UKR

|

RUS

Summary of research and developments

Introduction

The

problem of efficient and rational money management has

appeared in Ukraine at the same time when the stock exchange

of the country has been organized. During this period the

process of capital investment started. It is aimed to adjust

normal process of economical development by means of

creation efficient mechanism of transformation of

temporarily surplus funds into loanable funds, conversion of

saving into capital investments.

In developed country

the majour originator of investment process is an

institution of professional traders. Services of mutual

funds, trusts and bond houses play the most important role

in the creation of funds involvement activity.

This services haven't gained that much spread in the

domestic model of stock exchange due to some peculiarities

of stock conjuncture and a poor experience of using economic

mathematical models of money management.

Actuality

of the graduation work theme

Nowadays

there is a great diversity of money management dynamic

methods which are used by stockbrokers for their aims. But

most of them are not reliable enough and vary much

from each other in speed of reaching some definite goals and

complicacy of implementation. In order to gain desirable

results and minimize risks it is necessary to analyze

efficiency of these methods via some certain rates and

factors. The results of comparison will show which one

satisfies traders' purposes best.

The goal of the

investigation

The goal of the

investigation consists of getting reliable datum as for the

comparative analysis of dynamic methods of money management.

In order to do this a few problems should be solved. The

definite series of rates and factors are to be calculate as

those of :

- average rate of return;

- standard deviation of an

investment portfolio;

- Sharpe ratio;

- profit factor.

The datum for calculation

will be obtained by means of model simulation.

Expected practical value of the research

The

future results of the work while used in money management

can provide stockbrokers with some reliable data of ways to

maximize future profits of investment portfolio minimizing

its risks or staying within some restrictions (of maximal

acceptable loss, amount of capital involved, time

restriction etc.) Besides the assumption made may be used

for further researches in order to optimize existing dynamic

algorithms of money management or offering a new one.

Survey of research and

developments

Survey of research and

developments in DonNTU

The

investigation of the theme of the work are conducted by

associate professor Smirnov Alexander, PhD jointly with

Guryanova and Revega. The results of their work are

represented in the articles "About Vince's "Optimal f" [1],

"New in Dynamic Capital Management" and "Multicriteria

Analysis of Dynamic Algorithms of Money Management" [4,5].

The Main propositions of Ralph Vince's

"optimal f" theory

To increase the efficiency of

economic system it is often used to reinvest profit returned

into new investment projects. This lets stockbrokers to gain

additional profit though deals with increasing risks. The

American scientist Ralph Vince suggested the theory of

"optimal f" - the optimal part of capital for increasing

investments.

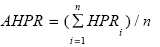

He introduced such notions

as:

- holding period returns

(HPR)

-

profit or loss of an

investor (P&L)

HPR = 1 + P & L ,

if profit

HPR = 1 - P & L

, if loss

(1)

(1)

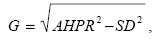

where:

G

and

- is geometrical and arithmetical average

correspondingly

- is geometrical and arithmetical average

correspondingly

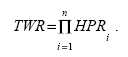

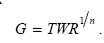

n - number of transactions

In case the profit is reinvested the geometrical average is

more representative than AHPR. The ratio of initial

and ultimate investor's funds is designate as TWR

(Terminal

Wealth

Relative):

(2)

(2)

The geometrical average is

designate as:

(3)

(3)

Without any sufficient mathematical

proves by means of reflection R. Vince introduce the notion

of a share of invested funds а

which according to his point of view is "optimal f"

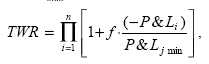

for

max TWR

(4)

(4)

where:

- f -

percentage of funds to be reinvested

-

(-P&L) -

profits and loss with opposite sighns

-

P&Lj min -

the biggest loss

-

opt f -

one of the values of

f , when TWR = TWRmax.

Survey of foreign research and

developments

There are a great

diversity of research on the theme abroad. Ralph Vince in

his work "The Mathematics of money Management. Risk Analysis

Techniquesfor Traders" criticizes the Kelly's formula and

introduce his own criteria "optimal f"- percentage for

reinvestment. [3]

The theory suggested by

Vince is criticized in the article of Leo J. Zamansky,

Ph.D., and David C. Stendahl "Secure Fractional Money

Management". The introduce their own criteria named "secure

f". To formulate the problem solved by secure f, they add a

constraint into the calculation of optimal f. The constraint

may reflect the acceptable maximum drawdown (and/or other

characteristics). This is a more conservative strategy that

has the benefit of finding the percent of equity invested in

every trade that would have yielded the highest possible

return subject to the acceptable maximum drawdown. This

formulation of the problem is such that its solution will

maximize TWR and guarantee that the drawdown when running

the system on past data does not exceed the amount defined

by the trader — value D. [6]

Conclusions

For empirical researchers, the conclusion that

capitalization and money management may play a role in

determining the success or failure of speculative traders

cannot be ignored. The underestimation of any strategy

drawbacks can result that the propensity for

account balances to be reduced to zero by undercapitalizing

futures trading positions and possibility of this is

quite high and may contribute to the failure of many

speculators. Finally, many works on the performance of

technical trading models have reported results for a single

futures contract for simplicity/comparability or for other

reasons. The research presented here allows greater

reconciliation between planned results and the trading

performance more likely to be encountered by traders with

respect to risk attitudes observed in behavioral finance

characteristics and the reinvestment of profits in

speculative trading.

References

1. Смирнов А.В., Гурьянова Т.В. Об

«оптимальном f» Ральфа Винса. Научные труды Донецкого

национального технического университета, серия

«Информатика,

кибернетика и вычислительная техника»,

вып. 9 (132), Донецк, ДонНТУ, 2008. - С 216-220

2. Швагер Дж.

Технический анализ. Полный курс. - М.: Альпина Паблишер,

2001. - 768с.

3. Винс Р. Математика

управления капиталом.Методы анализа риска для трейдеров и

портфельных менеджеров: Пер. с англ. – М.: Альпина Паблишер,

2001. – 400 с.

4. Смирнов А.В.,

Гурьянова Т.В. Новое в динамическом управлении капиталом.

Научные труды Донецкого национального технического

университета, серия

«Информатика, кибернетика и

вычислительная техника», 2009 (в

печати).

5. Смирнов А.В.,

Гурьянова Т.В. Многокритериальный

анализ эффективности алгоритмов динамического управления

капиталом. Научные труды Донецкого национального технического

университета, серия

«Информатика, кибернетика и

вычислительная техника», 2009 (в

печати).

6.

Zamansky, Leo J., and David Stendahl [1997]. Dynamic

zones, Technical Analysis of STOCKS & COMMODITIES, Volume

15: July.

7.

Мертенс А.В. Инвестици: Курс лекций по современной

финансовой теории. - К.: Киевское инвестиционное агенство,

1997.- 416 с.

8. Van K. Tharp, Ph.D.

Special Report on Money Management/

Copyright © 1997 by I.I.T.M., Inc.

9.

Брандт З. Анализ данных. Статистические и вычислительные

методы для научных

работников и инженеров: Пер. с англ. – М.: Мир, ООО «Изд.

АСТ», 2003. – 686 с.

10.

Лоу А.М., Кельтон В.Д. Имитационное моделирование. Классика

CS. 3-е изд.: Пер.

с англ. – СПб.: Питер; Киев: Изд. группа BHV, 2004. - 847 с.