| Summary of master's degree work | ||||

|

English | Russian

http://www.12manage.com/methods_balancedscorecard.html History of the Balanced ScorecardIn 1992, an article by Robert Kaplan and David Norton entitled "The Balanced Scorecard - Measures that Drive Performance" in the Harvard Business Review caused a lot of attention for their method, and led to their business bestseller, "The Balanced Scorecard: Translating Strategy into Action", published in 1996.

The financial performance of an organization is essential for its success. Even non-profit organizations must deal in a sensible way with funds they receive. However, a pure financial approach for managing organizations suffers from two drawbacks:

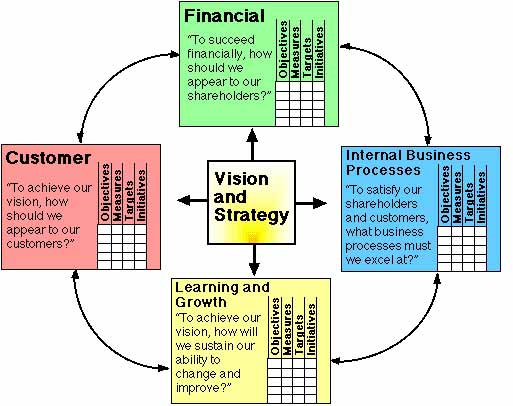

The 4 perspectives of the Balanced ScorecardThe Balanced Scorecard method of Kaplan and Norton is a strategic approach, and performance management system, that enables organizations to translate a company's vision and strategy into implementation, working from 4 perspectives:

This allows the monitoring of present performance, but the method also

tries to capture information about how well the organization is positioned

to perform in the future. Benefits of the Balanced ScorecardKaplan and Norton cite the following benefits of the usage of the Balanced Scorecard:

1. The Financial PerspectiveKaplan and Norton do not disregard the traditional need for financial data. Timely and accurate funding data will always be a priority, and managers will make sure to provide it. In fact, there is often more than sufficient handling and processing of financial data. With the implementation of a corporate database, it is hoped that more of the processing can be centralized and automated. But the point is that the current emphasis on financial issues leads to an unbalanced situation with regard to other perspectives. There is perhaps a need to include additional financial related data, such as risk assessment and cost-benefit data, in this category.

2. The customer perspectiveRecent management philosophy has shown an increasing realization of the importance of customer focus and customer satisfaction in any company. These are called leading indicators: if customers are not satisfied, they will eventually find other suppliers that will meet their needs. Poor performance from this perspective is thus a leading indicator of future decline. Even though the current financial picture may seem (still) good. In developing metrics for satisfaction, customers should be analyzed. In terms of kinds of customers, and of the kinds of processes for which we are providing a product or service to those customer groups.

3. The Business Process perspective

4. Learning and Growth perspectiveThis perspective includes employee training and corporate cultural attitudes related to both individual and corporate self-improvement. In a knowledge worker organization, people are the main resource. In the current climate of rapid technological change, it is becoming necessary for knowledge workers to learn continuously. Government agencies often find themselves unable to hire new technical workers and at the same time is showing a decline in training of existing employees. Kaplan and Norton emphasize that 'learning' is something more than 'training'; it also includes things like mentors and tutors within the organization, as well as that ease of communication among workers that allows them to readily get help on a problem when it is needed. It also includes technological tools such as an Intranet.

The integration of these four perspectives into a one graphical appealing picture, has made the Balanced Scorecard method very successful as a management methodology.

Objectives, Measures, Targets, and InitiativesFor each perspective of the Balanced Scorecard four things are monitored (scored):

Double-Loop FeedbackIn traditional industrial activity, "quality control" and "zero

defects" were important words. To shield the customer from receiving poor

quality products, aggressive efforts were focused on inspection and

testing at the end of the production line. A problem with these approaches

- as pointed out by Deming - is that the true causes of defects could

never be identified, and there would always be inefficiencies because

products with a defect are rejected. Deming understood that variation is

created at every step in a production process, and the causes of variation

need to be identified and repaired. If this can be done, then there is a

way to reduce the defects and improve product quality indefinitely. To

establish such a process, Deming emphasized that all business processes

should be part of a system, with feedback loops. The feedback data should

be examined by managers to determine the causes of variation, and what are

the processes with significant problems. Then they can focus their

attention on repairing that subset of processes.

Outcome MetricsYou can't improve what you can't measure. Therefore metrics must be

developed based on the priorities of the strategic plan, which provides

the key business drivers and criteria for metrics managers most desire to

watch. Processes are then designed to collect information relevant to

these metrics and reduce it to numerical form for storage, display, and

analysis. Decision makers examine the outcomes of various measured

processes and strategies and track the results to guide the company and

provide feedback.

Management by FactThe goal of measuring is to permit managers to see their company more

clearly - from many perspectives - and hence to make wiser long-term

decisions. A 1997 booklet on the Baldrige Criteria

summarizes this concept of fact-based management: Cautionary note on using the Balanced ScorecardYou tend to get what you measure. People will work to achieve the

explicit targets which are set. For example, emphasizing traditional

financial measures may encourage short-term thinking. The Core Group

Theory by Kleiner provides further clues on the mechanisms behind

this. Kaplan and Norton recognize this, and urge for a more balanced set

of measurements. But still, people will work to achieve their scorecard

goals, and may ignore important things which have no place on their

scorecard. Evolution of the Balanced ScorecardIn 2002, Cobbold and Lawrie developed a classification of Balanced Scorecard designs based upon the intended method of use within an organization. They describe how the Balanced Scorecard can be used to support three distinct management activities, the first two being management control and strategic control. They assert that due to differences in the performance data requirements of these applications, planned use should influence the type of BSC design adopted. Later that year the same authors reviewed the evolution of the Balanced Scorecard as shown through the use of Strategy Maps as a strategic management tool, recognizing three distinct generations of Balanced Scorecard design. | ||||