Formal description and modeling of facial expressions of emotions

Content

- Introduction

- 1. PROBLEM STATEMENT

- 1.1 Relevance of the topic

- 1.2 Purpose and Objectives of the Study, Expected Results

- 2. REVIEW OF RESEARCH AND DEVELOPMENT

- 3. STATUS OF THE COMMITMENT PROBLEM

- Output

- References

Introduction

The most important prerequisite for sustainable business development in the long term is to increase its competitiveness. Competitiveness consists of two main factors – the ability to attract capital on favorable terms and the ability to effectively use the resources available to the organization. State control can become one of the most effective tools for identifying opportunities to improve the efficiency of activities and, consequently, one of the competitive advantages of an organization.

The process of economic development is inextricably linked with information support for the activities of business entities, the most important component of which is accounting data and the results of its control, providing information about the financial condition of the enterprise to interested parties, in order to use them for making managerial decisions.

In the process of economic activity of enterprises, their economic relationships with other market entities, including individuals, counterparties, state and tax authorities, which cause the emergence of obligations, are activated. As a source of formation and financing of assets, liabilities play an important role in the financial and economic activities of an economic entity. Significantly affecting financial stability and solvency, obligations, given their dynamic nature, require effective cash flow management, control of the actual state of settlements, especially during a difficult financial situation and financial crisis. Such control becomes possible on the basis of reliable, high-quality and adequate information about debt, which is formed in the accounting system and timely and effective control of this information by the state control and audit services.

1. PROBLEM STATEMENT

1.1 Relevance of the topic

The relevance of the topic is due to the problem of managing economic stability, which has become particularly acute in modern economic conditions, which is very important for capital-intensive sectors of the national economy, which include enterprises of the coal mining complex.

Such enterprises operate under the influence of a high level of depreciation of fixed assets, frequent changes in tax legislation, low labor productivity, difficult mining and geological conditions, spontaneous changes in the mineral raw materials markets, undocumented price increases for equipment and materials, and a complex geopolitical situation.

Such enterprises operate under the influence of a high level of depreciation of fixed assets, frequent changes in tax legislation, low labor productivity, difficult mining and geological conditions, spontaneous changes in the mineral raw materials markets, undocumented price increases for equipment and materials, and a complex geopolitical situation.

A significant component characterizing the financial condition of an enterprise is information about obligations, their structure and dynamics. This information is used by experts when assessing the solvency and financial stability of an economic entity.

1.2 Purpose and Objectives of the Study, Expected Results

The purpose of this master's thesis is to study and generalize theoretical, methodological, methodological and organizational provisions, as well as to develop scientific and practical recommendations for improving the control and audit of obligations in accordance with modern management requirements, their impact on the sustainable development of the enterprise and the state as a whole.

To achieve this goal , the following tasks are defined:

- to investigate the economic essence of obligations and determine their place and role as an object of accounting, control and audit;

- determine the criteria for classifying obligations in order to ensure the rational formation and full use of information for making effective management decisions;

- to substantiate methodological approaches to the recognition and evaluation of obligations, to develop proposals for their improvement taking into account domestic and foreign experience;

- evaluate the current procedure for reflecting liabilities in the accounting and financial reporting registers and provide suggestions for its improvement, which would ensure accurate and complete information about the state of liabilities at the enterprise as a whole and by their types in particular;

- To develop recommendations for improving state control and audit of obligations of the of the Shakhty of A.A. Skochinsky.

Subject of research: state control and audit of obligations as an element of sustainable development of the enterprise on coal mining.

Object of research: financial and economic activity of the branch of the A.A. Skochinsky Mine of the State Coal Mining Enterprise Donetsk Coal and Energy Company.

2. REVIEW OF RESEARCH AND DEVELOPMENT

In order to develop and deepen the theoretical and organizational and methodological foundations of the problems under consideration, the accumulated foreign experience can be useful, but its use is possible only taking into account the prevailing features of state control of commercial organizations in the specific conditions of the DPR and Russia.

A scientific review of the works of foreign specialists investigating various theoretical and organizational and methodological aspects of the foundations of the system of state control and audit is presented by the works of: E.A. Ahrens, R. McConnell, Emerson, K. Drury, J. K. Lobbeck, R. Montgomery, M.B. Hirsch, etc. The review was carried out within the framework of the study of the processes of state control of settlements of an enterprise with other market entities that characterize the state and movement of obligations and their reflection in the accounting system.

The works of many Russian scientists are devoted to the study of the essence, content, approaches to assessment, methods and tools for managing the economic stability of enterprises, among which it is necessary to highlight the works of O.M. Belotserkovsky [1], A.A. Aroshidze, V.M. Vasiltseva, P.S. Tsvetkov [2, 3], E.V. Korchagina, T.A. Pikalova [4], Baranova V.E. [5], Fedoseeva S.V., Romanova A. I., and other scientists.

Various techniques and methods are used to study the state of economic stability. Thus, in the works of a team of authors led by O.M. Belotserkovsky, the effectiveness of the application of nonlinear dynamics methods in the study of modern economic processes at the regional level is shown. The authors consider the theories of an effective sustainable market with nonlinear processes of the economic model of the region. The possibility of using the theory of catastrophes and the theory of deterministic chaos in solving some socio-economic problems is being studied [6].

The problems of management of mining enterprises based on measuring and evaluating the effectiveness of their activities in market conditions are considered in the research of T.A. Pikalova.. In the articles on the direction of research related to the sustainable development of mining enterprises, the factors that determine the need to implement the principles of corporate sustainability in the activities of a mining company are formulated. The interrelation of the company's operational activities and the principles of corporate sustainable development is revealed [4].

Baranov V.E. summarizing and comparing existing approaches to the interpretation of the concept of "economic stability of an enterprise", comes to the conclusion that it is necessary to observe the point of view of scientists who consider economic stability as an ability (property, characteristic) of an enterprise, the level of which can be assessed by analyzing indicators of the dynamics of the state and structure of the enterprise [5].

The central link of any work devoted to the problem of economic sustainability is its assessment. Research by Tsvetkov P.S. allowed us to identify several of the most popular approaches to assessing economic sustainability:

- the use of an integral indicator, presented as a geometric mean, composed of partial indicators reflecting stability;

- application of the method of coefficients consisting in their multiplication. The advantages and disadvantages of the first two methods are practically the same;

- calculation of the integral stability indicator by the weighted average sum of criteria [2].

The influence of the structure of obligations on the corporate management system is studied in the works of Ivashkevich A.V., Gudkov E.A., Bashkatov N.F., Druzhinovskaya T.Yu., Dubkov V.A., Nesterov I.N., etc. Their work is based on the task of identifying the most effective mechanisms for assessing the value of an enterprise from the standpoint of fulfilling various obligations. At the same time, all scientists agree that there is no single universal methodology in the field of finance. Thus, in practice, accounting methods of accounting and evaluation of financial resources are most often used and regulated. The issues of reflecting accounting information on borrowed capital on financial accounting accounts are considered in the works of E.V. Kleschina, E.Yu. Dirkova, R.R. Akhmetishina, V.V. Shcherbatyuk, etc. and the movement of muscles is approximate.

Druzhilovskaya T.Y. and Igonina T.V. [7] proposed a classification of types of liabilities, which is shown in Figure 2.1.

Figure 2.1 – Classification of types of liabilities (animation: 8 frames, 3 repetition cycles, 47.9 kilobytes)

Shcherbatyuk V.V. in the article "Recognition. Assessment and accounting of long-term and current liabilities" provides economic characteristics and classification of liabilities of Moldovan market structures, national peculiarities of accounting of long-term and current liabilities in accordance with new regulations developed on the basis of International Financial Reporting Standards are considered in detail [8].

Such domestic researchers as L.S. Braginskaya, D.V. Kukelko, S.V. Shkodinsky, T.P. Hrebtova, E.O. Basangova, M.V. Melnik and others made a significant contribution to solving the problems of the theory of the organization of state control and audit.

In particular, Fokina O.N. [9], having analyzed the methodological foundations of accounting, analysis and control of obligations, came to the conclusion that enterprises have an unsatisfactory or formalized analytical base regarding the movement of obligations, the expediency of their involvement, riskiness and effectiveness.

The issues of accounting for accounts receivable and accounts payable under IFRS today are among the most relevant for both Russian and foreign business entities in the process of accounting. One of the main unresolved problems of the present time is the fact that IFRS does not provide for a special standard that would regulate a certain procedure for accounting for receivables and payables [10].

Analyzing the Russian accounting standards for accounts receivable and accounts payable, we can say that the main feature of IFRS, in comparison with Russian legislation, is the fact that IFRS 39 does not establish an inventory obligation. And in Russia, during the annual inventory of calculations, the reliability and validity of accounts receivable and accounts payable of the enterprise is checked and debts with expired statute of limitations are identified [11].

3.STATUS OF THE COMMITMENT PROBLEM

A number of works by domestic and foreign authors are devoted to the question of the essence of the concept of "obligation", the problems of their reflection on accounting accounts: Gulina V.A., Kozlova M.O., Kolomiets N., Lapteva D., Maidanik R, Nikolenko L., Malyugi N.M., Ometsinskaya I.Ya., Petruk A.N., Pyatova M.L., Rilnik I.L., Sokolova Ya.V., Soldatkina A.A., etc. However, some theoretical provisions regarding the interpretation of current obligations are debatable. In this regard, there is a need to clarify and further improve the theoretical and methodological aspects of recognition, classification, documentation, evaluation and reflection of obligations and their state control and audit.

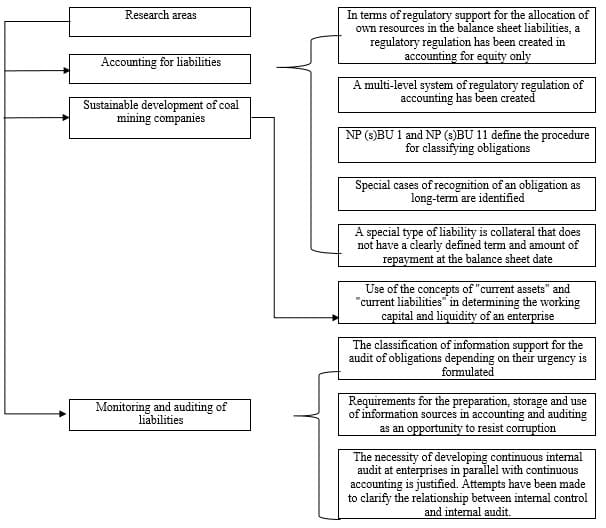

The first question that an enterprise may have is the allocation of borrowed and own resources in the balance sheet liabilities. If regulatory regulation in accounting provides such an opportunity in relation to equity, then determining the amount and structure of borrowed capital requires additional research.

The domestic regulatory framework has certain gaps in the reflection of medium-term loans. If the legislation regulating banking activity assumes the allocation of loans to a separate group, the maturity of which is from 1 to 3 years, then the National P(S)BU does not support the corresponding classification.

Attention should be paid to contradictions in the definitions of national accounting standards, in particular in the assessment of unforeseen liabilities. So, in P(S)The BU states that the amount of unforeseen liabilities is determined by the accounting estimate of the resources required for repayment at a certain reporting date, but, guided by this document, the amount of the contingent liability cannot be reliably determined. The same situation is observed in the assessment of collateral, and this can already significantly affect the financial results of the enterprise, since the amounts of collateral created are recognized as expenses of the reporting period.

The definition of current assets and current liabilities has traditionally been considered useful information to help users of financial reports analyze the financial condition of an enterprise. Some believe that the classification of assets and liabilities into "current" and "non-current" should give an approximate definition of the liquidity of the enterprise, that is, its ability to carry out daily activities without financial difficulties. Others consider this classification as providing a definition of those resources and obligations of the enterprise that are in constant circulation.

Such points of view are to some extent incompatible. The criterion for determining assets and liabilities as current is whether they will be consumed or repaid to provide income during the normal operating cycle of the enterprise. The operating cycle of an enterprise, as a rule, is called the average time interval between the acquisition of materials for production and the final sale of products for cash. For example, construction in progress will be excluded from current assets according to the first criterion, while according to the second criterion it will be included in current assets.

Such conflicting points of view have led to the adoption in many countries of a provision on how items are included in current assets, based on whether they are expected to be realized within one year or during the normal operating cycle of the enterprise, depending on which period of time is longer; items are included in current liabilities, if they are paid at the request of the creditor or are expected to be repaid within one year. Even if this approach is applied as a general rule, there are cases of inclusion or exclusion of individual articles in accordance with different criteria. Thus, the classification of articles into current and long-term in practice is based mainly on contracts, and not on any one concept.

Figure 3.1 shows the existing solutions to the identified problems of accounting for liabilities.

Figure 3.1 – Existing solutions to the problem of accounting for liabilities

Output

Based on the results of the work, we can say that all the main goals and objectives were fulfilled.

The economic essence of obligations is investigated and their place and role as an object of accounting, control and audit are determined. The criteria for classifying obligations are defined in order to ensure the rational formation and full use of information for making effective management decisions. Methodological approaches to the recognition and evaluation of obligations are substantiated, proposals for their improvement are developed taking into account domestic and foreign experience. The current procedure for reflecting liabilities in the accounting and financial reporting registers was evaluated and proposals for its improvement were presented. Recommendations have been developed to improve the state control and audit of the obligations of the Shakhty of A.A. Skochinsky

References

- Белоцерковский, О.М. Экономическая синергетика: Вопросы устойчивости / О.М. Белоцерковский, Г.П. Быстрай, В.Р. Цибульский. – Новосибирск, 2006. – 116 с. – ISBN 5-02-031101-4.

- Цветков П.С. Оценка экономической устойчивости горнорудных предприятий на основе динамического подхода / Цветков П.С.// Дис. ... канд. экон. наук. – СПб, 2015

- Цветков П.С. Проблемы оценки экономической устойчивости горнодобывающих предприятий // Известия Санкт-Петербургского государственного экономического университета. - СПб, 2014. - № 5 (89). - с. 132- 136.

- Пикалова Т.А. Алгоритм целевого управления операционной деятельностью горнодобывающей компании в контексте устойчивого развития / Т. А. Пикалова // Горный информационно-аналитический бюллетень (научно-технический журнал). – 2014. – № 2. – С. 380-386.

- Баранова В.Е. Экономическая устойчивость предприятия / В.Е. Баранова, Е.Ф. Николаева // Academy. – 2018. – № 10(37). – С. 18-24.

- Гудкова Е.А. Совершенствование экономической сущности и классификации обязательств / Е.А. Гудкова // Вестник Белорусской государственной сельскохозяйственной академии. – 2021. – № 2. – С. 22-27.

- Дружиловская Т.Ю. Особенности практики учета обязательств и их влияние на показатели деятельности организаций / Т.Ю. Дружиловская, Т.В. Игонина // Бухгалтерский учет в бюджетных и некоммерческих организациях. – 2015. – № 6(366). – С. 2-10.

- Danescua T., Prozanb M., Prozanc R.D. // The Valances of the Internal Audit in Relationship with the Internal Control – Corporate Governance, 2015. – Р. 960-966. Режим доступа: https://www.researchgate.net/publication/283236819_The_Valances_of_the_Internal_Audit_in_Relationship_with_the_Internal_Control_-_Corporate_Governance

- Щербатюк В.В. Признание, оценка и учет долгосрочных и текущих обязательств / В.В. Щербатюк // Статистика, учет и аудит. – 2015. – № 4(59). – С. 66-75.

- Горбулин В.Д., Фокина, О.Н. Дебиторская и кредиторская задолженность. Особенности бухгалтерского и налогового учета: учеб.пособие. / Горбулин В.Д., Фокина О.Н. - М.: ГроссМедиаФерлаг, 2018. - 127 с.

- Клещина Е.В. Современные подходы к учету дебиторской и кредиторской задолженности согласно российскому законодательству и МСФО / Е.В. Клещина // Форум молодых ученых. – 2020. – № 4(44). – С. 145-152.

- Башкатова Н.Ф. Гармонизация учета финансовых обязательств по российским и международным стандартам в судостроении / Н.Ф. Башкатова, С.А. Полухина // Вестник Самарского государственного экономического университета. – 2019. – № 11(181). – С. 62-70.