Content

- Introduction

- 1. Relevance of the topic

- 2. The purpose and objectives of the study

- 3. Research and Development Overview

- 4. Cost accounting for the production of thermal energy. Technological features of thermal energy production and their impact on the organization of cost accounting

- 5. Calculation of the cost of thermal energy and calculation of heat loss at the production stage

- Conclusions

- List of sources

Introduction

Thermal energy is an important industry of the state’s energy complex. For this production sector, it is especially important to ensure unhindered and uninterrupted supply of thermal energy to consumers. Improving the efficiency and stability of the industry will allow the uninterrupted supply of heat and hot water to residential buildings and enterprises, which is very important.

The energy industry is different from other material industries and has its own specific features: the continuity of the process of production, transmission and consumption of thermal energy; lack of ability to create thermal energy reserves.

In thermal power engineering there are a number of economic problems: deterioration of heating networks; government tariff policy does not stimulate industry development; there are losses of thermal energy during its transmission, which adversely affects the efficiency of enterprises; high costs for the production and repair of equipment; outdated regulatory and training base in terms of cost accounting and calculating the cost of thermal energy. Energy companies should identify opportunities for technological and organizational measures to solve the problem of modernization of heat supply without a shock rise in tariffs.

Currently, there is a tendency to save energy and increase efficiency in the energy industry. The main impetus for energy saving in the field of thermal energy is the accelerated growth in the cost price for thermal energy.

Reducing the cost of thermal energy has a positive effect not only for the enterprise, but also for consumers. The cost of energy in the energy sectors is taken into account in the cost of the heat tariff, therefore, reducing the cost, and, as a result, reducing the tariff, brings economic benefits to the consumer (population).

One of the important economic results of the financial and economic activities of the enterprise is the level of production costs. Therefore, of great importance for an economic entity is the effective management of production costs of the enterprise. In the production process, the organization bears certain production costs that are necessary for the manufacture of products (works, services).

In domestic practice, the term production costs

began to be used to describe all production costs for a certain period. Costs are the consumed raw materials, material, labor and other resources, valued in value terms. Also, in addition to the cost of production, the organization bears the additional costs associated with the sale (transportation costs and others).

An important economic indicator of the work of any energy company engaged in the production of thermal and electric energy is the cost of energy. The cost of energy includes all the total costs in the process of production of thermal energy, which are expressed in cash. The cost of production is one of the most important quality indicators, which in a generalized form reflects all aspects of the financial and economic activities of the enterprise and characterizes the level of use of all resources at the disposal of the enterprise.

1. Relevance of the topic

The relevance of the chosen topic is that tariffs for thermal energy should be set economically justified taking into account the real costs of producing thermal energy. The order of cost accounting, cost management and cost reduction of thermal energy are of great importance for enterprises and the population, due to the social significance of energy production. Cost management improves production efficiency, positively affects the results of the financial and economic activities of the enterprise.

2. Purpose and objectives of the study

The aim of this work is to assess the state of cost accounting and calculation of the cost of production of thermal energy, to analyze the costs and cost of production of thermal energy on the basis of the SPP Donetsk Gorteploset

, as well as to determine heat losses at the production stage.

The main objectives of the study:

- determination of technological features of thermal energy production and their impact on the organization of cost accounting;

- to identify the features of the consolidated accounting of production costs and calculation of the cost of thermal energy;

- determine the heat loss at the stage of its production.

Object of research : SPP Donetskgorteploset

DONBASSTEPLOENERGO

, whose main activity is the provision of heat and energy, hot water and a couple.

Subject of research : a set of questions on organizing cost accounting and calculating the cost of production and transmission of thermal energy.

3. Research and development overview

The issues of cost accounting and costing in the energy sector, the problems of reducing the cost of production of energy enterprises were considered by Gavrilenko V.A. [1], I. Zabrodin [2], A. Koshkarova [3] and other authors.

4. Accounting for the cost of heat energy production. Technological features of heat energy production and their impact on the organization of cost accounting

The process of thermal energy production at energy enterprises has its own specific features. The process of generating thermal energy consists of separate technological stages (phases), on the basis of which the structure of the entire production is built. The number of technological stages by which the grouping of production costs occurs depends on the process and method of production [3].

At SPP Donetskgorteploset

the production of thermal energy, hot water and steam occurs with the help of steam and hot water boilers.

The number of technological stages by which the grouping of production costs in boiler plants takes place depends on the production process, available equipment and initial energy resources. Costs of heat production will be reflected in the workshops.

In accordance with the list and composition of the articles on calculating production costs at the SPP Donetskgorteploset

for general production costs for servicing the main production, the cost centers determined the following structural units of the servicing production:

– Shop No. 1 for the repair, installation and commissioning of thermal automation and measuring instruments (is engaged in the repair and maintenance of instrumentation, remote controls, automation and technological protection, controls technological parameters);

– electrical laboratory;

– Workshop No. 2 for the repair of heating equipment and heating networks;

– workshop for the repair and operation of electrical equipment;

– central warehouse;

– mechanical repair shop;

– repair and construction workshop;

– production and chemical laboratory (organization of water treatment processes, monitoring the operation of equipment, devices and premises under the control of the workshop);

– production and technical laboratory;

– production and emergency service;

– gas station;

– expenses of managerial personnel for production servicing.

Further, overhead costs are allocated to the following accounts:

– 2302 power Generation generated by KGU

;

– 231 Total cost of thermal energy

;

– 2310 thermal energy Production

;

– 2311 transportation of heat energy

;

– 2312 heat energy Supply

;

– 232 cost Of district heating services

;

– 233 Cost of centralized hot water supply services

.

Power enterprises are subject to special requirements for the reliability, continuity and continuity of the process.

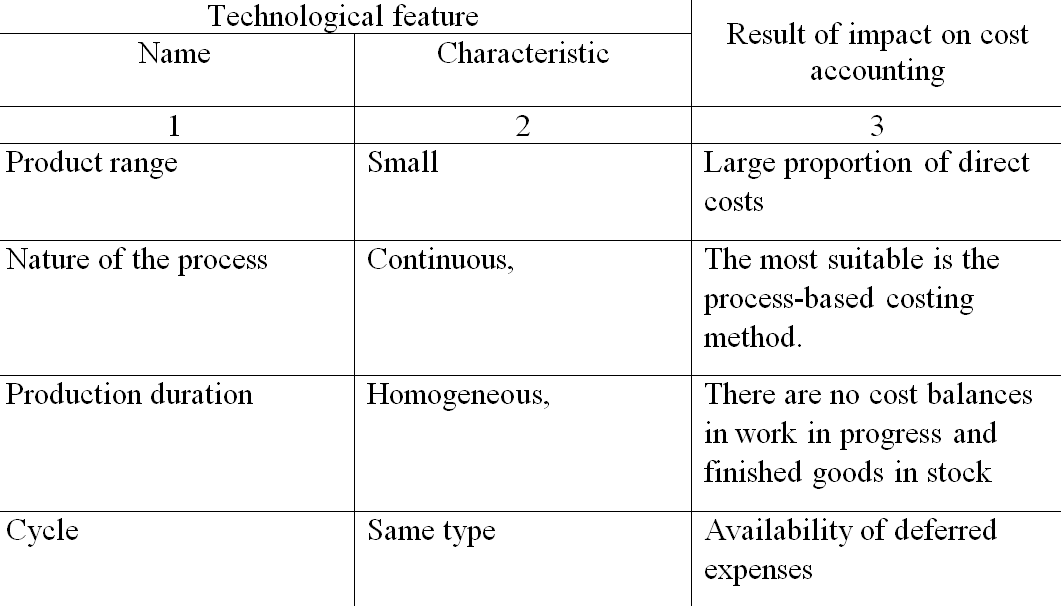

Technological features of thermal energy production can affect the composition of costs and the organization of their accounting. The results of this effect are presented in Fig. 1.

Figure 1 – Results of the influence of technological features of the power system on the organization of cost accounting and costing

In the energy industry, simple and homogeneous products are manufactured, which allows the use of a simple, process-based method of cost accounting and costing.

5. Calculation of the cost of thermal energy and calculation of heat loss at the production stage

Calculation in modern economic literature is defined as a system of economic calculations of the cost of certain types of products (works, services). When calculating the cost of production, a comparison is made of the costs of production with the number of manufactured products and the unit cost of production is determined [11]. The end result of costing is costing. Depending on the purpose of the calculation, a distinction is made between planned, estimated and actual estimates.

A feature of the costing methodology in the energy sector, different from the costing methodology in other industries, is the calculation of the total cost of energy ex-consumer.

The company compiles planned and actual costing of the generated heat energy.

To compile a planned calculation of thermal energy and its transmission, the following preliminary estimates and calculations are used:

a) calculation of specific fuel consumption in boiler rooms;

b) fuel balance;

c) calculation of depreciation deductions;

d) payroll calculation;

e) cost estimates for auxiliary production workshops;

e) cost estimates for maintenance and production management;

g) cost estimates for the preparation and development of production (start-up costs);

h) calculation of the cost of purchased energy;

i) calculation of heat energy losses in heating networks;

k) calculation of the net supply of heat energy.

All technical and economic indicators of the cost plan should be justified by detailed balance sheet calculations to ensure organic alignment with all sections of the planned costs.

Production costs are planned by costing.

For the heat power industry, estimates are made for the following cost groups:

1) material costs, which include: acquisition costs from raw materials; costs of auxiliary materials; water charges; costs of payment for services; fuel costs; purchase energy costs; household repair; contract repair;

2) labor costs;

3) deductions for social needs;

4) depreciation of fixed assets;

5) other costs.

Cost estimates are prepared for the year using forecast prices, tariffs and other valuations.

At the enterprise SPP Donetskgorteploset

the process-based method of costing is used.

The transportation of heat from the heat source to consumers in modern district heating systems is associated with losses of thermal energy, including through thermal insulation of pipelines. In various speeches and publications, the value of heat losses during transportation in existing heat networks is estimated at 15-20% of heat energy supplied from sources. Heat losses are included in the tariffs for thermal energy and are one of the indicators of the energy efficiency of the operation of heating networks, therefore, determining the actual value of these losses is an important practical task.

To assess the performance of any system, including a heat power system, a generalized physical indicator is usually used - the coefficient of performance (COP). The physical meaning of efficiency is the ratio of the amount of useful work (energy) received to the spent. The energy spent, in turn, is the sum of the useful work (energy) received and the losses occurring in the system processes. From this we can conclude that we will achieve an increase in the efficiency of the system (and hence increase its efficiency) only by reducing the amount of unproductive losses that occur during operation. This is the main task of energy conservation.

For the purpose of analysis, we will conventionally divide all heat energy systems into 3 main components:

1. Thermal energy production.

2. Transportation of thermal energy to the consumer.

3. Consumption of thermal energy.

Each of these sections has characteristic unproductive losses, the reduction of which is the main function of energy conservation.

Conclusions

In order to avoid such losses, the following ways to solve the problem of heat loss at the production stage are proposed:

- conduct a comprehensive survey of boiler units. Assess the quality of the peripheral equipment of the boiler room;

- equip the boiler room with working devices for monitoring and regulation;

- restore the thermal insulation of the boiler unit by detecting and eliminating uncontrolled sources of suction air into the furnace.

When writing this essay, the master's work is not yet completed. Final completion: June 2020. Full text of the work and materials on the topic can be obtained from the author or his manager after that date.

The list of sources

- Gavrilenko V.A. Economic analysis of industrial enterprises: Donetsk: DVNZ. DonNTU, 2009. 96 p. – 383 p. – P. 601 – 604.

- Zabrodin I.P. Justification of directions of development of cost accounting and cost calculation in heat power engineering [Electronic resource] / I.P. Zabrodin / / Vestnik VSU: scientific journal. – 2016. – access Mode: http://www.vestnik.vsu.ru/program/view/view.asp?sec=econ&year=2016&num=01&f_name=2016 - 01-20

- Koshkarova A.A. Basic principles of cost accounting and calculating the cost of electricity at thermal power plants / Amirov A.Zh., Popov S.N. / / Young scientist. – 2016. – No. 9.

- Boiler plants and their operation: textbook for the beginning of professional education / B.A. Sokolov. – 6th ed., erased. Moscow: publishing center "Academy", 2011. – 432 PP.

- Zhigunova O.A. Costs, expenses, expenses: interpretation from the position of resources / Kovalev A. S. / / Accounting. 2015. N 1.

- Rgulation (standard) of accounting 16 "Expenses", approved by the order of the Ministry of Finance of Ukraine of 31.12.99 No. 318. [Electronic resource]. – access Mode:http://kodeksy.com.ua/ka/buh/ psbu/16.htm

- Voitolovsky N.V. Economic analysis. Fundamentals of the theory. Complex analysis of the organization's economic activity: a textbook for bachelors / ed. By N.V. Voitolovsky, A.P. Kalinina, I.I. Mazurova.– 4th ed., pererab. and additional – M: yurayt, 2013. – 548 PP.

- Adamova G.A. Method of calculating the cost of production/ Ilchenko A.A. / / Vestnik GUU.2015. No. 4 Pp. 161-164.

- Accounting. Module 2. Fundamentals of accounting financial and management accounting. Version 1.0 [Electronic resource]: electron. studies'. manual / S.A. Samusenko, O.N. Kharchenko, T.V. kozhinova, etc. – Krasnoyarsk: IPK SFU, 2008.– 650 PP.

- Accounting financial accounting: textbook / A.V. Zonova, I.N. Bachurinskaya, S.P. Goryach.// – SPb.: Peter, 2011. – 480 PP.

- Akhmedov A.E. Improving the cost accounting system for production / Shatalov M.A. / / Territory of science. 2015. N 1. Pp. 127– 132.

- Boiler plants and their operation: textbook for the beginning of professional education / B.A. Sokolov. – 6th ed., erased. Moscow: publishing center "Academy", 2011. – 432 PP.

- Accounting: textbook / G.I. Alekseeva, S.R. Bogomolets, I.V. Safonova; edited by S. R. Bogomolets. – 3rd ed., pererab. and additional. – M.: Moscow financial and industrial University "synergy", 2013. – 720 PP.