Abstract

Сontents

- Introduction

- 1. Relevance of the topic

- 2. Theoretical foundations of accounting for tax calculations

- 3. Organization of accounting and audit of tax calculations in the conditions of Sunflower Group LLC

- 4. Analysis of tax accounting and development of recommendations for its improvement

- Conclusion

- References

Introduction

Tax is a mandatory, regular, individual gratuitous payment, the payer of which is an individual or organization, in the form of transfer of funds belonging to them on the basis of ownership, economic management or operational management, in order to financially support the activities of the state or municipalities.

The economic content of taxes is to withdraw certain shares of the national income from business entities, citizens, who are disposed of by the state for the implementation of its functions and tasks. The totality of types of taxes, forms and methods of their construction, tax authorities form the tax system of the state.

Purpose of the study - identification of contradictions and shortcomings in the organization of accounting for tax calculations at the enterprise and development of recommendations for its improvement.

Research objectives:

- To reveal the essence and content of tax calculations as an accounting object.

- Analyze the legal framework for tax accounting.

- To reveal the problems of accounting for objects of tax settlements and give recommendations for improving their accounting.

- Demonstrate the organization of primary, analytical and synthetic accounting of tax payments in the conditions of Sunflower Group LLC.

- To reveal the stages of the audit of tax calculations.

- To study the features of labor protection, life safety and civil defense in the enterprise.

In preparing this thesis, various textbooks on accounting for tax payments, literature containing a description and characteristics of tax systems in various countries of the world, articles of an economic nature that consider problems of taxation and possible ways to improve accounting and audit of taxes and payments, and statistical data were used. , showing the differences between certain indicators.

The methodological basis for the completion of the thesis was the legislative and regulatory framework on the subject of research, as well as the work of scientists and practitioners in this area.

1. Relevance of the topic

The relevance of the thesis is that the tax system is one of the most important economic regulators, the basis of the financial and credit mechanism of state regulation of the economy. The effective functioning of the entire national economy depends on how well the taxation system is built.

The problems of the formation and functioning of an effective state tax policy are of particular relevance in the conditions of an unstable socio-political situation in the Donetsk People's Republic, which is being actively discussed at various levels.

The theoretical and methodological basis of the study was the scientific works of leading experts in the field of taxation, accounting, finance, such as: Smith A., Ricardo D., Astakhova V.P., Babaeva Yu.A., Panskov V.G. and others, as well as regulations and data on current accounting, accounting and statistical reporting of the enterprise. The main sources used in writing the thesis are scientific, methodological and educational literature on taxes and taxation, economic theory and macroeconomics. However, despite numerous studies on tax policy, such issues as improving the efficiency of tax control, simplifying tax legislation, searching for and selecting professional personnel in the tax system of the state are not fully disclosed. The above determined the relevance, choice of topic, its purpose and objectives.

The novelty of the work lies in the development of recommendations for eliminating contradictions, eliminating shortcomings in accounting for taxes and payments and ways to implement them at the enterprise.

2. Theoretical foundations of accounting for tax calculations

Tax calculations as an object of accounting are the obligations of an enterprise that arise for this enterprise as a payer of certain types of taxes in accordance with the current tax legislation.

Tax calculations are classified as current liabilities (obligations for settlements with the budget) and are reflected in the balance sheet by the amount of repayment, accounting is regulated by P (S) BU 11 «Liabilities». Restructured tax liabilities are classified as long-term liabilities, depending on their maturity.

According to NP (C) BU 11 «Liabilities are the debt of an enterprise that arose as a result of past events and the repayment of which in the future is expected to lead to a decrease in the resources of the enterprise that embody economic benefits[1]. Obligations for settlements with the budget arise on the basis of declarations that are filled in for each type of tax by the enterprise.

In accordance with the Law on the tax system of the Donetsk People's Republic, a tax is a mandatory, individually gratuitous payment levied to the relevant budget from taxpayers in the form of alienation of their property, economic management or operational management of funds in order to financially support the activities of the Donetsk People's Republic [2].

From an economic point of view, taxes are instruments of fiscal policy and, at the same time, a method of indirect regulation of economic processes at the macro level.

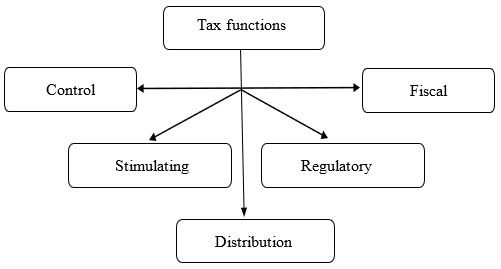

The essence of taxes are their functions. The group of basic functions includes the essential function of the tax (fiscal) and two general financial functions (regulatory and control). It is on the basis of these functions that the tax mechanism is built, and, acting together, they constitute an integral complex.

Additional functions detail the main goals implemented through the subsystem of the main functions. In addition, if the main functions are mandatory for all types of taxes, then additional ones have a tinge of optionality and are not necessarily presented in all available types of tax.[3].

Taxes and their functions reflect the real basis, that is, the objective laws of the movement of tax relations, which are used by the state in tax policy (pic. 1)

Picture 1 – Tax functions

The most important function of taxes is fiscal. In all states, in all social formations, taxes primarily performed a fiscal function. In accordance with this function, taxes fulfill their main purpose - to saturate the revenue side of the budget, state revenues to meet the needs of society.

The regulatory function serves as a kind of complement to the previous one and affects both the regulation of production and the regulation of consumption (for example, indirect taxes). At the same time, the regulatory mechanism exists objectively and the influence on payers is carried out regardless of the will of the state. This function plays an important role, without which it is impossible to do without in an economy based on commodity-money relations. It is impossible to imagine an effectively functioning market economy that is not regulated by the state.

The control function is implemented in the course of taxation when the state regulates the financial and economic activities of enterprises and organizations, the receipt of income by citizens, the use of property by them. With the help of this function, the rationality and balance of the tax system, each lever separately, is assessed, it is checked how taxes correspond to the realization of the goal in the current conditions. In principle, through the implementation of the control function, it becomes possible to quantify tax revenues and compare them with the state's needs for financial resources.

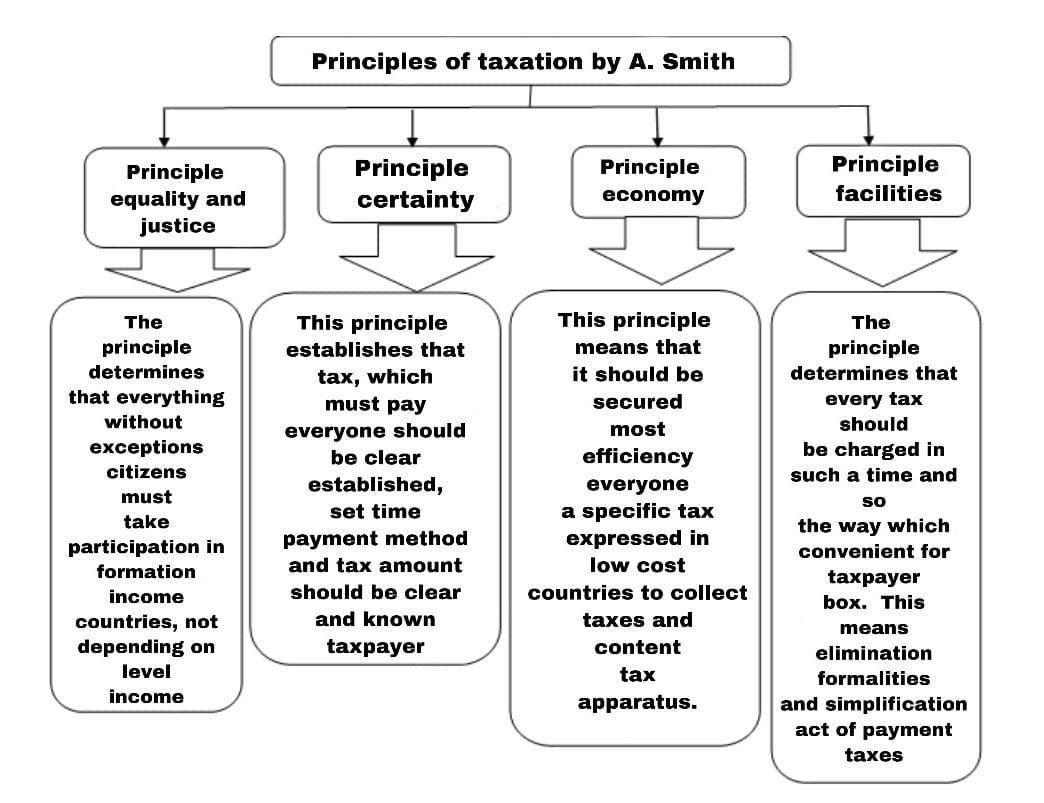

Speaking about the principles of taxation, we can say that the state needs to fully meet the needs, on the basis of which it establishes a set of taxes that will be withdrawn according to uniform laws and principles. For the first time, these principles were expressed by Adam Smith, who in his work «An Inquiry into the Nature and Causes of the Wealth of Nations» writes about the four main principles of taxation (pic. 2).

Picture 2 – A. Smith's principles of taxation

Thus, the essence of taxes is expressed in its functions and principles. And on the part of the state, the essence of taxes is connected with the fact that for the state regulation of socio-economic processes, the financial and budgetary mechanism and its component - taxes - are used as a means of interaction.

The English economist A. Smith, based on the factors of production (land, labor, capital), supplemented the income of the landowner with income from capital and labor and, accordingly, two direct taxes - on the entrepreneurial profit of the capital owner and on the wages of an employee. A. Smith considered indirect taxes to be taxes that are associated with expenses and are passed on to the consumer[5].

For more than a hundred years, it has been known to distinguish taxes into two subsystems:

- Direct taxes - those that are directly related to the result of economic and financial activities, capital turnover, an increase in the value of property, an increase in the rental component.

- Indirect taxes - those that are a surcharge on the price or are determined depending on the amount of value added, turnover or sales of goods, works, services.

The tax system has its own legal regulation, but, as in every tax system of the country, there are drawbacks and problems. The problems of the formation and functioning of an effective state tax policy are of particular relevance in the context of an unstable socio-political situation in the Donetsk People's Republic. In the current state of instability, the imperfection of the tax system and the instability of the economy, it is important to establish a strong structure of tax collections, which will ensure the future development of a strong as well as competitive state.

List of regulatory and legal support for accounting for taxes and payments: Law of the DPR «On Accounting», Law of the DPR «On the Tax System», P (S) BU No. 11 Obligations, P (S) BU No. 16 Expenses, P (S) BU No. 17 Income tax.

After analyzing the regulatory framework of the Donetsk People's Republic, it is possible to single out the main legal acts that regulate the activities of the revenue and fees bodies of the DPR:

- Constitution of the Donetsk People's Republic.

- Temporary Regulations on the Ministry of Revenue and Fees.

- Law of the Donetsk People's Republic «On the tax system».

- Decrees of the People's Council of the Donetsk People's Republic, Decrees and Orders of the Head of the Donetsk People's Republic, Decrees and Orders of the Council of Ministers of the Donetsk People's Republic.

- Orders of the Ministry of Income and Fees of the Donetsk People's Republic.

- Normative-legal acts adopted by local governments.

Deferred tax liability is the amount of income tax that will be paid in the following periods from temporary tax differences that are taxable.

A deferred tax asset is the amount of income tax that is recoverable in the following periods as a result of:

- Temporary tax difference deductible.

- Transfer of tax loss not included in the calculation of income tax reduction in the reporting period.

- Transfer to future periods of tax benefits that cannot be used in the reporting period.

Tax difference is the difference arising between the assessment and recognition criteria of income, expenses, assets, liabilities in accordance with P(S)BU and income and expenses determined by tax legislation. This means that the same items of income and expenses can have different values in accounting and tax accounting, the difference between the values is called the tax difference.

Permanent tax difference is a tax difference that arises in the reporting period and is not canceled in the following reporting tax periods. This means that the difference will always be present; when calculating deferred tax liabilities (IT) and deferred tax assets (ITA), this difference is not taken into account.

Temporary tax difference - a tax difference that arises in the reporting period and is canceled in the next tax reporting periods; the same income and expenses are taken into account in accounting and tax accounting, but for a different period or in different periods. The temporary tax difference serves as the basis for determining IT and ITA[6].

Accounting profit (loss), which is calculated as the difference between the accounting income and expenses of the enterprise before tax, is called accounting profit (loss). The amount of accounting profit (loss) is reflected in the form No. 2 of the financial statements "Statement of financial results" in line 2290 (profit) or 2295 (loss).

According to N (C) BU No. 1 “General requirements for financial reporting”, profit is the amount by which income exceeds the costs associated with them. Loss - the excess of the amount of expenses over the amount of income for which these expenses were made. Income is an increase in economic benefits in the form of an inflow of assets or a decrease in liabilities that lead to an increase in equity. Expenses - a decrease in economic benefits in the form of disposal of assets or an increase in liabilities, which, on the contrary, lead to a decrease in equity.

From an accounting point of view, according to P (S) BU No. 15 “Income”, income is recognized when an increase in an asset or a decrease in a liability that causes an increase in equity, provided that the estimate of income can be reliably determined[7].

According to P (S) BU No. 16 "Expenses", the expenses of the reporting period are either a decrease in assets or an increase in liabilities, which leads to a decrease in the equity capital of the enterprise, provided that these expenses can be reliably estimated [8].

Income and expenses calculated according to accounting data in many cases do not coincide with income and expenses calculated in accordance with the provisions of tax legislation, which often causes difficulties in the process of accounting for income tax calculations.

Methodology for determining deferred taxes - deferred tax liabilities (IT) and deferred tax assets (ITA) on the example of income and expense items that have different meanings in tax and accounting. The process is to:

- Write out all these items of income and expenses in accounting and tax accounting.

- Actually calculate the difference.

Temporary tax differences are the differences between the carrying amount (BC) of an asset or liability and its tax base (NT). The algorithm for determining the amount of deferred taxes in Table. 1.

| Name of temporary difference | The change | IT (gr. 2 x tax rate) | ITA(gr. 2 x tax rate) |

|---|---|---|---|

| Active balance sheet items | BS - NB = "+", BS>NB | + | |

BS - NB = "-", BS| |

+ |

| |

| Passive balance sheet items | BS - NB = "+", BS>NB | + | |

BS - NB = "-", BS| + |

|

|

3. Organization of accounting and audit of tax calculations in the conditions of Sunflower Group LLC

Sunflower Group LLC independently organizes the tax accounting system, fixing its position in the accounting policy for tax purposes, approved by the head of the enterprise. The accounting policy of Sunflower Group LLC was developed on the basis of the requirements for accounting: completeness, reliability, timeliness, prudence, priority of content over form, consistency, rationality.

Each transaction carried out at the enterprise, as a payer of income tax, is documented. Primary documents confirming a business transaction and affecting the declaration and payment of income tax are stamped.

The documents confirming the transaction, based on the agreement concluded between the parties, are:

- Commodity, consignment note (commodity-transport, consignment note).

- Act of work performed (services performed).

- Cargo customs declaration for the import and export of goods issued in accordance with the requirements of customs legislation.

- Bank statement of payment.

- A check, a settlement receipt issued by business entities of the Donetsk People's Republic.

- Incoming and outgoing cash orders.

- Other settlement documents established by the accounting rules and not contradicting the requirements of the current legislation.

Depreciation of fixed assets is calculated using the straight-line method, according to which the annual amount of depreciation is determined by dividing the cost that is depreciated by the useful life of the item of property, plant and equipment.

Gross expenses arise at the time of debiting funds from the current account or issuing from the cash desk of the enterprise, and forms the enterprise. Income and expenses are recognized on the basis of primary documents, which confirm the receipt of income and expenses, the obligation to maintain and store which is provided for by the accounting rules of the Law of the Donetsk People's Republic «On the tax system». Also, separate subdivisions fill out tax declarations, guided by the Procedure for filling out and submitting, approved by order of the Ministry of Revenue and Duties of the DPR.

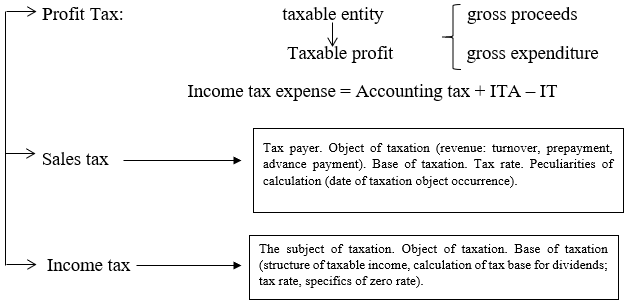

LLC «Sunflower Group», as a taxpayer, pays such types of payments to the budget as: income tax, turnover tax, income tax.

Structural representation of tax calculations is shown in pic. 3.

Picture 3 – Structural representation of tax calculations paid to Sunflower Group LLC

The object of taxation for income tax is net profit, calculated as the difference between gross income and gross expenses of the taxpayer for the reporting period.

The base of taxation is the monetary value of the object of taxation. The basic (basic) tax rate is 20%.

The base of taxation for the turnover tax is the value expression of the object of taxation. The object of taxation is revenue - turnover, prepayments, advances received by a business entity in the reporting period. The rate to be paid is 1.5% of the object of taxation.

The object of income taxation is: total monthly (annual) taxable income (with a source of origin both in the DPR and abroad), income of individuals, in the form of wages.

The total monthly taxable income of a taxpayer includes: income in the form of wages; amounts of remuneration and other payments; income from the sale of objects of property and non-property rights; income from the provision of property for leasing, rent; income in the form of a penalty (fines, penalties), compensation for material or non-property (moral) damage.

The tax base is the total taxable income.

Payment of taxes and fees is made within 10 days after the deadline for filing tax returns. Income tax return is submitted no later than the 20th day of the month following the reporting one; for income tax no later than the 15th; VAT returns must be submitted on a monthly basis no later than the 20th day of the month following the reporting month.

Payment of taxes is carried out by non-cash payment at the branch of the bank of the Central Republican Bank of the DPR. When paying taxes, the following entry is made in accounting:

- Dt 641 «Tax Calculations» (indicating the corresponding sub-account).

- Kt 311 «Bank accounts in national currency».

All business transactions in Sunflower Group LLC are carried out with the execution of primary documents established by the Law of the Donetsk People's Republic, adopted by the Decree of the People's Council, on the basis of which accounting is maintained.

The methodological basis for the formation in accounting of information on expenses, income, assets and liabilities for income tax is determined by P (S) BU 17 «Income Tax»[9].

Primary documents for income tax accounting:

- To calculate the gross income of the VD: cumulative tables or statements of gross income for the current month (the list of gross income is given in the Law of the DPR «On the tax system»).

- To calculate the gross expenditures of BP: accumulative tables or statements of gross expenditures for the current month (the list of gross expenditures is given in the Law of the DPR «On the tax system»).

- To reflect the current income tax (TN): Declaration of income tax.

- Cumulative tables (statements) for deferred tax assets (ITA), deferred tax liabilities (ITL).

- Accounting certificate (calculation) of the amount of expenses for income tax (RP).

According to P(S)BU 17, income tax is divided into current and deferred.

Income tax expense (income) in accordance with P(S)BU No. 17 «Income Tax» is the total amount of income tax expense (income), which consists of current income tax, taking into account the deferred liability and deferred tax asset.

Income tax expenses (income) are calculated according to the following formula:

Income tax expense (Rp) = Current income tax (Tn) + Deferred tax liabilities for the period (ΔIT) - Deferred tax assets for the period (ΔITA)

Current income tax (TN) is the amount of declared income tax according to tax accounting. The object of taxation of income tax (according to tax accounting) is profit, which is calculated by reducing the amount of gross income of the reporting period by the amount of gross expenses of the reporting period, taking into account the rules established by the Law of the DPR «On the tax system»:

Current income tax (TN) = Gross income (TD) - Gross expenses (VR)

Gross income (turnover) - the total amount of the taxpayer's income from all types of activities received (accrued) in the reporting period, both on the territory of the DPR and outside it, determined on the basis of primary documents that confirm the receipt of such income by the taxpayer.

Gross expenses - the amount of expenses of the taxpayer incurred (accrued) in the reporting period on the basis of primary and other documents confirming the expenses incurred by the taxpayer related to the conduct of economic activities.

The primary documents for accounting for income include: a bank statement, a bill of lading, an invoice, a sales contract, an invoice, an inventory act, claim documents, a revaluation sheet.

The primary documents for accounting for expenses include: LZK, invoice for the release of materials, signal requirements, acts for the write-off of materials, time sheets, reports, orders, payroll sheet, depreciation sheet, acts of work performed, services rendered, invoices for writing off fixed assets, advance reports, an act on write-offs of the IBE.

Accrued income and expenses are written off to the financial result of the enterprise using an accounting statement. Also, the accounting statement is the primary document when reflecting the accrued income tax amounts and when writing off income tax expenses to financial results.

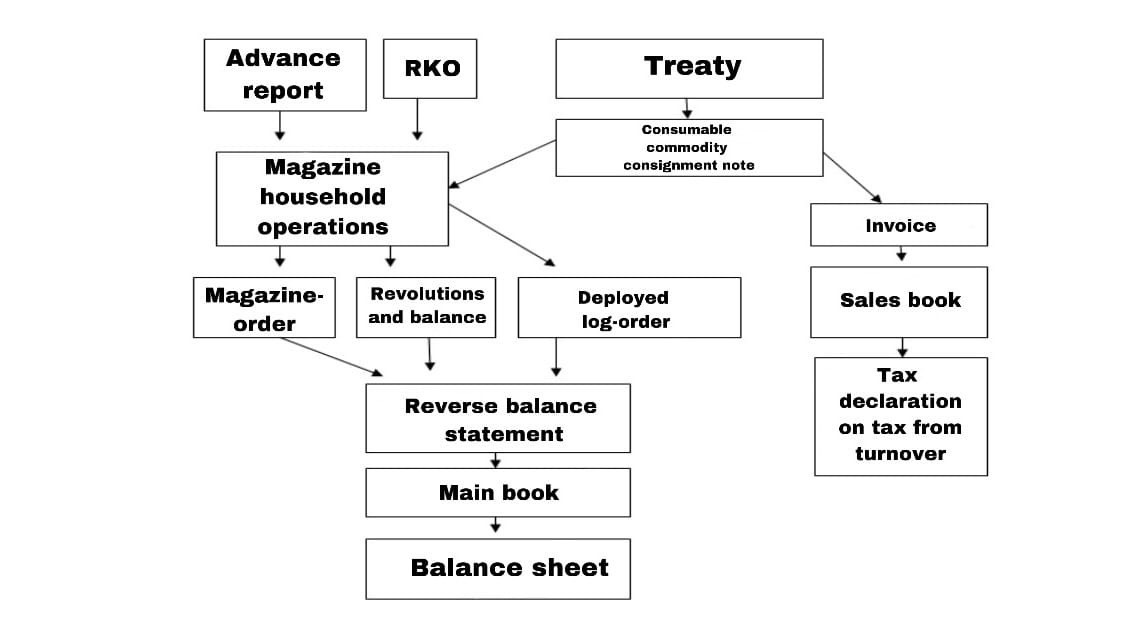

Value added tax is paid to the budget on the basis of the value added tax declaration. Declarations are submitted by the 20th day of the month following the reporting month. The tax is paid within 10 days after the deadline for filing the declaration.

The date of occurrence of the object of taxation with turnover tax is determined according to the «first event» rule, i.e. within the reporting period, the date of the earlier event. When carrying out operations with give-and-take raw materials, the taxable turnover is determined by the date of transfer of the finished product to the customer[10].

The volume of sales of goods, works, services in the reporting period is determined by the date of transfer of ownership to the buyer on the basis of primary documents: contracts, commodity (expenditure) waybill, certificate of completion, cargo customs declaration, etc.

Documents for VAT deduction:

- Journals of orders for the sale of products.

- Invoices, acts of work performed, services.

In more detail, the turnover tax document flow is shown in pic. 4.

Picture 4 – Turnover tax paperwork

Income tax is levied on the salary of all employees, regardless of whether they work under employment contracts, contracts and agreements of a civil law nature, etc. The amount of tax is calculated as follows:

Tax amount = Tax rate (13%) * Tax base.

Tax reporting on tax includes: tax return on income tax, which is compiled on paper, in electronic form. The data for calculating the tax is taken from the payroll sheet, on the basis of which the journal order is filled.

To calculate labor costs, calculate income tax and deductions for social needs, a payroll sheet is used. This statement reflects data on accruals (basic, additional salary fund, incentive and compensation payments) and deductions (advance payment, social security contributions, income tax, union dues, alimony) for the whole month for the organization. This statement is filled out on the basis of the data of the employee's payroll or time sheet.

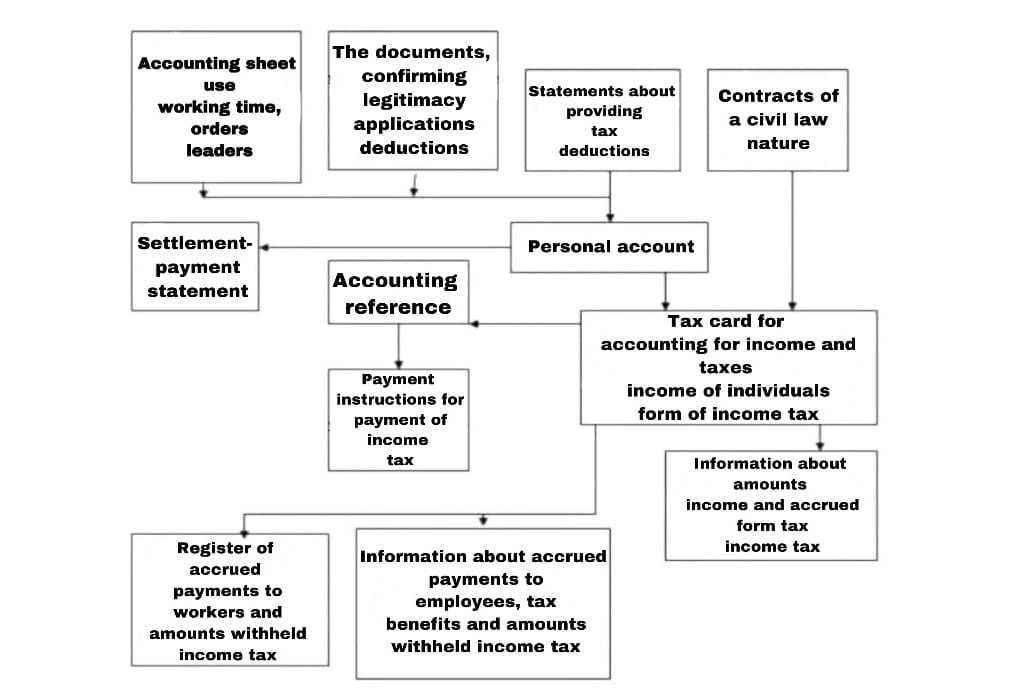

The time sheet is a document that contains information about the hours actually worked and the number of absences per month for each employee of the organization. On its basis, the calculation and calculation of wages. In the event that the time sheet is maintained manually, the standard form T-12 is used, if the control of attendance and absence is carried out automatically (turnstile) - the form T-13 is used. The time sheet is kept every working day for a month, on the last day of the month the total number of hours worked and absences by each employee is summed up. This document is compiled in one copy and transferred to the accounting department. The document is signed by the person responsible for filling out the timesheet, the head of the structural unit, the employee of the personnel department or the director of the company. The income tax document flow is shown in pic. 5.

Picture 5 – Income tax paperwork

Synthetic accounting is maintained on synthetic accounting accounts in accordance with the Chart of Accounts. To summarize information about the enterprise's settlements for all types of payments to the budget, account 64 «Calculations for taxes and payments» is used. The account is characterized as passive, on credit - accrual of payments to the budget, on debit - their payment, write-off, and taxes that are subject to reimbursement from the budget are also reflected. The credit balance is reflected in the fourth section of the liability. The debit balance is reflected in a separate line in the second section of the asset.

Account 64 «Calculations on taxes and payments» has 4 sub-accounts. For each type of taxes and fees, according to the chart of accounts, the necessary sub-accounts are opened:

- Sub-account 641 «Tax Calculations» keeps records of taxes that are accrued and paid in accordance with the current legislation (income tax, value added tax, and others).

- On a subaccount 642 «Calculations on mandatory payments» keeps records of settlements on fees (mandatory payments) that are charged in accordance with applicable law and which are not recorded on account 65 «Calculations for insurance».

- On a subaccount 643 «Tax liabilities» records the amount of value added tax, determined on the basis of the amount of advances received (prepayment) for finished products, goods, other tangible assets and intangible assets, works, services to be shipped. On subaccount 644 «Tax credit», accounting for the amount of value added tax for which the company has acquired the right to reduce the tax liability [11].

Accounting for income tax calculations is carried out on subaccount 641/ «Calculations for income tax». The credit of this sub-account reflects the tax liability calculated on the basis of tax accounting for income tax payable for the reporting period. That is, on the credit of sub-account 641 / «Calculations on income tax», the enterprise shows the amount of income tax declared in the Declaration on income tax, reduced by the amount of advance payments on income tax.

In accordance with the current Chart of Accounts and the Instructions for its Application, synthetic accounting of tax payments for LLC Sunflower Group is kept on account 64 «Calculations for taxes and payments». The credit turnover on this account shows the accrual of the company's debt to the budget for taxes, and the debit turnover shows the budget debt to the company.

Accounting is kept by types of taxes and various payments to the budget. Thus, a sub-account has been opened for account 64 at Sunflower Group LLC: 641/1 «Calculations for income tax».

The data of synthetic and analytical accounting of taxes on account 64 «Calculations on taxes and payments» are summarized and maintained in turnover sheets, which are tables containing information on initial balances, turnovers (debit, credit) for the reporting period, and final balances. Namely, the balance sheet, where the balances and turnovers from the turnover sheet for analytical accounts are recorded. The results of the turnover sheet for analytical accounts are reconciled with the totals and balances for all sub-accounts included in the turnover balance sheet, the final balance for account 64 is transferred to the General Ledger. The result of each turnover sheet of analytical accounting must correspond to similar indicators of the corresponding synthetic account.

For synthetic accounting of tax calculations, order journals are used. Journal-order - a checklist, built in a chess form, allowing one entry to record the operation on two accounts - debited and credited.

Entries in order journals are made on the basis of data from verified and properly executed primary documents or reports of financially responsible persons, bank statements, etc. On the documents recorded in the order journals, the following is indicated: the date of the entry, the number of the order journal, the number of the line in the journal on which the entry was made. Order journals are built on a credit basis, i.e. registration of credit turnover for each balance sheet account is carried out in correspondence with debited accounts. The order journals reflect all transactions related to the credit of a particular account in correspondence with the debit of the corresponding accounts[12].

To account for taxes and payments, order journals No. 3 (calculations for taxes, their accrual), No. 5 (expenses for determining income tax), No. 6 (income for determining income tax) are used.

Summing up, we can single out a mandatory condition for synthetic accounting. Synthetic accounting for account 64 is kept in the balance sheet, where the balances and turnovers from the turnover sheet for analytical accounts are recorded. The results of the statement on analytical accounts are compared with the results of the corresponding synthetic account - they must be equal. Synthetic accounting of settlements with the budget is kept in the journal-order, and analytical (by type of tax) - on cards.

4. Analysis of tax accounting and development of recommendations for its improvement

The analysis of taxation begins with the study of the information-spatial tax field. The information-spatial tax field is formed by a set of relations in the field of calculation, payment, collection and distribution of mandatory payments.

At the enterprise, factors may arise that affect the state of tax settlements, which do not depend on the staff. For example, an increase in the overall tax burden. The risks of an increase in the tax burden are associated with the upcoming changes in tax legislation in terms of increasing tax rates, the emergence of new mandatory payments to the budget and the abolition of benefits, i.e. these risks arise under the influence of external factors.

Recommendations for reducing the tax burden of Sunflower Group LLC

To reduce the tax burden, you can transfer to a special tax regime. Payment of a simplified tax exempts the payer from paying: income tax; turnover tax.

The easiest way to optimize taxes is to properly manage costs. The law provides for the possibility of reducing taxable income by the amount of costs incurred to ensure the functioning of a business entity. The higher the cost, the lower the tax. For example, to reduce income tax, you can artificially increase gross expenses by including expenses for paying for services that were not actually provided, including expenses for market research conducted by third parties, etc.

A rationally drawn up accounting policy has a good effect on the taxation of an enterprise. So, for example, the following elements of accounting policy affect the amount of expenses, and hence the amount of profit:

- Methods for calculating depreciation of fixed assets and intangible assets.

- Methods for assessing raw materials and materials when they are written off to production, as well as the cost of goods when they are sold.

- The procedure for assessing the balance of work in progress, the balance of finished products.

It is also recommended that all amounts of financial assistance to employees and the amounts of remuneration and other payments made to members of the board of directors be attributed to expenses that are not taken into account for tax purposes.

It is important that the company pays taxes correctly and on time. Timely payment of taxes and avoidance of penalties from the fiscal authorities also optimizes the tax burden on the enterprise.

Decrease in gross income due to VAT amounts

The Law of the Donetsk People's Republic «On the tax system» establishes that when determining gross income for taxation by income tax, «gross income does not include the amount of turnover tax».

So, for income tax, the income of the reporting period includes the performance of all income-generating operations, regardless of their payment.

For the turnover tax, the income of the reporting period includes the performance of all income-generating operations, regardless of their payment + prepayments received in this period.

Simplified, this can be represented as follows:

For income tax:

Income = Sales

For VAT:

Income = Sales + Prepayments

Sales subject to income tax will necessarily be subject to value added tax. And this means that in any case, all income for income tax will be subject to VAT. VAT will inevitably be charged and paid on all sales.

Consequently, if turnover tax amounts are not included in income for income tax of the reporting period, then these «non-included» amounts are related exclusively to the base (income) that is subject to income tax of this period, that is, to sales.

And since prepayments are not included in income for income tax, such income cannot be reduced by the amount of tax on prepayments. (Since you can not reduce what is not).

Therefore, we can reduce income for income tax only by the amount of value added tax on the same income.

Income = Sales - Sales tax on this sales

An example of calculating turnover tax amounts that reduce gross income from income tax: in March, an enterprise sold goods in the amount of 10,000,000 rubles. rub. They were also provided with services, according to the acts of work performed, in the amount of 200,000 rubles. rub. In the same month, an advance payment was received for the future delivery of goods in the amount of 100,000 rubles. rub. Calculate the amount of turnover tax and gross income for income tax.

For VAT:

Income = sales (10,000,000 + 200,000) +100,000 (prepayment)

Income for VAT = 10,300,000 ros. rub.

Turnover tax = 10,300,000 * 1.5 = 154,500 dew. rub.

For income tax:

Income = sales (10,000,000 + 200,000) - VAT on this operation.

Income for income tax = 10,200,000 - (10,200,000 * 1.5%) = 10,200,000-153,000 = 10,047,000 ros. rub.

The amount of turnover tax by which income was reduced = 153,000 grew. rub.

In April, goods were shipped on account of an advance payment for 100,000 rubles. rub. and rendered services in the amount of 300,000 rubles. rub.

For VAT:

Income = sales (300,000) + prepayment (0)

Income for sales tax = 300,000 roubles. rub.

Turnover tax = 300,000 * 1.5 = 4,500 dews. rub.

For income tax:

Income = sales (100,000 + 300,000) - VAT on this operation

Income for income tax = 400,000 - (400,000 * 1.5%) = 400,000 - 6,000 = 394,000 ros. rub.

The amount of turnover tax by which income was reduced = 6,000 grew. rub.

And after two months:

The amount of declared and paid turnover tax = 159,000 rubles. R.

The amount of turnover tax by which we reduced income = 159,000 rubles. R.

An analysis of the development of tax control revealed such significant shortcomings as the lack of a systematic approach, as well as ignoring the impact of the economic conditions of the region, which limits the possibility of a comprehensive assessment of the effectiveness and efficiency of tax control. The complexity of the relationship between tax authorities and taxpayers is due to the contradictions of fiscal interests, on the one hand, and on the other hand, the desire to maximize the profits of individuals and legal entities. A combination of factors such as: subjective assessment of the tax burden, low level of economic literacy of payers, the desire to hide taxes, distrust of the tax authorities, led to the formation of problems. The conflict of these relationships requires the development of optimal formalization of procedures. The elimination of these shortcomings is ensured by the use of a structural-functional approach, which is implemented while taking measures to simplify the procedure for concluding a settlement agreement, the application of penalties for offenses, the introduction of counter benefits in relation to conscientious taxpayers, as well as reducing the fiscal burden.

In addition, accounting and tax approaches to determining the profit tax base differ in terms of the principles of generating income and expenses, methods of assessing fixed and current assets, and in a number of other ways, which has been repeatedly discussed by leading scientists and practitioners on the pages of various publications.

The discrepancies listed above in tax and accounting are not temporary, but permanent, the amount of which every year significantly affects the discrepancy between the financial results of tax and accounting statements. To reflect such discrepancies in accounting, accounts 17 «Deferred tax assets» and 54 «Deferred tax liabilities» are intended, the turnover of which affects the balance sheet in the direction of increase. This information, along with other adjusting balance sheet items, such as tax liabilities and tax credits (data from s/s 643, 644), which are reflected in the liabilities side of the balance sheet, does not give a true picture of the financial position at the balance sheet date. Therefore, it is necessary to minimize discrepancies between accounting and tax accounting for a more reliable reflection of the size of assets, liabilities and equity.

Reducing tax pressure can be achieved through the provision of tax incentives.

Also, an important problem of many enterprises, in particular the analyzed one, is the lack of preferential customs duties. Their absence does not give advantages to DPR enterprises when selling their products in Russia.

Conclusion

The paper considers the theoretical foundations of accounting for tax payments, considers their classification, pays attention to the state of the problem of legal regulation of accounting for tax payments, the tasks of improving the accounting of tax payments and the formation of an accounting policy, accounting for tax payments at an enterprise. The paper considers the structure of tax settlements as an object of accounting in an enterprise, outlines primary and analytical accounting, describes the organization of synthetic accounting, and develops recommendations for improving tax accounting. Also in this section, the methodology for auditing tax calculations is disclosed.

Primary accounting describes the primary documents that are the basis for the calculation of a particular tax, presents documents for their calculation. Analytical and synthetic accounting contain registers, business transactions carried out at the enterprise related to the calculation of taxes are given.

The analysis of accounting of tax payments was carried out and recommendations for its improvement were developed.

At the time of writing this essay, the master's work has not yet been completed. Final completion of construction: June 2023. The full text of the work and materials on the topic can be obtained from the author or his supervisor after the specified date.

References

- Положение (стандарт) бухгалтерского учета 11 «Обязательства», утв. приказом Министерства финансов Украины от 31.01.2000 г. № 20 (с изм. и доп.; в ред. 27.06.2013 г.)

- Закон Донецкой Народной Республики «О налоговой системе» № 99-IHC от 25.12.2015 г. действующ. ред. // Официальный сайт Народного Совета ДНР – Электрон.дан. – Донецк, 2019.

- Давыдов, А.И. Теория и практика налогообложения. Монография. - М.: Русайнс, 2015. - 215 c.

- Брызгалин, А.В. Налоговая оптимизация / А.В. Брызгалин. — М.: Изд-во Норма-М, 2007- 210 с.

- Турчинов, А. И. Опыт теории налогов. Москва, Изд-во: Библиогр.2018. С. 28.

- Ткаченко, Н.М. Бухгалтерский финансовый учет, налогообложение и отчетность: Учебник. - К. 2006. -1080 с.

- Положение (стандарт) бухгалтерского учета 15 «Доходы»: Приказ Министерства финансов Украины от от 29.11.1999 г. № 290 в ред. 09.08.2013 г.) // Официальный сайт Верховного Совета Украины.

- Положение (стандарт) бухгалтерского учета 16 «Расходы»: Приказ Министерства финансов Украины от 31.12.1999 г. № 318 в ред..08.2013 г. // Официальный сайт Верховного Совета Украины.

- 9. Закон Донецкой Народной Республики «О бухгалтерском учете» от 18.12.2020 №223-IIНС

- Шилов, В.Н. «Учет в налогообложении» Днепр, Изд-во: Омега 2018г.-118 с.

- Инструкция о применении Плана счетов бухгалтерского учета активов, капитала, обязательств и хозяйственных операций предприятий и организаций, утв. приказом Министерства финансов Украины от 30.11.1999 г. № 291 (с изм. и доп.)

- Грабова, Н.Н. Бухгалтерский учет на производственных и торговых предприятиях. Учеб. пособие для студентов вузов. - К.: А.С.К., 2000. - 624с.