Analysis and directions for improving the organization of state audit and financial control of the efficiency of financial and economic activities of a state unitary enterprise in the conditions of the Subsidiary "Republican Market No. 6/3" of the State Enterprise "Donbass Markets"

Content

- Introduction

- 1. Relevance of the topic

- 2 The purpose and objectives of the study

- 3 Ensuring economic growth

- 3.1 The scheme of achieving sustainable economic development

- 3.2 Key indicators of sustainable development

- 3.3 Types of sustainable development assessment

- 3.4 Integral indicators

- Output

- List of sources

Introduction

The main disadvantages of the control of financial and economic activities, the imperfection of state regulation of this activity are considered.

The high technogenic load of industrial enterprises on the sustainability indicators of the region as a whole is indicated, the need to take this component into account when conducting an audit and control of enterprises is justified. It is proved that the process of forming a comprehensive assessment of the sustainable development of the enterprise is based on the analysis of the final financial result, taking into account internal and external factors affecting the economic, environmental and social results of the enterprise.

The most progressive methods of accounting for key indicators of sustainable development of the enterprise were given in the work. The novelty of the results obtained consists in deepening the existing theoretical provisions and developing practical recommendations for improving the control and audit of financial and economic activities of state unitary enterprises on the basis of key indicators of sustainable development in conditions of increasing influence of the information component of the economy on economic processes [3].

1 Relevance of the topic

The relevance of the topic is due to the need for further scientific study of the organization of control and audit of the effectiveness of financial and economic activities of state unitary enterprises on the basis of key indicators of sustainable development [1].

The object of the study is the financial and economic activity of a state unitary enterprise.

The subject of research is the improvement of the system of control and audit of the efficiency of financial and economic activities of a state unitary enterprise based on the concept of sustainable development [4].

2 The purpose and objectives of the study

The purpose is to identify ways to improve the system of control and audit of financial and economic performance indicators of a state unitary enterprise on the basis of key indicators of sustainable development [7].

To achieve this goal, it is necessary to perform the following tasks:

3 Ensuring economic growth,

To ensure sustainable economic growth, it is necessary to ensure any of the following components:

1) changing the flow of financial resources:

- inflow of financial resources providing an ultra-liquid balance;

- absence (or low level) of accounts payable;

- reinvesting profits in their own activities.

2) significant production potential, providing:

- growth of stock and material output;

- reduction of stock and material consumption;

- increase in the turnover of working capital and output by 1 ruble of invested capital;

- resource-saving policy;

- reduction of the cost of production.

3) optimal scientifically-based management decisions on:

- optimization of the capital structure;

- choosing the direction of production development;

- justification of the product range;

- changes in seasonal demand;

- justification of the amount of a short-term loan [10].

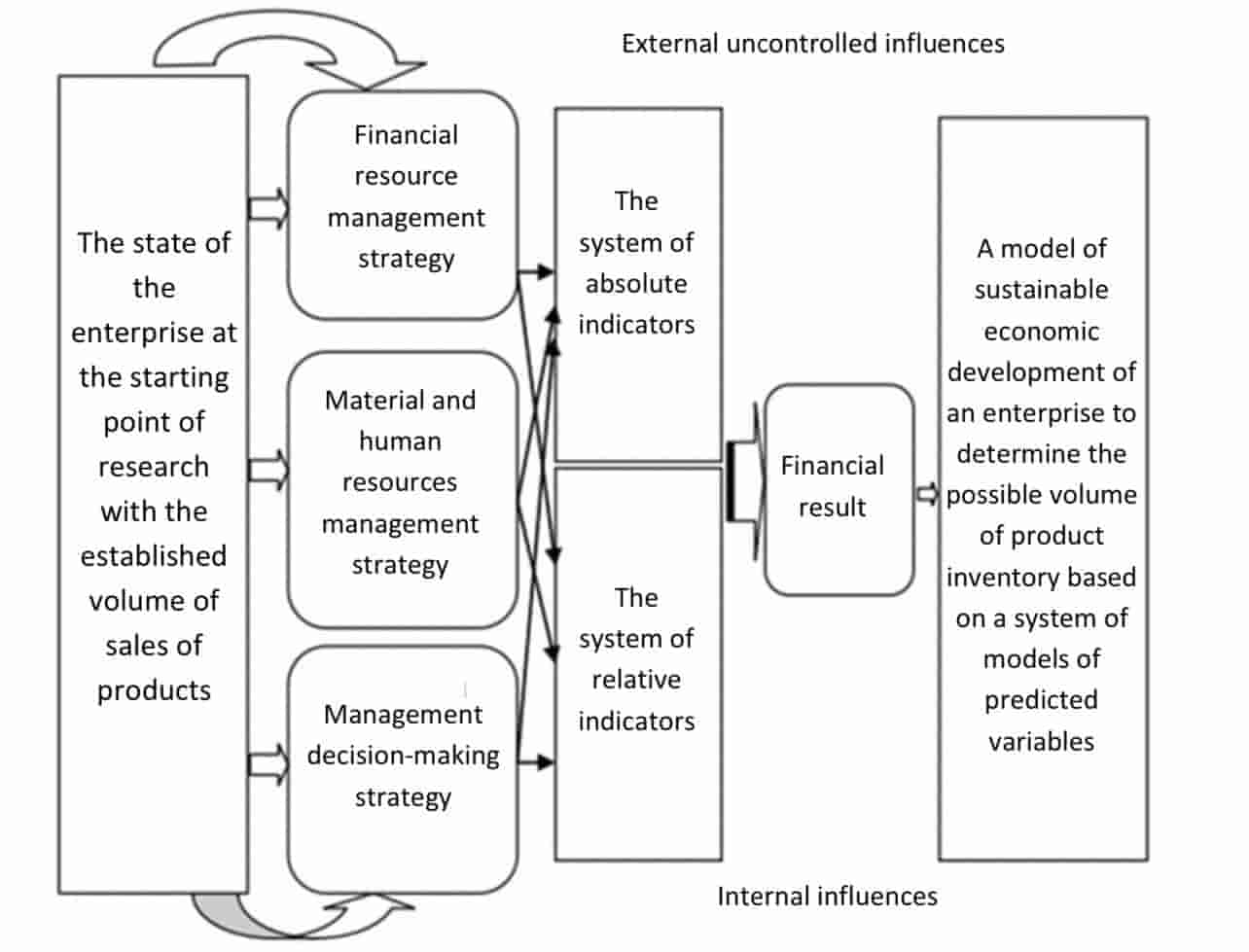

3.1 The scheme of achieving sustainable economic development

Picture 3.1 – The scheme of achieving sustainable economic development

Schematically, the concept can be represented as the cumulative impact of financial, material and labor resources, as well as the selected strategies for managing them on the final result[8].

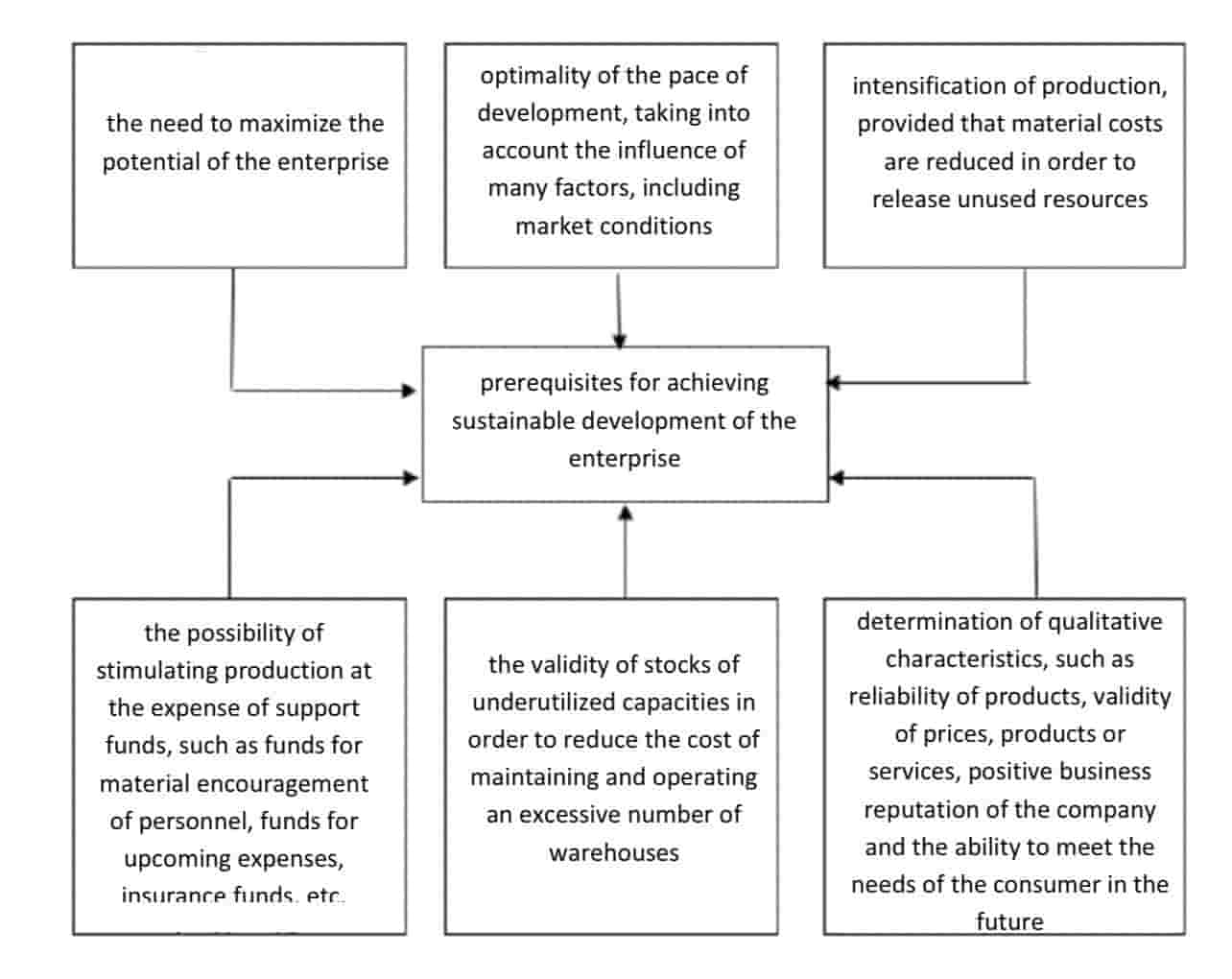

3.2 Key indicators of sustainable development

Picture 3.2 Key indicators of sustainable development

Picture 3.2 Key indicators of sustainable development

At the same time, it is necessary to know and understand the main indicators of the sustainable development of the enterprise:

- production (commodity products in actual and comparable prices, the index of growth in the volume of products, products sold, production costs, cost growth index, the share of variable costs in the cost of production, output per worker, the percentage of orders completed on time);

- social (the number of employees by category, the ratio of wages to the subsistence minimum, the ratio of the average monthly salary of employees to the average monthly salary in the country)

- financial and economic (working capital, own working capital, net profit, net profitability, current liquidity, return on funds) [4].

3.3 Types of sustainable development assessment

The process of forming a comprehensive assessment of the sustainable development of the enterprise is based on a system of integral indicators:

- the financial stability of an enterprise is a reflection of a stable excess of income over the expenses of the enterprise, ensuring the free turnover of its cash flows;

- marketing (market) sustainability - reflects the needs of the market in terms of the range of manufactured products in terms of quantity, price, quality, market needs for new products that correspond to the profile of the enterprise from the standpoint of technology and technology, as well as the possibility of conquering new sales markets;

- production sustainability - characterizes the presence of such a production potential at the enterprise, which is able to provide a break-even production volume;

- innovative sustainability - characterizes the ability of an enterprise to introduce new technologies and ways of organizing production, to produce new types of products, perform new types of work, and provide new types of services.

A system of indicators is proposed that is sufficient to assess the sustainable development of the enterprise and takes into account the interests of both internal and external users [5].

Integral indicators

The system of indicators sufficient to assess the sustainable development of the enterprise and taking into account the interests of both internal and external users includes:

- integral indicator of a comprehensive assessment of the financial stability of the enterprise;

- an integral indicator of a comprehensive assessment of the marketing (market) stability of the enterprise;

- an integral indicator of a comprehensive assessment of the production sustainability of the enterprise;

- an integral indicator of a comprehensive assessment of the innovative sustainability of the enterprise [5].

Picture 3.3 – Growth of integral indicators

When monitoring and auditing the effectiveness of financial and economic activities of a state unitary enterprise based on key indicators of sustainable development, special attention should be paid to the risks of control. The audit risk assessment should be carried out taking into account the risk of environmental activities.

The traditional financial reporting system for the needs of monitoring and auditing of key indicators of sustainable development does not fully meet the needs of internal and external users, in this regard, it is recommended, along with the control of standard financial statements, to audit the integrated (non-financial) reporting of business entities.

However, at the stage of analyzing indicators of sustainable development of enterprises, a significant disadvantage is the lack of uniform and universal indicators that allow companies and industries to be compared and analyzed on the basis of key indicators in the field of sustainable development. Standardization of this process undoubtedly presents prospects for further research and development [2].

Output

1. The issues of control and audit of financial and economic activities, taking into account the indicators of sustainable development, are an urgent topic of scientific research, which is reflected in many scientific research and development.

2. The main disadvantages of control lie in the imperfection of the legislative and regulatory framework both for the implementation of financial and economic activities based on the concept of sustainable development and the imperfection of state regulation of the control of this activity.

3. Sustainable development at the state level implies the possibility of increasing the volume of industrial production, improving the living standards of people while preserving and improving the quality of the environment, while the changes are coordinated with each other and aimed at strengthening the current and future potential of the state [1].

4. The root cause of the need to monitor and audit the effectiveness of the financial and economic activities of a unitary enterprise is the dominance of extensive management methods and, as a consequence, the imbalance of environmental, economic and social interests in the nature-society system, which strives to a critical limit and puts forward tasks to ensure the achievement of a sustainable development model [5].

5. The process of forming a comprehensive assessment of the sustainable development of an enterprise is based on the assessment of the final financial result, taking into account internal and external factors, in order to develop management methods that best affect the economic condition of the enterprise, the final results of its activities, the possibility of achieving them with constant consideration of the social and environmental component.

6. When assessing the risks of control, the need to take into account the environmental component and groups of non-financial risks that may affect the overall level of sustainable development of the enterprise is indicated [4].

7. A system of indicators sufficient to assess the sustainable development of an enterprise and taking into account the interests of both internal and external users is proposed and considered, including: a set of local indicators for assessing each of the four types of sustainability; integral indicators for assessing each type of sustainability; integral indicators for assessing the sustainable development of the enterprise as a whole.

8. To interpret these indicators of financial and economic activity of a unitary enterprise on the basis of key indicators of sustainable development in the system of non-financial reporting, the parallel use of the index of sustainable cyclicity, formed in three directions of sustainable development of the enterprise: economic, social and environmental components, taking into account the criteria of cyclical operation of the enterprise, is considered and proposed [2].

9. The necessity of practical control and audit of the efficiency of financial and economic activities of state unitary enterprises on the basis of key indicators of sustainable development is indicated.

List of sources

- Bezrukova T.L. Sustainable development of the enterprise: questions of methodology / T.L. Bezrukova, E.A. Yakovleva, Ch. Jiang // The mechanism of regulation of the economy. - 2008. – No. 3. – pp. 106-113.

- Bagrovnikova A.N. Research of methodological provisions of controlling in the management system of sustainable development of the enterprise / A.N. Bagrovnikova // Socio-economic management: theory and practice. – 2020. – № 4(43). – Pp. 3-10.

- Biryukova V.V. Russian and foreign experience in the formation of indices of sustainable development of vertically integrated oil companies / V.V. Biryukova, A.E. Cherepovitsyn // Economics and Management: a scientific and practical journal. – 2020. – № 6(156). – P. 5-10. DOI: https: // doi.org/10.34773/EU.2020.6.1

- Bodnar I.N. Evaluation of the economic efficiency of using associated petroleum gas as a source of obtaining processed products / I.N. Bodnar, M.M. Kostyaeva, D.K. Lutchenkova // Technological perspective within the Eurasian Space: New Markets and Points of Economic Growth : Proceedings of the 5th International Scientific Conference, St. Petersburg, 07-08 November 2019. – St. Petersburg: Center of Scientific and Production technologies "Asterion". - 2019. – pp. 134-138

- Bychkova E.V. et al. Formation of a mechanism for the organization of accounting for the results of environmental activities of coal mining enterprises // Economics: the realities of time. – 2014. - №3 (13). – Pp. 87-93

- Bychkova E.V. Integrated assessment of the effectiveness of environmental activities of a coal mining enterprise in the process of making a management decision // Improving the competitiveness of economic sectors as a way out of the economic crisis. - 2016. – pp. 97-104

- Vasina E.V. Production stability as a guarantee of enterprise stability / E.V. Vasina // Actual problems of science and technology: A collection of works based on the materials of the IV International Competition of scientific research works, Ufa, April 10, 2021. – Ufa: Limited Liability Company "Scientific Publishing Center "Bulletin of Science", 2021. – pp. 40-47

- Kislinskaya M.V. Managerial control as a basis for sustainable development of organizations / M.V. Kislinskaya, S.V. Sharokhina, O.E. Pudovkina // Prospects for the development of science in the modern world : A collection of articles based on the materials of the VI International Scientific and Practical Conference. In 2 parts, Ufa, March 09, 2018. – Ufa: Dendra Limited Liability Company. - 2018. – pp. 137-141

- Matveeva A.A. Assessment of environmental sustainability of the Volgograd agglomeration based on indicators of sustainable development / A.A. Matveeva, E.A. Gerusova // Landscape geography in the XXI century : Materials of the International Scientific Conference, Simferopol, September 11-14, 2018 / Edited by E.A. Pozachenyuk. – Simferopol: Limited Liability Company "Publishing House Printing House "Arial". - 2018. – pp. 410-414

- Medvedev D.A. Russia -2024: Strategy of socio-economic development // Economic issues. – 2018. - No.10. – p.5-28. DOI: https: // doi.org/10.32609/0042-8736-2018-10-5-28

- Bagrovnikova A.N. Research of methodological provisions of controlling in the management system of sustainable development of the enterprise / A.N. Bagrovnikova // Socio-economic management: theory and practice. – 2020. – № 4(43). – Pp. 3-10.