economist I. Ansoff (figure 2.) [19].

Figure 2 – The matrix of I.Ansoffa

The matrix of Ansoff suggests the use of four alternative strategies to increase sales [19]:

- The market penetration;

- Market development;

- Product Development;

- Diversification.

Market penetration strategy assumes that the bank gets to the already established market and it offers the same product (or service) as the competitors. This strategy is preferred if the target market is growing or is not saturated [20].

There are three variants of this strategy of market penetration:

- Increase the use of existing products;

- Luring customers from competitors;

- Attracting new customers.

Market development strategy means that the transnational bank seeks to expand the market for services rendered, but not at the expense of penetration of existing markets and by creating new markets or market segments. In the application of this strategy include the following elements [21]:

- identification of new areas of application of banking products;

- promotion of existing products into new segments;

- geographical expansion.

This strategy is used in those cases where a well-known product (service) identified new areas of application and its starting to get new group potrebiteley.Chto As for the promotion of products in new segments, such a strategy is used when a newly introduced product has been successfully received by the intended target markets initially. Thus, the service-oriented initially only to affluent consumers (for example, plastic cards), banks are beginning to offer and target groups with lower incomes. Regarding the penetration of the financial institution into new geographic markets may be noted that in the past, geographical expansion are carried out through the opening of new branches, representative offices, subsidiaries.

talking about strategies of multinational banks. We can distinguish three types of banking innovation [21]:

- adaptive innovation;

- functional innovation;

- fundamental innovation.

Adaptive innovation – this is the least complicated form of innovation, it involves minimal changes in the product or service and do not require any changes in consumer behavior. At the same time, this innovation is also very simple in terms of copying competitors. An example would be the formation of inter-related packages that are already familiar to consumers of banking services.

Functional innovation involves maintaining the function of the product, but the nature of the function changes. Buyers are able to meet their needs for a new and better way. Thus, this type of innovation requires certain changes in the habits of consumers.

Fundamental innovation – this is the most complex type of innovation, which implements a new concept or idea, whereby there are new functional qualities. The injected product is completely new and satisfies a need that had not noticed or not satisfied sufficiently.

Thus, the competitive strategy of the bank is influenced such elements as: expanding the range of services offered and the development of geographic markets, the market introduction of new services [21].

5. Simulation assessment of the level of competitiveness of the commercial bank

For the development a dynamic simulation model of assessing the level of competitiveness of a commercial bank, it is necessary to determine the competitiveness of the bank's internal factors, the influence of which can be analyzed using graph cause-and-effect relationship, shown on the figure 3.

Figure 3 – The diagram cause-and-effect relationships of factors affecting the competitiveness of commercial banks

Construction of a diagram cause-and-effect relationships of factors affecting the competitiveness of the bank, can develop a model of assessing the level of competitiveness of the bank. In developing the model evaluation of the competitiveness of the bank should consider its financial performance, and to evaluate its financial position.

Dynamic model consists of a set of interrelated elements that are included in the model as variables. The main component of a dynamic simulation model of a commercial bank's profit.

To assess the competitiveness of commercial banks were definitely following parameters:

- the competitiveness of services;

- credit risk

- index of bank risk.

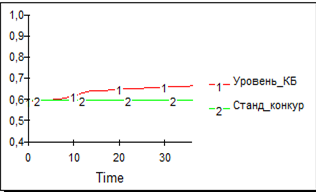

Figure 4 shows the dynamics of the competitiveness of the bank during the analyzed period.

Figure 4 – Dynamics of the level of competitiveness of the bank

The developed a simulation model of assessing the level of competitiveness of the commercial bank to determine the value of key financial and economic indicators in future periods that characterize the activities of the bank, to influence the level of competitiveness of the bank, changing its basic components, and enhances the effectiveness of the bank's management

Conclusion

Rating competitive commercial bank includes: constructing a model of a commercial bank and a model assessment of the level of competitiveness of the commercial bank. Developed a dynamic simulation model for assessing the level of competitiveness of the commercial bank to determine the value of key financial and economic indicators in future periods that characterize the efficiency of the financial activities of the bank, to analyze the level of competitiveness of the bank changing its basic components, and enhances the effectiveness of the bank's management.

Model allows to determine the level of competitiveness of the bank in general to better assess the need to introduce additional parameters that characterize the competitiveness of the bank. The results will enable the bank management to more accurately develop a strategy for the bank, given its competitiveness.

Based on calculation of the level of competitiveness and identifying the bank's management may determine its competitive edge and to determine the future development of the banking business.

Further studies assessing the level of competitiveness should be directed on the one hand to develop the competitiveness of the evaluation mechanism that will allow on the basis of the available stages of evaluation of the competitiveness of the bank and the appropriate methods of analysis to develop a management solutions to improve the competitiveness of the bank, and the other – on the development of information analytical evaluation of the competitiveness of the bank, which will reduce the loss of information between the different levels of management, and will help to make informed, timely management decisions.

In writing this essay master's work is not yet complete. Final completion: December 2013. Full text of the and materials on the topic can be obtained from the author or his manager after that date.

References

- Официальный сайт Национального банка Украины: [Электронный ресурс]. – Режим доступа: http://www.bank.gov.ua/

- Кудашева Ю. С. Совершенствование методики оценки конкурентоспособности коммерческого банка : дис. .к. э. н : спец. 08.00.10 «Финансы, денежное обращение и кредит» / Кудашева Юлия Сергеевна. – Ставрополь, – 2007. – 186 с.

- Павлова Е.Е. Конкурентоспособность российского банковского сектора: Базовые составляющие и способы оценки: дис. .к. э. н : спец. 08.00.10 «Финансы, денежное обращение и кредит» / Павлова Екатерина Евгеньевна. – Ростов-на-Дону, – 2008. – 238 с.

- Смит А. Исследование о природе и причинах богатства народов / А. Смит. — М. : Эксмо, – 2007. – 960 с.

- Menger C. Principles of economics / C. Menger. - Vienna: Braumu

- Мизес Л. Человеческая деятельность: Трактат по экономичеcкой теории / Л. Мизес. — М.: Экономика, – 2000. — 878 с.

- Хайек Ф. А. Познание, конкуренция и свобода / Ф.А. Хайек. – СПб. : Пневма,– 1999. – 212 с.

- Портер М. Е. Конкурентное преимущество: Как достичь высокого результата и обеспечить его устойчивость : пер.с англ. / М.Е.Портер. – М. : Альпина Бизнес Букс, – 2005. – 715 с.

- Закон Украины «О защите прав потребителей» от 24 мая 2001 года №2438-III

- Закон Украины «О защите от недобросовестной конкуренции» от 18 декабря 2008 года N 689-VI.

- Закон Украины «О защите экономической конкуренции» от 11.01.2001 № 2210-III.

- Закон Украины «О финансовых услугах и государственном регулировании рынков финансовых услуг» от 12.07.2001 № 2664-III

- Герасименко В. В. Экономическая сущность и особенности банковской конкуренции и конкурентоспособность банков / В. В. Герасименко // Вестник Национального банка Украины. – 2011. – 8 с.

- Заруба Ю. С. Конкурентоспособность коммерческого банка / Ю. А. Заруба // Финансы Украины. – 2001. – № 2. – С. 119-124.

- Федулова Л. И. Управление конкурентоспособностью банков в условиях трансформационной экономики: монография / Л. И. Федулова, И. П. Волощук // – К. : Науч.мир, – 2002 . – 301 с.

- Пикуш Ю.П. Управление конкурентоспособностью банка в условиях финансовой либерализации : дис. .к.э.н : спец. 08.00.10 «Финансы, денежное обращение и кредит» / Пикуш Юрий Петрович. – Сумы, 2006. — 27 с.

- Седых А. Е. Оценка эффективности управления продуктами банка // Экономический простор. – 2009 . – № 22/1. – 9 с.

- Виханский О.С. Стратегическое управление. Учебник. 2-е изд., перераб. и доп. — М.: Гардарика, – 1998. — 296 с.

- Ansoff I. The new corporative strategy. NY. 1998

- Юданов А.Ю. Конкуренция: теория и практика. - М.: АКАПИС, 2000. - С. 67.

- Doyle. P. Marketing. Management and Strategy. NY. 1999

- Kirzner I. M. Competition and Entrepreneurship. / I. M. Kirzner. – Chicago : The University of Chicago Press, 1978. – 242 p.