Abstract

Content

- Introduction

- 1. Theme urgency

- 2. Goal and tasks of the research

- 3. Overview of research and development

- 3.1 Review of international sources

- 3.2 Overview of national sources

- 3.3 Overview of local sources

- 4. Performance audit as a methodological basis for improving financial control

- Findings

- References

Introduction

In the accounting system, information about the costs of the enterprise is extremely valuable for making management decisions. Accounting for the expenses of the enterprise is regularly improved in connection with the use of computer technology and communication environment, methodology and organization of accounting. Successful management of the activities of enterprises is impossible without improving the system of accounting and analysis of the costs of the main activities of the enterprise and the cost of production. The adoption of operational management decisions on the appropriateness of the use of resources, the size and types of costs and the formation of costs becomes possible with the help of accounting and analysis of costs, on which the quality and efficiency of production management mainly depend.

Properly organized cost accounting will make it possible to effectively manage them, increasing production efficiency, maintaining the competitiveness of manufactured products, and increasing economic potential. After all, it is known that well-established accounting of costs and production costs is considered a significant condition for improving the production process. The need for further research into the issues of accounting and analysis of expenses at enterprises in modern economic conditions determined the choice of the topic of this article and its relevance.

1. Theme urgency

The relevance of the chosen topic lies in the fact that the accounting system for income and expenses from ordinary activities is a qualitative basis for the formation of the final financial results of the enterprise, is the starting point from which the strategy and tactics of enterprise management are built. The effectiveness of management decisions, the quality of planning for the future and the effectiveness of this planning depend on how well the work on accounting for income and expenses is planned.

2. Goal and tasks of the research

The purpose of the work is to study the issues of organizing cost accounting in the conditions of the branch “Shakhta im. A.A. Skochinsky”, search for shortcomings in accounting and development of measures to improve accounting at this enterprise.

The objectives of the thesis work are:

- reveal the economic essence and classification of expenses;

- determine the features of cost accounting;

- explore the organization of cost accounting;

- to analyze the practice of keeping records of expenses in the conditions of the branch “Shakhta im. A.A. Skochinsky";

- consider the stages of conducting an audit of expenditures;

- develop proposals for optimizing the methodology and technology for accounting and auditing expenses;

- to study the organization of labor protection at the enterprise.

Research object: accounting and auditing of expenses.

Research subject: improving the methodology of state audit and financial control of enterprise expenses.

3. Overview of research and development

3.1 Review of international sources

In modern economics, scientific, methodological and analytical approaches to the study of this topic have been repeatedly considered by scientists of various schools and directions and are reflected in the scientific A. Chaikovskaya, R.I. Balashova, D.Yu. Samygin and N.G. Baryshnikova A.I. Mordvintseva, V.E. Nadtochy. In their works, a significant part of the authors emphasize that the improvement of the functions of control and audit of enterprise expenses is one of the main directions for achieving an effective result of their activities. However, as an element of assessing their impact on the optimal cost of enterprises, this issue requires further study. Therefore, the purpose of the study is the methodological foundations of digital support for the control and audit of enterprise expenses, their improvement.

Zavyalova E.S. in her article she considered the concept of the cost of production, objects and the main Russian and Western methods of calculating the cost of production. The objects of calculation of the cost of production are largely determined by the type of production, and the method of calculation by the methods of calculation used. The use of specific techniques and methods that make up one or another method of cost accounting are determined by the accounting policy of the organization, the formation of which directly depends on the characteristics of economic activity. Due to the fact that accounting objects and costing objects in production often do not coincide, various methods for calculating the cost of production are used. [1]

Bychkova S.M. and Badmaeva D.G. investigated the issues of accounting for the organization's costs in accordance with the requirements of the law, analyzed the criteria for recognition of expenses in Russian and international accounting practice, proposed a methodology for calculating the amounts of estimated liabilities associated with remuneration for labor, recommended financial indicators for analyzing the effectiveness of the organization's expenses. [2]

Mamushkina I.V. the article considered methods for auditing production costs, typical errors that lead to distortion of information, and ways to eliminate them. Due to the fact that at present most auditors use only a small part of the existing methods in their practical work, there is a need for a comprehensive study and scientific classification of audit methods known to specialists and possible to use. [3]

At present, the financial management of companies is increasingly considering tax liabilities as an independent object of audit, which is explained by the significant amount of tax deductions from enterprises to the budget and extra-budgetary funds, the peculiarities of tax legal relations and the nature of tax liability. In the article by Usatova L.V. the Conceptual model of tax audit, its directions, the methodology for auditing individual taxes, as well as its methodology are considered. [4]

3.2 Overview of national sources

In his article "Methodological approach to the analysis of costs for the development of new products in mechanical engineering" Serdyuk V.N. Professor of Donetsk National University proposed a methodical approach to the analysis of costs associated with the development of new products, by defining the boundaries of the development process and distinguishing two stages in it (technical and economic) and clarifying the classification of types of costs for their implementation, which allows more reasonably to identify reserves to reduce increased costs for preparation of production and development of new types of machine-building products. [5]

The issues of accounting for the expenses of the enterprise were considered by the professor of the accounting department of the Donetsk National University of Economics and Trade named after Mikhail Tugan-Baranovsky Rassulova Nadezhda Vasilievna. Her article is devoted to the study of the practice of formation, determination, and accounting reflection of financial results at enterprises in developed capitalist countries. Recommendations for improving the model for the formation of financial results in domestic practice have been formulated. [6]

3.3 Overview of local sources

The methodology for accounting for expenses and attributing depreciation and depreciation to the cost of production was described in detail and disclosed in his work “Features of reforming the accounting for operations with fixed assets and its impact on equity” by prof. Gavrilenko V.A. and Associate Professor Leonova L.A. They considered the problem of attributing capital investments to the cost price, and not to current expenses, as well as accounting for the revaluation of fixed assets. They proved the illegitimacy of comparing the concepts of capital and current repairs, as well as the illegitimacy of attributing revaluations and capital repairs to expenses. [7]

4. Performance audit as a methodological basis for improving financial control

Performance audit is one of the main methods of financial control that allows assessing the effectiveness of financial flows and state property management, as well as the effectiveness of tax administration, identifying opportunities for improving the implementation of government decisions, and developing recommendations for further actions.

The transition of the organization of the budget process in Russia to the principles of efficiency of budget expenditures requires the regulatory authorities to create adequate financial control mechanisms to determine the degree of achievement of the planned socio-economic results, thereby assessing the effectiveness of the use of public funds by executive authorities. However, a unified methodology for the implementation of state financial control has not yet been developed. An appropriate basis is required for the implementation of an assessment of the effectiveness of the use of public funds, the weak implementation of the preliminary control functions, which is largely formal in nature and is not supported by measures to eliminate the identified shortcomings, makes itself felt. The consequence of this problem is the narrowing of the range of control over the receipt of income in a particular budget, which primarily affects the level of its filling for the subsequent period. [8]

The effectiveness of the use of public funds can be characterized from different angles and include, depending on the objectives of the audit, the determination of the economy and productivity of use, as well as the effectiveness of activities to achieve the set tasks. Thrift refers to the achievement by the auditee of specified results with the minimum amount of public funds or the best result with a given amount of public funds and can be determined by comparing the amount of funds spent on the purchase of resources with the same indicator of the previous year or with that of other organizations. In this case, the organization must produce a specified volume of products or provide the required number of services of appropriate quality.

A more difficult methodological task is the assessment of social performance, which is associated with the identification of the final social effect for society as a whole or a certain part of the population, obtained as a result of the performance of the functions and tasks assigned to it by the audited organization. To do this, it is necessary to have a set of specific and quantitatively measurable indicators that reflect the performance of a particular function or task, as well as characterize the planned social results. The absence of such indicators requires additional work to create methods and criteria on the basis of which it would be possible to assess the social effectiveness of the use of public funds.

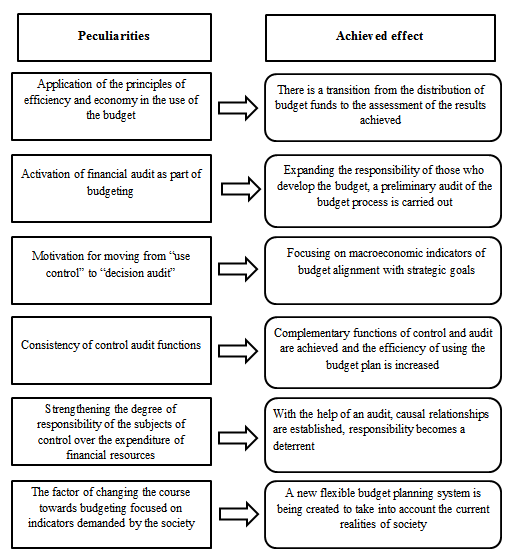

Methodological features of public audit related to improving the efficiency of financial resource management (Fig. 1)

Figure 1 - Methodological features of public audit related to improving the efficiency of financial resource management

The basis of a unified control methodology, in our opinion, can be a performance audit, which mainly involves checking the quality of management, as well as distinguishing between the concepts of "performance control" and "control efficiency". In practice, this will minimize the number of complex field audits and thematic audits.

In Russian legislation, including regional legislation, there are no definitions for a number of concepts widely used in control activities. As a result, terminological confusion often arises, as evidenced by speeches in periodicals and at conferences, when everyone interprets the term "performance audit" in their own way.

The effectiveness of financial control implies a dual interpretation: on the one hand, the effectiveness of the use of budgetary funds, on the other hand, the effectiveness of state financial control methods.

Monitoring the efficiency of spending budgetary funds and the use of state property involves:

- organization and control over the timeliness of the execution of revenue and expenditure items of budgets and state off-budget funds in terms of volume, structure and purpose;

- determination of expediency of expenses and use of state property;

- assessment of the validity of income and expenditure items of budgets.

Thus, the efficiency of budget execution is the leading indicator of the quality of public spending. Quantitatively, the effectiveness of budgetary policy is measured by the ratio of the results obtained to the amount of expenditures incurred. The effectiveness of state financial control methods is largely determined by the system of its organization. The measure of effectiveness is the ratio of the result (the effect of verification) to the costs associated with obtaining this result. When considering the category of efficiency in relation to financial control, one methodological feature stands out that distinguishes it from the category of efficiency in relation to production.

An economical use of resources is when the actual cost of a unit of a resource is less than the planned one or less than the cost of a similar resource used by other organizations to produce similar services. A typical example of the economy in the use of public funds is the reduction in the cost of purchasing goods and services through competitions. Thus, such an activity is considered economical if less money is spent on acquiring the necessary resources of the required quality than, for example, in the same period of the previous year.

The effectiveness of the use of public funds is characterized by the degree of compliance of the actual results of the audited organization with the planned ones and, taking into account their duality, should also be determined from two sides: production (economic) and social.

It is necessary to learn how to predict the situation with minimal errors, to control the effectiveness of decisions made in terms of economic or social benefits at the present time and in the future, even if decisions are made within the framework of current legislation. This is a new approach to state financial control, and it must have appropriate legislative support, which is not available today.

The performance audit for all the main parameters of the control activity has a more complex methodology, requires significantly larger procedures, as well as serious time and resources compared to traditional financial audit, since the choice of topics and objects of performance audit, their preliminary study, and especially the formation of audit evidence requires obtaining extensive information and studying many documents and materials. [9]

The emergence of performance audit, on the one hand, is a consequence of the development of the financial system of the state, and on the other hand, one of the factors contributing to its reform in order to improve the efficiency of public financial management. In the performance audit process, a variety of analytical and evaluation methods and procedures are used, various surveys and questionnaires are often conducted, which require careful preparation and considerable time.

The full performance audit cycle includes the stages of directly organizing and conducting a performance audit (planning, checking and preparing a report), as well as the stages of monitoring the use of audit results (implementation of recommendations and determination of the socio-economic effect obtained).

The performance evaluation criteria can be considered as qualitative and/or quantitative characteristics of the activity of the audited entity in the use of public funds, which show what should be in the audited area and what results are evidence of the effective use of public funds.

Performance audit, as a rule, covers issues of great importance for society, protects the financial interests of the state, allows you to determine the causal relationships of their non-compliance, makes it possible to make timely proposals to eliminate the causes of non-compliance with the requirements established by law. Performance audit does not replace other methods of public financial control; its demand as a method of state financial control is especially great in the budget system, which is focused on achieving a specific end result.

As you know, the forms of financial control exercised by legislative and representative authorities are established by the Budget Code of the Russian Federation. Based on the essence of the definitions given by the legislator to preliminary, current and subsequent financial control, it is rather difficult to interpret performance audit as a special or new form of state financial control, however, in our opinion, it is still necessary to give performance audit such a status. [10]

From a practical point of view, a performance audit is a complex procedure that covers a significant time frame and requires, among other things, high professionalism of the personnel of the control bodies.

Findings

It can be concluded that cost accounting in an enterprise is quite significant, since a correct assessment of expenses can improve the operation of an enterprise in general. Also, as a result of the analysis of accounting practice, it was found that there are obvious contradictions in standards 7 and 16 that require improvements, since in a number of cases they (accounting for current and major repairs, accounting for depreciation, markdowns, revaluations, etc.) and violate the principle of accounting accounting "Compliance of income and expenses". This results in a material misstatement of the financial statements.

References

- Бычкова С.М., Бадмаева Д.Г. Бухгалтерский учет и анализ расходов организации / С.М. Бычкова, Д.Г. Бадмаева // Известия Санкт-Петербургского государственного аграрного университета. – 2014. [Электронный ресурс]: https://cyberleninka.ru/article/n/buhgalterskiy-uchet-i-analiz-rashodov-organizatsii

- Гавриленко В.А., Леонова Л.А. Особенности реформирования учета операций с основными средствами и его влияния на собственный капитал / В.А. Гавриленко, Л.А. Леонова // Вестник Института экономических исследований. – 2017. [Электронный ресурс]: https://cyberleninka.ru/article/n/osobennosti-reformirovaniya-ucheta-operatsiy-s-osnovnymi-sredstvami-i-ego-vliyaniya-na-sobstvennyy-kapital

- Гаджиев Н.Г., Ахмедов А.З., Гаджиев А.Н. Внутренний аудит в высших учебных заведениях: теория и практика его осуществления / Н.Г. Гаджиев, А.З. Ахмедов, Н.А. Гаджиев // Экономический анализ: теория и практика. – 2018. [Электронный ресурс]: https://www.elibrary.ru/item.asp?id=10133541

- Дроботова, Е. В. Аудит эффективности бюджетных средств / Е. В. Дроботова // Молодой ученый. — 2014. [Электронный ресурс]: https://moluch.ru/archive/78/13566/

- Завьялова Е.С. Методы учета затрат на производство продукции / Е.С. Завьялова // Научно-исследовательские публикации. – 2015. [Электронный ресурс]: https://cyberleninka.ru/article/n/metody-ucheta-zatrat-na-proizvodstvo-produktsii

- Мамушкина И.В. Методы проведения аудита затрат на производство продукции. Типичные ошибки, приводящие к искажению информации, и их устранение / И.В. Мамушкина // Вестник НГИЭИ. – 2011. [Электронный ресурс]: https://cyberleninka.ru/article/n/metody-provedeniya-audita-zatrat-na-proizvodstvo-produktsii-tipichnye-oshibki-privodyaschie-k-iskazheniyu-informatsii-i-ih-ustranenie

- Рассулова Н.В., Корогодина А.М. Учет финансовых результатов: сравнительная характеристика отечественной и зарубежной практики, проблемы и пути решения / Н.В. Рассулова, А.М. Корогодина // Мир науки и образования. – 2018. [Электронный ресурс]: https://cyberleninka.ru/article/n/uchet-finansovyh-rezultatov-sravnitelnaya-harakteristika-otechestvennoy-i-zarubezhnoy-praktiki-problemy-i-puti-resheniya

- Рябухин С.Н. Аудит эффективности использования государственных ресурсов / С.Н. Рябухин // Монография. – 2018. [Электронный ресурс]: https://search.rsl.ru/ru/record/01002448664

- Сердюк В.Н. Методический подход к анализу затрат на освоение новой продукции в машиностроении / В.Н. Сердюк // Экономика: реалии времени. – 2013. [Электронный ресурс]: https://cyberleninka.ru/article/n/metodicheskiy-podhod-k-analizu-zatrat-na-osvoenie-novoy-produktsii-v-mashinostroenii

- Усатова Л.В. Организация процесса налогового аудита расходов / Л.В. Усатова // Экономический анализ: теория и практика. – 2008. [Электронный ресурс]: https://cyberleninka.ru/article/n/organizatsiya-protsessa-nalogovogo-audita-rashodov