{kind=link}

Abstract for theme of master's work

Introduction

The trading system is the code of rules and conditions that trader use to execute trading operations on a financial market [1]. Nowadays advances in computer technology as well as development of trading methods and tools afford an opportunity to create a complex and multifunctional computer trading systems (CTS). These systems can completely automate the process of trading.

Urgency of a theme of research

Computer trading system is a very complex system, which consists of many interconnected subsystems. The classical scheme of CTS consists of two components: generation of entry signals and generation of exit signals. However this scheme has already gone out of dates. The development of dynamic money management enabled to supplement CTS with algorithms of determination the value of open positions. Modern CTS needs to have operative control methods and tools to analyze the efficiency of the system. And in addition, there is a necessity to provide opportunities for further optimization of the system [2,3].

The complexity of CTS makes it necessary to determine which of its subsystems is more important for successful trading. It will identify subsystems that require more attention during engineering of CTS.

Aims and objectives of research

The aim of master’s dissertation is to considerate the complete structure of a computer trading system and make sensitivity analysis of the influence of subsystems to a general trading system concerning the most widely used algorithms and indicators.

The objectives of the work:

- To make a systematization of the structure of CTS;

- To develop a CTS, which includes all the components of its structure;

- To test CTS in the conditions when parameters of one separate subsystem is optimized and parameters of other subsystems are fixed;

- To determine the percentage of influence of each subsystem on the general efficiency characteristics of CTS.

Object of research: Computer trading system

Subject of research: Influence of efficiency of subsystems of computer trading system on general efficiency of CTS.

Scientific novelty

Nowadays, there are no methods which allow allocating and comparing elements of CTS. It complicates search of "bottlenecks" and system optimization.

So the scientific novelty of this work consists in allocation of subsystems of computer trading system and evaluating the efficiency of each subsystem on multicriteria basis.

Expected practical results

The result of master's work will be the percentage of influence of various subsystems on general efficiency of CTS. It will identify subsystems that require more attention during engineering of CTS.

A review of research on the subject

After the search at global, national and local levels it can be maintained that there is no work similar to this. But there are many works which have similar themes: the development and optimization of computer trading systems, research in the field of technical analysis and dynamic money management.

This topic has been studied by following scientists and economists: J. Schwager T. R. DeMark, A. Elder, V. Yakimkin, A. Stecenko, V. Alekchin, E. Naiman, V. Gordon, A. Smirnov.

Summary of own results available at the time of completion the abstract

Structure and features of the functioning of CTS

Computer trading system consists of several interconnected subsystems. Let's consider them in details (pic. 1) [2,3].

The subsystem of entry signals' generation determines the time to enter the market. This subsystem can be divided into two subsystems depending on the type of signal:

- Subsystem of generating signals to buy issues opens a long position;

- Subsystem of generating signals to sell issues opens a short position.

The most frequently in CTS the entry signals are generated by technical market indicators.

The subsystem of exit signals' generation determines the time to exit the market. This subsystem ensures the timely closing of an open position that will get the maximum profit from the transaction [4].

The subsystem of emergency protection generates stop-loss signals to exit the market. This signal is often called protective stop or money management exit. The purpose of this subsystem is to prevent great loss by the timely closing of unprofitable positions [4].

The subsystem of dynamic money management determines the value of open position. A lot of traders don’t pay attention to this subsystem. But it is necessary to mention that the value of open position directly influences the rate of increasing the trading account [5].

The subsystem of the operative control of indicators determine the quality of trading signals issued by indicators, and allows or forbids usage of a particular indicator in CTS. This subsystem is necessary due to the fact that all currently known indicators make mistakes in generating trading signals [6,7].

The subsystem of an estimation economic and technical efficiency of CTS. This subsystem allows estimating results of trading system’s work, both at a testing stage, and during the trading. With the help of efficiency characteristic it is possible to evaluate working quality of other subsystems and to identify opportunities to improve productivity of separate subsystems and whole CTS. The data of this subsystem are used by other subsystems of CTS [2,3].

Research of elements of trading system

Creating an effective trading system requires the development and optimization of all its components separately. However a lot of interconnected subsystems cause difficulties in development and testing of CTS.

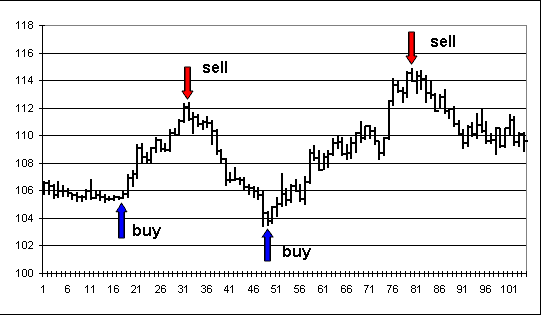

To carry out independent testing of subsystems we use the following method: parameters of one subsystem change, while parameters of other subsystems are fixed. The received characteristics of subsystems are compared with the standard version. This standard is the system with ideal entrances and exits at the turns of the market (pic 2) [3].

Conclusion

Computer trading system is a very complex system, which consists of many interconnected components. Creating an effective trading system requires the development and optimization of all its components. It is quite labour-intensive process. Therefore it is important to know which subsystems require more attention during development of CTS. To answer this question, it is necessary to make sensitivity analysis of subsystems’ influence on general efficiency of CTS.

The goal requires the isolation of subsystems during testing. But it is difficult to implement because of the existence of close connections between subsystems. The solution may be the following: to use a set of standard strategies for fixing the parameters of subsystems.

References

- Торговые системы [Электронный ресурс]/ TradeForecast (Торговые прогнозы), – http://tradeforecast.biz/ru/usefull/111--forex/2051--forex-

- Євтюшкіна А.Б. Побудова систематизованої структурної схеми комп’ютерної торгівельної системи /«Сучасна інформаційна Україна: Інформатика, економіка, філософія»: матеріали доповідей конференції, 13 – 14 травня 2010 року, Донецьк, 2010. Т. 1. – 438 c., с. 358-362.

- Евтюшкина А.Б. Исследование влияния подсистем компьютерной торговой системы на ее результирующие характеристики/ Електроний збірник трудів V науково-практичної конференції «ДОНБАС-2020: перспективи розвитку очима молодих вчених», Донецькій національний технічний університет, м. Донецьк, 25-27 травня 2010 р., – http://2020.donntu.ru/

- Джефри Оуэн Кац, Донна Л. МакКормик. Энциклопедия торговых стратегий/ Пер. с англ. – М.:Альпина Паблишер, 2002 – 400 с.

- Винс Р. Математика управления капиталом.Методы анализа риска для трейдеров и портфельных менеджеров: Пер. с англ. – М.: Альпина Паблишер, 2001. – 400 с.

- Голбан А.П. Автореферат на тему «Разработка и исследование алгоритмов адаптации компьютерных торговых систем к рыночной ситуации»[Электронный ресурс]/ Портал магистров ДонНТУ, – http://masters.donntu.ru/2008/fvti/golban/diss/index.htm

- Элдер А Основы биржевой торговли.[Электронный ресурс]/ Trader Online Library, – http://www.trader-lib.ru/books/508/20.html

Important:

Master's work has not completed when this abstract was written. Completion of the master's work: December 2010. Full text of the work and materials on the topic can be obtained from the author or her supervisor after that date.