Summary of research and developments

Соntent

- Introduction

- Main part of work

- 1. Scientific–theoretical bases of cost management

- 2. Methodical principles of cost management

- 3. Recommendations about improvement of cost management

- Conclusion

- References

Introduction

Actuality. In modern conditions of instability an economic situation, competition increase in the market and reduction of the income, search of effective methods of management by economic activity gains the increasing relevance. Under these conditions stability and development of any enterprise depends first of all on creation of an effective cost management system.

Work purpose. The purpose of a master's thesis is further development of theoretical bases and development of methodical recommendations about improvement of a cost management system of the enterprise.

Problems of work. For achievement of this purpose in work the following tasks were set:

- to consider essence and classification of expenses;

- to prove need of cost management;

- to consider cost management systems;

- to prove ensuring efficiency of activity of the enterprise;

- to consider functional and cost analysis of management;

- to prove cost management from the point of view of life cycle of production;

- to develop methodical recommendations about cost management system of the enterprise;

Object of the research: management process by enterprise activity in modern conditions.

Subject of the research: theoretical bases and economic approaches to management of enterprise expenses.

Analysis of the researches. Theoretical and methodical approaches of cost management of the enterprises were considered in works of many scientists, such as: F. Butinec, S. Golov, I. Davidovich, K. Druri, T. Karpova, V. Lebedev, L. Napadovskaya, A. Turilo, A. Cherep and others. However, despite rather large number of the scientific works, not all aspects of a component and actual for development of the enterprises of a problem are found out. It predetermines need of continuation of researches for this area.

Methods of the researches. Scientific works and methodical development both domestic, and foreign scientists in the field of management of enterprise expenses formed a theoretical and methodical basis of a master's thesis. For the solution of the tasks set in work the next methods were used: induction and deduction (at definition «management of expenses»), the analysis and classification; approaches: information (analysis of sources of information), system (consideration of management by expenses as complex system), process approach. Information base of researching are standard and legislative acts of Ukraine, general provisions of scientific works by domestic and foreign scientists, statistical information of Goskomstat in Ukraine, materials of research conferences and the Internet.

Scientific significance of the research consists of development theoretical bases and development of methodical recommendations about improvement of a cost management system of the enterprise.

Approbation results of work: The basic, scientific and practical provisions of work were presented at All–Ukrainian scientific conferences: conference of students and young scientists «Modern problems in management of investment, innovative activity» in 2012–2013, «Financial policy: global and national priorities of formating and realization» in 2012, «Actual problems of economic and social development of production sphere» in 2013.

Main part of work

In introduction the actuality of a subject of a master's thesis is considered, the research objective, object, a subject and research methods are given, practical value of results reveals..

1. Scientific–theoretical bases of cost management

In the first section of work «Scientific–theoretical bases of cost management» consider essence of expenses, their classification, need of management of expenses locates, and also cost management systems are considered.

There is a set various theories of definition expenses at the enterprise. So in matter interpretation among domestic scientists were engaged: M. Bakanov, A. Fridman, A. Makarova, F. Butinec, S. Golov, I. Davidovich, T. Karpova, V. Lebedev, L. Napadovskaya, A. Turilo, A. Cherp, Siroma N. and others. As the matter was considered in works of foreign authors, such as: K. Druri, D. Shim, D. Sigel, C. Horngren, J. Forster, R. Entoni, J. Ris and others.

Proceeding from definitions of expenses, it is possible to draw a conclusion that expenses is a monetary form of the involved factors of the production necessary for implementation by the enterprise of the production and realizatsionny activity spent for a certain period.

Management of expenses is a dynamic process which consists in achievement of high economic result. Underestimation a role of management by expenses predetermines considerable expenses of the enterprise that negatively influences level of production expenses and results of a financial condition of the enterprise [1].

Analyzing statistical data of the Ministry of Finance of Ukraine for 2008–2012 the tendency growth of expenses, especially in the industry sphere is observed [2]. The rise in prices for raw materials, energy carriers, salary increase, economic and financial policy of the state and so on can be the reasons of increase in expenses.

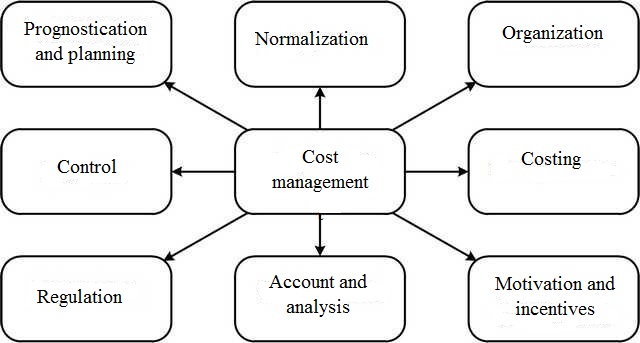

Management of expenses at the enterprise provides performance of all functions of management, that is functions have to be implemented through elements of administrative process (fig. 1).

Figure 1 — Elements of cost management

Each elements of system is directed on achievement common goals of the enterprise and carries out accurately put tasks [3].

Considering the review of economic literature in the field of management expenses for existing systems and methods of control over expenses, it is possible to divide on traditional and modern. Traditional methods treat: poprotsesny; the job order; poperedelny and standard methods. Modern systems are presented such as: standard–cost, direkt–costing, method of the accounting of prime cost (АВС), and others.

Most often at the enterprises applly traditional methods, but in modern conditions of market economy the use only traditional methods of management are applied not enough, in this regard, it is necessary to use on the example of foreign countries new modern cost management systems [4].

The system «standard–cost» is the most widespread among modern systems. The essence of this system is that on the basis of the established standards it is possible to define previously the sum of expected expenses for production and realization of products and calculate prime cost of unit a product for determination of the prices. At this system information on available deviations is use for adoption of operational administrative decisions [5].

In difference from «standard–cost», feature of «direkt–costing» systems is that it is based on classification of expenses for constants and variables. In this system prime cost of production production is considered and planned only regarding variable expenses. Constant expenses don't include in calculation of prime cost of products and as expenses of this period write off from the got profit during that period in which they were developed [6].

One more of modern control systems is the system of АВС (Activity Based Costing) which consists in distribution of the nomenclature realized inventory items to three unequal groups A, B, and С . This system is founded on the principle: production consumes kinds of activity, and the production activity consumes resources. For determination of cost there are forming expenses factors which connect concrete kinds of activity and the corresponding expenses, and as act as an activity criterion as expenses change in proportion to activity scale [7].

2. Methodical principles of cost management

In the second section «Methodical principles of cost management» ensuring effective activity of the enterprise locates, the analysis is carried out functional and cost, and also management of expenses from the point of view of life cycle of production locates. For ensuring effective activity of any enterprise it is necessary to study a ratio of output (realization) of production with expenses and profit. For this purpose it is necessary to carry out the analysis of a point of profitability which serves one of the most important ways in solution of many problems in management, as at the combined application with other methods of the analysis, accuracy is quite sufficient for justification of administrative decisions in real life.

The point of profitability is that level which the enterprise needs to reach what not to have a loss (completely to compensate all expenses), it is that boundary which the enterprise has to reach what not to go out of business.[25] Initial in definition a point of profitability there is a research of structure expenses and allocation among constants and variables. It is necessary to divide the size of constants and variable expenses as at their inexact definition we will receive incorrect result in formation a point of profitability [8].

Under modern conditions for increase efficiency of the enterprises is necessary to apply modern techniques of diagnostics and management of enterprise expenses, among which the special attention is deserved functional and cost by the analysis (FSA) as an effective way of identification reserves an expenditure of material, labor and monetary resources, and also decrease in expenses.

The most known experts in development of FVA are such people as: Danchenko O., Karpunin M., Krijanovskaya E., Ploshadka B., Muravskaya V., Rovenskaya V. and others.

The functional and cost analysis (FVA) is a practical method of complex, system researching of objects, which is directed on providing the minimum expenses on production, realization or operation, when ensuring consumer properties [9].

Main goal of this analysis is identification of decrease in expenses at the expense of more effective options, the best ratio, between the consumer cost of a product and costs of his production [10].

When forming strategy of business management, and strategy of cost management, features life cycle of a product are very important, because let out product is the main source of the current profit and future cash flows [11].

3. Recommendations about improvement of cost management

In the third section «Recommendations about improvement of cost management» it is planing to develop recommendations about rational management of expenses on the basis of concrete economic–mathematical model and to prove efficiency of the offered actions.

Conclusion

Increase of a role of cost management in modern conditions is predetermined by need of achievement by each enterprise of an optimum level expenses for production and production realization on which its successful activity depends.

Providing an optimum level of expenses will give the chance of appropriate conditions for growth, competitiveness of production, and also there will be a soil for the long–term economic growth of the enterprises.

The following tasks were solved in the course of work: the essence and classification of expenses were considered; it was reasonable need of management of expenses; cost management systems are considered; ensuring effective activity of the enterprise is reasonable; the analysis of management is carried out by expenses functional and cost; management of expenses from the point of view life cycle of production is reasonable; management of expenses from the point of view life cycle of production is reasonable.

References

- Баканов М.И., Мельник М.В., Шеремет А.Д., Теория экономического анализа // М.: Финансы и статистика, 2005. — 536 с.

- Сайт статистики України // [Електронний ресурс]. — Режим доступу:http://www.ukrstat.gov.ua

- Колісник Г.М. Складові системи управління витратами підприємницьких структур // [Електронний ресурс]. — Режим доступу: http://archive.nbuv.gov.ua/portal/soc_gum/evu/2011_17_2/Kolisnuk.pdf

- Козаченко А.В. Методы управления затратами // [Электронный ресурс]. — Режим доступа: http://www.elitarium.ru/2010/11/10/metody_upravlenija_zatratami.html, 2010 г.

- Друри К. Учет затрат методом стандарт–кост / Пер. с анг. под ред. Н.Д. Эриашвили. — М.: Аудит, ЮНИТИ, 1998. — 224 с.

- Нападовська Л.В. Управлінський облік: Монографія. — Дніпропетровськ: Наука і освіта, 2000. — 450 с.

- Голубовський Л.В. Аналіз сучасних методів управління витратами / Л. Голубовський // Галицький економічний вісник, 2010. — №1(26). — С. 187–192.

- Ратушна О.П. Теоретичні основи розрахунку точки безбитковості // [Електронний ресурс]. — Режим доступу: http://eztuir.ztu.edu.ua/1669/1/18.pdf

- Ровенська В.В. Генезіс фунуціонально–вартісного аналізу // Вісник Донбаської державної машинобудівної академії, 2008. — № 3Е (14). — С. 297–302.

- Организация ФСА на предприятии / Е.П. Крыжановская, В.В. Муравская и др. — М. : Финансы и статистика, 2009. — 128 с.

- Грещак М.Г., Коцюба О.С. Управління витратами: Навч.–метод. посібник для самост. вивч. дисц. — К.: КНЕУ, 2002. — 131 с.