Economic substantiation of an investment project for the development of a coal mining enterprise

Content

- Introduction

- The essence of investments and investments in the development of the enterprise

- Formation of investment resources of the enterprise

- Economic justification of the effectiveness of investment investments

- conclusions

- List of sources used

Introduction

Relevance of the research topic.

In a market economy, the competitiveness of an enterprise, the possibility of attracting investment, development prospects, and ultimately the possibility of successful operation of the enterprise depend on the assessment of the effectiveness of investment investments.

Investment activity means investing funds in the long term to obtain the maximum effect, i.e. arrived. As a result of investment in enterprises, production volumes grow, income increases, and in connection with these, the cost of this product decreases. The effectiveness of investment investments depends on a comprehensive analysis of both the expected income and the necessary costs for the implementation of a particular investment project. A project can be implemented if it is cost effective, and, conversely, if it is ineffective, then it should be rejected.

The degree of elaboration of the research topic.

Many different interpretations of the content of the term

investment were considered

,

investment investments were

studied by such foreign and domestic scientists as: I.A.

Blank, V.G.

Zolotogorov, I.V.

Sergeev, I.I.

Veretennikova, Z. Bodie, A. Kane, A.J.

Markus and others.

The generalization of scientific publications allows us to

highlight various approaches of scientists to the definition of the concept of

investment

,

investment investment

.

However, the state of investment investments requires further

study, taking into account the specifics of the economic conditions.

Purpose of the study.

Economic justification of technical measures to increase the

production capacity of the OP

Shakhta im.

M.I.

Kalinin

.

Object of study.

Investment activity of the coal mining enterprise OP

Shakhta im.

M.I.

Kalinina

State Enterprise

Makeevugol

)

Subject of study

Theoretical and practical aspects of investing in the development of a coal mining enterprise.

1. The essence of investments and investments in the development of the enterprise

In each market economy of the country, an enterprise needs to increase or confirm its competitiveness, as well as to ensure the stability and stability of functioning in a dynamically changing economic environment, in which various factors of influence (positive and negative) arise. In this regard, for the improvement and development of any enterprise, it is necessary to make investments.

The term

investment

comes from the Latin word

invest

, which means to

invest

,

to clothe

.

The concept of

investment

is widespread, both in domestic and foreign literature.

Many scientists

[1]

have their own point of view on the essence of this category

(Table 1).

Table 1 - Disclosure of the essence of investments by various scientists

| Author's name | The essence of the concept |

| I.A. Blank | Investments - investment of capital in monetary, material and non-material forms in objects of entrepreneurial activity in order to obtain current income or ensure an increase in its value in the long term |

| V.G. Zolotogorov | Investment is an investment of funds (internal and external) in various programs and individual activities (projects) with the aim of organizing new, maintaining and developing existing production facilities (production facilities), technical preparation of production, making a profit and other end results, for example, environmental , social, etc. |

| I.V. Sergeev and I.I. Veretennikova | Investments in a broad sense should be understood as monetary funds, property and intellectual values of the state, individuals, directed to the creation of new enterprises, expansion, reconstruction and technical re-equipment of existing ones, the acquisition of real estate, stocks, bonds and other securities and assets in order to make a profit ( i) or other positive effect |

| M.Yu. Makovetsky | Investments are investments of savings of all participants in the economic system both in objects of entrepreneurial and other types of activity, and in securities and other assets in order to generate income (profit) or achieve a positive (social) effect |

| G.P. Podshivalenko | Investments are a set of costs realized in the form of a targeted investment of capital for a certain period in various sectors and spheres of the economy, in objects of entrepreneurial and other types of activity to generate profit (income) and achieve both individual goals of investors and a positive social effect |

| Z. Bodie, A. Kane and A.J. Marcus | An investment is an expenditure of cash or other funds in anticipation of obtaining future benefits |

| G.V. Savitskaya | Investments - long-term investments in the assets of an enterprise in order to increase profits and build up equity capital |

Having analyzed various approaches to understanding

the essence of the concept of

investment,

we can conclude that, on the one hand, investments

are an investment of funds (capital, savings), and on the other, a set of costs (expenditure of

funds).

In the broadest sense, investments must provide the mechanism that is necessary to finance the growth and development of organizations and any state as a whole. Taking into account the structure of the investment process, its participants and types of investors, investments are understood as real estate, property, machinery, equipment, technology, cash, deposits in banks, securities, property rights, licenses, intellectual values invested as a way of investing capital in entrepreneurial activity in order to preserve or increase them. In other words, investments are a tool with which you can place investments in the investment object and provide a positive amount of income [2] .

As a resource in the very concept of

investment

is money that can be invested in intangible assets, movable

and immovable property, various financial instruments, etc.

The following classification of investments can be distinguished:

- as a way to generate entrepreneurial profit:

- direct investment is an investment in fixed assets of movable and immovable property;

- portfolio investment is an investment in financial instruments for the purpose of obtaining speculative profit as a result of changes in stock quotes;

- other investments (credit for the purpose of obtaining loan interest);

- as an investment object are distinguished:

- investments in tangible assets, that is, investments in fixed assets (land, buildings and structures, machinery and equipment, transport, etc.);

- investments in intangible assets (know-how, property rights, including copyrights, etc.);

- investments in financial instruments (securities);

- investments in human capital (advanced training, additional courses, staff training, etc.);

- as a subject of ownership:

- private;

- state;

- mixed;

- by investment duration:

- short-term (up to 1 year);

- medium-term (from 1 to 3 years);

- long-term (more than 3 years);

- ultra-short-term (from several hours to a couple of days);

- extra long-term (over 30 years);

- in relation to the life cycle:

- initial investment;

- extensive investments (for the expansion of the enterprise);

- reinvestments (investments aimed at developing production at the expense of available funds);

- reverse investments (investments that were withdrawn earlier with the departure of the investor from the activities of the invested object);

- in relation to the balance sheet:

- gross investment - the total volume of investment resources in all their forms, directed in a certain period for the implementation of real and financial investment;

- net investment - the main source of financing the goals of the enterprise aimed at its development, expansion and modernization [3] ;

It is necessary to highlight the following signs of investment:

- making investments by investors to achieve their own benefits, which do not always coincide with the general economic benefit;

- potential ability of investments to generate income;

- availability of investment term (always individual);

- the purposeful nature of capital investment in investment objects and instruments;

- the use of various investment resources, characterized by demand, supply and price, in the process of investment;

- the presence of capital investment risk [4] .

In a modern economy, investment functions are performed at the macro and micro levels.

At the macro level, the following investment functions are distinguished:

- the process of simple and extended reproduction of fixed assets, both in the production and non-production spheres;

- the process of providing and replenishing working capital;

- the flow of capital from one area to another through the sale and purchase of financial assets;

- redistribution of capital between owners by purchasing shares and investing in assets of other enterprises.

On a macroeconomic scale, current wealth is largely the result of yesterday's investments, and today's higher-wealth investments, which in turn lay the foundation for further growth in gross domestic product. Thus, the value of investments cannot be overestimated, since they directly predetermine economic growth [5] .

The functions of investment at the micro level include:

- prevention of excessive moral and physical wear and tear of fixed assets in all branches of activity;

- expansion and development of highly efficient areas of activity;

- increasing the technical level of production, which means reducing the costs of products and services provided;

- improving the quality and competitiveness of products;

- replenishment of working capital [6] .

At the micro level, investments are necessary primarily to achieve the following goals:

- expansion and development of production;

- prevention of excessive moral and physical wear and tear of fixed assets;

- increasing the technical level of production;

- improving the quality and ensuring the competitiveness of the products of a particular enterprise;

- implementation of environmental protection measures;

- purchasing securities and investing in assets of other companies.

Ultimately, investments are necessary to ensure the normal functioning of the enterprise in the future, a stable financial condition and maximize profits.

2. Formation of investment resources of the enterprise.

In modern economic conditions, the most pressing issue for enterprises is the formation of investment resources in order to ensure, in the first place for themselves, high rates of development and competitiveness.

Any enterprise is faced with investment activities that are directly related to the formation of investment resources. The entire economic activity of the enterprise depends on the nature of the formation of investment resources.

Investment resources represent all types of monetary and other assets of the enterprise, the source of which is the investor, which are intended for investment activities [7] .

The main goal of the formation of the investment resources of the enterprise is to meet the needs for the acquisition of the necessary investment assets and to optimize their structure in terms of ensuring effective results of investment activities.

One of the most important tasks of effective management of investment resources of an enterprise is to determine the sources of their formation.

In economic practice, there are many classifications of sources for the formation of investment resources, among which one can single out [8] :

- own financial resources (profit, depreciation charges, compensation for losses after accidents, natural disasters, etc.);

- borrowed financial assets of the investor (bond loans, bank and budget loans);

- attracted financial resources of the investor (funds received from the sale of shares, shares and other contributions of citizens and legal entities);

- budgetary investment appropriations (targeted funding provided free of charge by budgetary authorities);

- gratuitous and charitable contributions, donations from organizations, enterprises, citizens.

Also, among the general classification, investment resources can be divided into internal and external [9] .

Internal investment resources are understood as: profit, depreciation charges, insurance claims, investments of the owners of the enterprise.

External include: budgetary investments; funds of credit institutions and organizations, insurance companies, non-state pension funds of other institutional investors; sale of securities, etc.

According to this classification, internal investment resources are formed directly at the enterprise to ensure its development, and external ones - outside of it.

The effective formation of investment resources for individual sources is the most important condition for the financial stability of an enterprise. In turn, the volumes and sources of formation of investment resources are largely determined by the structure of capital that has developed at the enterprise in the process of its economic activity, as well as the cost of raising capital.

The main features of the process of forming investment resources of an enterprise are presented in Figure 1 [6] .

Figure 1 - The main features of the process of forming the investment resources of the enterprise

The accumulation of initial capital is carried out directly within the enterprise itself through the distribution of net profit.

The basis for the formation of the investment resources of the enterprise is its initial capital intended for reinvestment. The forms of such reinvested capital used in the process of forming investment resources are depreciation charges for fixed assets and depreciable material assets; funds received from the sale of retired capital assets and others.

The stages of the life cycle of an enterprise are

characterized by distinctive features in the rates and sources of formation of investment

resources, from the

implementation

stage

to a

decline

.

At the post-investment stage, investment resources are formed for operational purposes, in particular, for financing circulating assets for commissioned investment objects.

While real or financial investment may be carried out by an enterprise irregularly and differ by significant unevenness, the process of forming investment resources is continuous. To the greatest extent, this continuity is characteristic of their own internal sources of investment resources formation - depreciation deductions and profits directed to production development. However, the continuity of the process of formation of investment resources does not mean the uniformity of the volumes of their formation in time. These volumes can fluctuate significantly over time, depending on the attraction of investment resources from external sources. The determinism of the process of formation of investment resources is characterized by its quantitative definiteness in time, in volume, structure and other parameters. The regulation of this process is determined by a system of specific effective investment management methods that allow achieving and maintaining the specified parameters for the formation of investment resources. The determinability and controllability of the process of forming the investment resources of an enterprise allow it to be carried out on a planned basis. allowing to achieve and maintain the specified parameters for the formation of investment resources. The determinability and controllability of the process of forming the investment resources of an enterprise allow it to be carried out on a planned basis. allowing to achieve and maintain the specified parameters for the formation of investment resources. The determinability and controllability of the process of forming the investment resources of an enterprise allow it to be carried out on a planned basis.

The formation of investment resources is inextricably linked with the goals and directions of the investment policy of the enterprise. As the financial basis for the implementation of the selected investment policy of the enterprise, the formation of investment resources is allocated, as a rule, into an independent target block, according to which certain target standards are developed. In some cases, the possibility of forming investment resources by an enterprise determine the pace of its strategic development [4] .

The process of formation of investment resources of a functioning enterprise at the expense of profit (accumulation of new own investment capital) is carried out through the mechanisms of dividend policy (the policy of distribution of newly created profit). The level of profit capitalization, determined by the time preference for its consumption, is formed at each enterprise individually, taking into account the specifics of its investment activities and the conditions of the external investment environment.

The rational structure of the sources of the formed investment resources allows to reduce the level of investment risks in the forthcoming activities of the enterprise, to prevent the threat of its bankruptcy.

The possibility of forming investment resources of an enterprise is largely determined by the capital structure achieved at the previous stage of its business cycle. First of all, this refers to the formation of additional investment resources at the expense of borrowed sources. There is an inverse relationship between the share of the borrowed capital actually used by the enterprise and the possible volumes of its additional attraction for investment purposes. This feature should be taken into account when predicting the potential and rate of formation of investment resources.

The volumes and sources of formation of investment resources are largely determined by the cost of attracting them (the cost of capital). In this case, the weighted average cost of the formed investment capital must be compared with the size of the effect from its use in the process of real or financial investment.

An important source of attracted investment resources are contributions from domestic and foreign investors, which are subdivided into direct and portfolio investments. Direct investment is an operation that provides for the contribution of funds or property to the statutory fund of a legal entity, in amounts that, in accordance with the law, provide the right to control its activities.

Portfolio investment - a transaction that involves the purchase of securities, derivatives (derivative financial instruments) and other financial assets or investment in enterprises without the right to control their activities.

The most important problem of an investor in the process of forming investment resources is to determine their total volume. The total amount of investment resources of the enterprise should be determined based on the planned volume of the development of funds in the implementation of individual real investment projects, as well as the planned increase in the portfolio of financial investments [3] , [6] .

So, characterizing the practice of forming investment resources of an enterprise, it should be noted that a significant part of the capital is generated by the enterprise itself at the expense of profit and depreciation deductions, the rest comes from the issue of securities for specific investment programs and projects, attracting resources from investment funds, insurance companies, commercial banks, non-standard methods of financing investment activities. When determining the optimal structure of the formation of investment sources, the requirements of the solvency and financial stability of the enterprise should be taken into account.

Thus, the formation of the optimal structure of investment resources will provide a single comprehensive impact on the investment activities of domestic business entities and will allow them to significantly increase their investment attractiveness and financial stability.

3. Economic justification of the effectiveness of investment investments

In the conditions of a modern market economy, the issue of the urgent problem of economic assessment of the effectiveness of investment investments arising in the process of forming and implementing project management remains unresolved.

To increase the investment attractiveness of an industrial enterprise and the high-quality structure of capital investments, it is necessary to improve approaches to assessing the effectiveness of investments [6] , [7] .

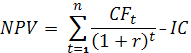

Currently, there are many methods for evaluating the effectiveness of investment projects, which are based on the use of various economic indicators, such as net present value (NPV), profitability index (PI), payback period (tok), internal rate of return (IRR), and etc. They are used by specialists - analysts of investment processes. A few of them are usually enough for investors to make an investment decision.

When calculating net present value, current (base) prices and a constant discount rate should be used. Under these conditions, net present value (NPV) is determined by the formula:

,(1)

,(1)

where NPV is net present value;

CFt - cash flow during time t;

IC - investment capital, representing the investor's costs in the initial period;

r - discount rate.

In order to calculate NPV, it is necessary to predict the future cash flows for the investment project, determine the discount rate and calculate the total value of the income reduced to the current moment.

NPV is one of the most common criteria for evaluating investment projects. Estimated NPV values are given in table. 2.

Table 2 - Estimation of NPV value

| Estimating NPV value | Making decisions |

| NPV≤0 | This investment project does not cover future costs or only provides a break-even point and should be rejected from further consideration |

| NPV> 0 | The project is attractive for investment and requires further analysis |

| NPV1>NPV2 | The investment project (1) is more attractive in terms of the present value than the second project (2) |

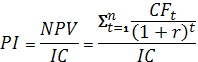

The profitability index reflects the efficiency of an investment project.

The return on investment index can be calculated as follows:

, (2)

, (2)

where PI is the profitability index of the investment project;

NPV - net present value;

n is the implementation period (in years, months);

r - discount rate (%);

CF - cash flow;

IC is the initial investment capital spent.

The main difficulty in calculating the profitability index is to estimate the size of future cash receipts and the discount rate (discount rate).

The stability of future cash flows is influenced by many macro- and microeconomic factors: the seasonality of supply and demand, interest rates of the Central Bank, the cost of raw materials and materials, sales, etc. The indicator of the profitability index indicates the efficiency of using capital in an investment project. Table 3 below shows the assessment of the investment project depending on the value of the indicator.

Table 3 - Assessment of the investment project depending on the value of the indicator

| Indicator value | Investment project appraisal |

| PI<1 | The investment project is excluded from further consideration |

| PI = 1 | The income of the investment project is equal to the costs, the project does not bring any profit or loss. It needs modification |

| PI>1 | The investment project is accepted for further investment analysis |

| PI1> PI2 | The level of capital management efficiency in the first project is higher than in the second. The first project has great investment attractiveness |

The profitability index itself, like any other indicator, has a number of advantages and disadvantages [10] , [11] , [12] , [13] .

The advantages of the yield index are as follows:

- the possibility of comparative analysis of investment projects of different scale;

- using the discount rate to take into account various difficult-to-form project risk factors.

The disadvantages of the profitability index include:

- forecasting future cash flows in an investment project;

- the difficulty of accurately estimating the discount rate for various projects;

- the complexity of assessing the impact of intangible factors on the future cash flows of the project.

The payback period (PP) is the minimum period of time for the return on investment in an investment project, business or any other investment. The payback period is a key indicator for assessing the investment attractiveness of a business plan, project and any other investment object.

PP is calculated by the formula:

, (3)

, (3)

where IC is the initial investment cost in the project;

CFi is the cash flow from the project in the i-th time period, which is the sum of net

profit and depreciation.

To calculate the cash flow, you must use the following formulas:

,(4)

,(4)

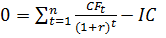

Internal rate of return (IRR, internal rate of return, internal rate, internal rate of return, internal discount rate, internal rate of return, internal rate of return) is a coefficient showing the maximum allowable risk for an investment project or the minimum acceptable level of return.

The internal rate of return is equal to the discount rate at which there is no net present value, that is, equal to zero.

,(5)

,(5)

where: CFt - cash flow in the time period t;

IC (InvestCapital) - investment costs of the project in the initial period (also cash flow

CF0 = IC).

t is a period of time.

The indicator is used to assess the attractiveness of an investment project or for comparative analysis with other projects. To do this, IRR is compared with the effective discount rate, that is, with the required level of profitability of the project (r). For this level, in practice, the weighted average cost of capital ( WACC ) is often used . The application of the internal rate of return is presented in table. 4.

Table 4 - Applications of the internal rate of return

| IRR value | Comments |

| IRR>WACC | The investment project has an internal rate of return higher than the cost of equity and debt capital. This draft should be accepted for further analysis. |

| IRR<WACC | The investment project has a rate of return lower than the cost of capital, this indicates the inexpediency of investing in it |

| IRR = WACC | The internal rate of return of the project is equal to the cost of capital, the project is at the minimum acceptable level and cash flow adjustments should be made and cash flows increased |

| IRR1>IRR2 | Investment project (1) has a higher investment potential than (2) |

It should be noted that instead of the WACC comparison criterion, there can be any other barrier level of investment costs, which can be calculated using the methods of estimating the discount rate.

Internal rate of return (IRR) is closely related to net present value (NPV). The change in net present value depends on the internal rate of return [13] .

Today, according to the above methodological recommendations, the main indicator of the effectiveness and attractiveness of an investment project is considered to be the net discounted income.

conclusions

The term

investment is of

Latin origin and means to

invest

.

From this we can conclude that investments in themselves

mean an investment of funds or a set of costs to achieve a certain result, that is,

obtaining a positive effect (profit).

The classification of investments is very diverse, ranging from the method of obtaining entrepreneurial profit to the relation to the balance sheet. But despite this, investments have certain signs (money investments do not always coincide with the general economic benefit in order to bring income within a predetermined period, since there is a risk of the investment itself under the influence of demand, supply and price in the process of making investments)

The main goal of the formation of the investment resources of the enterprise is to meet the needs for the acquisition of the necessary investment assets and to optimize their structure in terms of ensuring effective results of investment activities.

In order to effectively form investment resources, it is necessary to adhere to a certain condition, namely the financial stability of the enterprise.

Investment attractiveness can be increased by improving the approaches to assessing the effectiveness of investments.

Various economic indicators (net present value (NPV), profitability index (PI), payback period (PP), internal rate of return (IRR), etc.) are necessary in order to make the right investment decision. The main indicator of the efficiency and attractiveness of an investment project is considered to be the net present value.

List of sources

-

Аврашков, Л.Я. Инновационно-инвестиционная деятельность предприятий: научная монография / Л.Я. Аврашков. Г.Ф. Графова, А.В.,Графов С.А.. Шахватова– М. – 2015 г.

-

Алпацкая, Е. Г., Инвестиционная деятельность: институциональный аспект / Е. Г.Алпацкая // Вестник Челябинского государственного университета. – 2010. – № 14. С. 82-87.

-

Ангелко, І.В. Основні джерела формування інвестиційних ресурсів підприємства в умовах його розвитку / І.В. Ангелко // Молодий вчений. – 2015. – № 2 (17). – С. 893-897.

-

Баєва, О.І. Інструменти залучення інвестиційних ресурсів / О.І. Баєва // БИЗНЕС ИНФОРМ. – 2009. – № 11(1). – С. 5-7.

-

Балабанов В. С., Основные понятия и сущность инвестиционной деятельности предприятия / В. С. Балабанов , Е. В. Дмитриева // Мир: Развитие. – 2012. – С.103-107.

- Бланк, И.А. Инвестиционный менеджмент / И.А. Бланк // : Учебный курс. – 2-е изд., перераб. И доп. – к.: Эльга, Ника-Центр. – 2006 . – 552 с.

-

Брауде, А. Инвестиционный проект: управление мотивацией / А. Брауде, О. Ефименко , И. Леонова // Управление компанией. – Москва.– 2005. – С.25-28.

-

Бухонова, С.М. Теоретико-методические аспекты оценки потребности предприятия в инвестиционных ресурсах / С.М. Бухонова, Ю.А. Дорошенко // Экономический анализ: теория и практика. – 2007. – № 10. – С. 11-16.

-

Воробьева, И. М. Роль инвестиций в экономике / И. М. Воробьева, А. М. Пономарев. // Молодой ученый. – 2015. – №10. – С. 572-574.

-

Графов А. В. Оценка эффективности инвестиций в инновации в предпринимательской деятельности / А. В. Графов, Л. Я. Аврашков, Г.Ф Графова // Серия: Экономика. – 2016. – С.378-388.

-

Земцов, А.В Оценка эффективности инвестиционного проекта / А. В. Земцов // Методический журнал: Банковское кредитование. – Москва. – 2008. –№6. – С. 45-51.

-

Мирзабекова, М.Ю Оценка эффективности инвестиционного проекта / М.Ю. Мирзабекова // Международный Научный журнал

Инновационная наука

. – Владиковказ. – 2016. – №1. – С. 140-145. -

Окладников, Д. Оценка эффективности инвестиций. Выбор оптимальных подходов к принятию инвестиционных решений / Д. Окладников // Управленческий учет и финансы – 2012г. - №4.