Abstract

Contents

- Introduction

- 1. Theme urgency

- 2. Goal and tasks of the research

- 3. Research and development overview

- 4. Nature and structure of fixed assets

- Conclusion

- References

Introduction

Fixed assets form the basis of the material and technical base of production. The final results of the company's work depend on their perfection and reliability. Their value at industrial enterprises is estimated in tens and hundreds of millions of rubles. However, not all fixed assets at many enterprises are fully used and are in good condition. Part of the fixed assets of enterprises is inactive. As part of this technique, a huge amount of metal is deadened, which is not moving for a long time, causing an additional need for it. Maintenance and maintenance of such equipment in working condition involves the cost of both labor and material resources. The unreasonableness and lack of timely replacement of equipment leads not only to an increase in production costs, but also to significant distractions of funds from turnover, which also puts the company in a very difficult financial condition.

1. Theme urgency

The relevance of this topic is that fixed assets play a huge role in the labor process, since they together form the production and technical base and determine the production capacity of the enterprise. In this regard, the correct formation and rational use of fixed assets is of great importance for the sustainable and efficient operation of the enterprise and requires constant study of them.

2. Goal and tasks of the research

The purpose of the master's thesis is to study the organization of accounting and state audit of fixed assets, identify shortcomings and contradictions in the accounting of fixed assets in the enterprise and develop recommendations for their improvement.

To achieve this goal, the following tasks were set and completed:

- Determine the theoretical basis of accounting and auditing of fixed assets of the enterprise;

- Consider the organization of accounting for fixed assets of the enterprise;

- Investigate the mechanisms of state audit of fixed assets.

Research object: accounting and state audit of the investigated enterprise in the conditions of the Mine

Research subject: a set of theoretical, methodological and organizational provisions for accounting for fixed assets in industrial enterprises.

The paper considers the theoretical aspects of fixed assets, namely: the essence and classification of fixed assets; legal regulation of accounting for fixed assets. The structure of fixed assets, the organization of primary, analytical and synthetic accounting of fixed assets in the conditions of the enterprise under study is disclosed. Shortcomings and contradictions in the organization of accounting and audit of fixed assets are revealed and recommendations for its improvement are developed.

3. Research and development overview

For a long time, foreign scientists such as K. Marx [1], as well as well-known domestic scientists such as V. A. Gavrilenko [2], L. A. Leonova [3], V. V. Verbitskaya [4], L. Lovinskaya [5], F. F. Butinets [6], and others were engaged in improving the accounting of fixed assets. However, despite all efforts in this direction, it was not possible to solve this problem completely.

4. Nature and structure of fixed assets

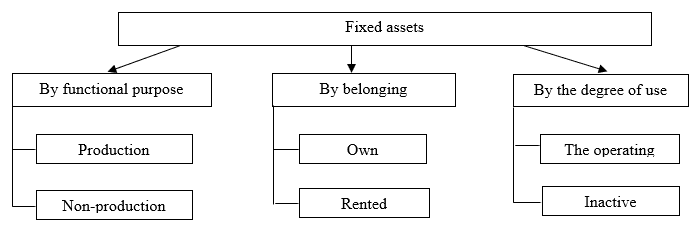

To ensure timely and correct accounting of fixed assets and control over their safety and use at the enterprise, an economically justified classification of fixed assets should be developed. In our opinion, it is advisable to distinguish the following classification group of fixed assets from the entire set of classification features for accounting purposes and effective management of fixed assets in the enterprise (Fig. 1).

Figure 1 – Classification of fixed assets

Fixed assets are defined as means of labor for production and non-production purposes that participate in the production process for many cycles while maintaining their basic properties and original shape.

The main production funds are those fixed assets that take part in the production process, directly at the mine under study. these include buildings and structures, machinery and equipment, vehicles, tools, appliances and inventory.

Fixed assets for non-production purposes are assets that are not involved in the production process. They are designed to serve the cultural and domestic needs of employees. This includes administrative buildings, cultural and household items, canteens, as well as other buildings, structures, and other items that are not intended for industrial use.

The following groups and subgroups of fixed assets are distinguished [7]:

- Buildings (construction objects for industrial purposes: shop buildings, warehouses, superstructure buildings).

- Structures (engineering and construction objects that create conditions for the production process: tunnels, structures for lifting machines, loading bins, etc.).

- Transfer devices (devices for transmitting electricity, liquid and gaseous substances: power grids, heating networks, gas networks, transmissions, etc.).

- Machines and equipment (power machines and equipment, working machines and equipment, measuring and control instruments and devices, computing equipment, valves, lifter trolleys, winches, various outdoor equipment; containers, etc.).

- Vehicles (locomotives, wagons, cars, trucks, pile drivers, elevators, trolley, etc., in addition to pipelines and transporters to be included in the production equipment).

- Tools (cutting, impact, pressing, sealing, as well as various devices for fixing, mounting, etc)

- Industrial equipment and supplies (items to facilitate the implementation of production operations: work tables, workbenches, fences, fans, containers, racks, etc.).

- Household equipment (items of office and household welfare: tables, cabinets, hangers, typewriters, safes, etc.).

- Other fixed assets (composition of this group include library collections, Museum treasures, etc.).

Depending on the degree of direct impact on the objects of labor and production capacity of the enterprise, the main production assets are divided into active and passive. The active part of fixed assets includes machinery and equipment, vehicles, and tools. The passive part of fixed assets includes all other groups of fixed assets.The efficiency of production and enterprise operations as a whole is impossible without an effective accounting structure for fixed assets. The structure of the accounting object relative to fixed assets in the conditions of the OP mine named after A. A. Skochinsky is shown in Fig. 2.

Figure 2 – Structure of the object of accounting for fixed assets

(animation: 17 frames, 5 cycles of repeating, 392 kilobytes)

5. Status of the fixed asset problem

An important condition for the functioning of a business entity is the availability of fixed assets. This requires constant monitoring of the efficiency of the use of fixed assets for the needs of production management. One of the main tasks of accounting for fixed assets is to provide complete, truthful and unbiased information about them. However, the information contained in the financial statements regarding fixed assets is not always such due to the imperfection of domestic legislation and constant changes in it, so fixed assets require research and improvement.

You can identify the following shortcomings in the accounting of fixed assets, such as the compilation of registers of fixed assets.

The information basis of all accounting, analytical and control procedures is accounting information, so the primary task of improving the organization of accounting is to form the composition and determine the content of indicators.

Documentation of operations on the movement of fixed assets, accounting registration and reporting should be organized as a systematic sequence of logically interrelated operations of the accounting process, subordinate to the needs of management, while ensuring the unity of approaches in the formation of indicators, documents, accounting registers and reporting forms.

Analysis of the structure of documents and registers for accounting for fixed assets introduced by regulatory documents showed that, on the one hand, they contain outdated indicators, do not form final, generalizing information, and on the other – they do not contain the indicators necessary for reporting under the conditions of application of ПСБУ 7 Fixed assets

, so the media for accounting for fixed assets requires improvement in both composition and content.

To improve the mechanism of operation of the enterprise through the document flow regarding the movement of fixed assets, namely [7]:

– Act of acceptance and transfer (internal movement) of fixed assets;

– Certificate of acceptance and delivery of repaired, reconstructed and modernized objects;

– The act of writing off fixed assets and accounting registers (inventory card).

Identified a problem that can be solved by deleting the columns that marked the book value, the code of the depreciation rate, the depreciation rate for full restoration and major repairs, the start date of payment for fixed assets, the correction factor, and add the following: the cost of fixed assets, providing for the ability to specify all possible types of estimates (initial, liquidation, revalued, fair) group of fixed assets, useful life (operation) depreciation method used for each object; source of capital investment with its own interpretation (own funds, target financing, contributions to the authorized capital, etc.) indicators that characterize the revaluation (revaluation, markdown) of both the original cost of fixed assets and their depreciation. Removing unnecessary indicators will reduce the amount of unnecessary work of the accounting apparatus and allow you to focus on effective information that directly affects management decisions about the availability of fixed assets and their use, that is, it will increase the efficiency of accounting[9].

The organization of accounting for the movement of fixed assets, starting with their commissioning, acceptance after repairs and ending with their liquidation, should be built taking into account their specific features, ensuring simultaneous control and analytical procedures. For high-quality, responsible performance of works on acceptance and write-off of objects, it is advisable to develop a working instruction that clearly defines the list of works and the procedure for their implementation, the functions and tasks of each member of the Commission, as well as their responsibility.

Thus, the theoretical and practical foundations of the organization of fixed assets accounting should be improved in the direction of expanding its management capabilities, as much as possible adapting to the practical needs of business entities that arise in the process of making management decisions on the movement of fixed assets and the effectiveness of their use. The main ways to improve the organization of fixed assets accounting is to rationalize both each form of documents and accounting registers, and methods and methods of collecting, processing and summarizing accounting information adapted to modern conditions.

Conclusion

Accounting for fixed assets plays a huge role in the labor process, they together form the production and technical base and determine the production capacity of the enterprise. Over a long period of use, fixed assets are transferred to the enterprise and put into operation, wear out as a result of operation, undergo repairs that restore their physical qualities, move inside the enterprise and leave the enterprise due to dilapidation or impracticability of further use.

Master's work is devoted to actual scientific problem of combining the basic methods of minimizing the instrumental Moore automata. In the trials carried out:

– improvement of the enterprise operation mechanism through document management;

– involve specialists in complex repairs;

– increase the level of specialization of production;

– upgrade equipment;

– improve the composition, structure and condition of the company's fixed assets;

– improve the quality of repairs.

Practical application of proposed measures in the whole enterprise will allow to increase volumes of output and increase profit from sales and the profitability of fixed assets of an organization.

When writing this paper, the master's thesis is not yet completed. Final completion: may 2021. The full text of the work and materials on the topic can be obtained from the author or his supervisor after the specified date.

References

- К., Маркс Капитал / К., Маркс. – М.: Политиздат, 1960. – 900 с.

- В. А., Гавриленко Економічний аналіз діяльності промислових підприємств / В. А., Гавриленко. – Д.: ДВУЗ, ДонНТУ, 2009. – 353 с

- В. А., Гавриленко, Л.А., Леонова Особенности реформирования учета операций с основными средствами и его влияния на собственный капитал / В. А., Гавриленко, Л. А., Леонова. – Д.: ГОУВПО ДонНТУ, 2017. – № 4/8.

- Л. В., Вербицька Теорія бухгалтерського обліку: навч. – метод. посібник / Л. В., Вербицька – К.: Логос, 2003. – 420 с.

- Л., Ловинская, А., Белоусова Учет налоговых разниц в системе регистров журнальной формы. – 2004. – № 4. – С. 7–25.

- Ф. Ф., Бутинець,Н. В., Шатило Податковий облік в Україні: навчальний посібник для студентів спеціальності 7.050106 Облік і аудит. – Житомир: ЖІТІ, 1998. – 928 с.

- Положение (стандарт) бухгалтерского учета 7

Основные средства

от 28.05.1997 № 392/3685 (с изменениями и дополнениями от 09.12.2011). [Электронный ресурс]. Электрон. дан. – Режим доступа: http://zakon2.rada.gov.ua/laws/show/z0288-00 - М. Н., Толчинская, Контроллинг качества аудита в современных условиях / Э. Н., Гаврилова // Научное обозрение. Серия 1: Экономика и право.– 2015. – № 3. С. 207–210.

- А. В., Коваленко, Направления повышения эффективности использования основных фондов предприятия / А. В., Коваленко, И. В., Громова // Экономический вестник Запорожской государственной инженерной академии. – 2014. – № 7. – С. 20–27.